Вам также может понравиться

- North Nashville Transit Center CommutesДокумент4 страницыNorth Nashville Transit Center CommutesUSA TODAY NetworkОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- AFP Poll CrosstabsДокумент17 страницAFP Poll CrosstabsUSA TODAY NetworkОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Skrmetti OpinionДокумент10 страницSkrmetti OpinionUSA TODAY NetworkОценок пока нет

- Recall Labels 006 2024Документ29 страницRecall Labels 006 2024USA TODAY NetworkОценок пока нет

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- EducationFreedomScholarships Amd - SB2787Документ7 страницEducationFreedomScholarships Amd - SB2787USA TODAY NetworkОценок пока нет

- Choose How You Move Transit Improvement Program MapsДокумент6 страницChoose How You Move Transit Improvement Program MapsUSA TODAY Network100% (1)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- House Omnibus Amendment HB1183 - Amendment (014448)Документ39 страницHouse Omnibus Amendment HB1183 - Amendment (014448)USA TODAY NetworkОценок пока нет

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Tennessee Attorney General Letter On McKamey Manor Haunted HouseДокумент2 страницыTennessee Attorney General Letter On McKamey Manor Haunted HouseUSA TODAY Network100% (1)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Lundberg Proposed Amendment To SB2787 (013336)Документ17 страницLundberg Proposed Amendment To SB2787 (013336)USA TODAY NetworkОценок пока нет

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Tennessee Attorney General Letter On McKamey Manor Haunted HouseДокумент2 страницыTennessee Attorney General Letter On McKamey Manor Haunted HouseUSA TODAY Network100% (1)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Joshua Brown Arrest Warrant 65314a3a488cbДокумент4 страницыJoshua Brown Arrest Warrant 65314a3a488cbUSA TODAY NetworkОценок пока нет

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Daryl Hall DeclarationДокумент11 страницDaryl Hall DeclarationUSA TODAY Network100% (1)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Sewer Status Report January 31Документ25 страницSewer Status Report January 31Anthony WarrenОценок пока нет

- Majority OpinionДокумент17 страницMajority OpinionGabriela Guerrero100% (1)

- State v. Murdaugh - Motion To StayДокумент65 страницState v. Murdaugh - Motion To StayUSA TODAY Network100% (1)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Robert Thomas ComplaintДокумент17 страницRobert Thomas ComplaintFOX 17 News Digital Staff0% (1)

- Zac Bryan Arrest AffidavitДокумент4 страницыZac Bryan Arrest AffidavitUSA TODAY NetworkОценок пока нет

- Airport Authority Permit Boundary Letter To MetroДокумент7 страницAirport Authority Permit Boundary Letter To MetroUSA TODAY NetworkОценок пока нет

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- 2023-09-05 LTR To Adair Ford BoroughsДокумент2 страницы2023-09-05 LTR To Adair Ford BoroughsUSA TODAY Network100% (1)

- MNPS Equity Roadmap PDFДокумент40 страницMNPS Equity Roadmap PDFUSA TODAY NetworkОценок пока нет

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- 1005 Herrington LawsuitДокумент7 страниц1005 Herrington LawsuitAnna TurmanОценок пока нет

- 2023 Accountability Media FileДокумент21 страница2023 Accountability Media FileUSA TODAY NetworkОценок пока нет

- Fairgrounds Renovation Vote Threshold LawsuitДокумент11 страницFairgrounds Renovation Vote Threshold LawsuitUSA TODAY NetworkОценок пока нет

- Wingate OrderДокумент7 страницWingate Orderjordon.gray100% (1)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Fairgrounds Speedway CBA Urban League Bristol 2023Документ8 страницFairgrounds Speedway CBA Urban League Bristol 2023USA TODAY NetworkОценок пока нет

- Racetrack SuitДокумент11 страницRacetrack SuitAnita WadhwaniОценок пока нет

- Conspiracy, Deprivation of Rights, Destruction of Records IndictmentДокумент30 страницConspiracy, Deprivation of Rights, Destruction of Records IndictmentUSA TODAY NetworkОценок пока нет

- Bryant MT ComplaintДокумент27 страницBryant MT Complaintthe kingfishОценок пока нет

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Mississippi Press Association Better Newspaper Media Contest Awards For Work in 2022Документ30 страницMississippi Press Association Better Newspaper Media Contest Awards For Work in 2022USA TODAY NetworkОценок пока нет

- Third Grade Promotion TimelineДокумент2 страницыThird Grade Promotion TimelineUSA TODAY NetworkОценок пока нет

- Fin Acc Valix PDFДокумент58 страницFin Acc Valix PDFKyla Renz de LeonОценок пока нет

- Etextbook 978 1305947771 Century 21 Accounting General Journal Copyright UpdateДокумент61 страницаEtextbook 978 1305947771 Century 21 Accounting General Journal Copyright Updatemaryann.atkins290100% (42)

- Cfab 2022 Ag AnswersДокумент23 страницыCfab 2022 Ag AnswersShirah ShahrilОценок пока нет

- Prior Period Errors. These Are Intended To Enhance The Relevance, Reliability and Comparability of TheДокумент4 страницыPrior Period Errors. These Are Intended To Enhance The Relevance, Reliability and Comparability of TheJustine VeralloОценок пока нет

- RTP May 2018 New Gr1Документ122 страницыRTP May 2018 New Gr1subhanvts7781Оценок пока нет

- Business Strategy Using Financial Statements: Asset Analysis-Long-Lived Asset and DepreciationДокумент41 страницаBusiness Strategy Using Financial Statements: Asset Analysis-Long-Lived Asset and DepreciationMeena KhattakОценок пока нет

- Accounting 504 - Chapter 02 AnswersДокумент19 страницAccounting 504 - Chapter 02 AnswerspicassaaОценок пока нет

- Abridged Balance Sheet: AssetsДокумент18 страницAbridged Balance Sheet: AssetsMiguel RamosОценок пока нет

- DPR PackageДокумент29 страницDPR PackageAbhishek SharmaОценок пока нет

- Final Exam Economy.Документ2 страницыFinal Exam Economy.keith tambaОценок пока нет

- Credit Memo Ok Debit Memo Ok Debit MemoДокумент22 страницыCredit Memo Ok Debit Memo Ok Debit MemoVea Canlas CabertoОценок пока нет

- Set B Multiple Choice, Chapter 24 - Capital Investment AnalysisДокумент2 страницыSet B Multiple Choice, Chapter 24 - Capital Investment AnalysisJohn Carlos DoringoОценок пока нет

- Investing in Cambodia - FINALДокумент22 страницыInvesting in Cambodia - FINALleekosalОценок пока нет

- 001 Finished Book - Adjusting Entries - Amended.10.22.11Документ168 страниц001 Finished Book - Adjusting Entries - Amended.10.22.11William E. WestwoodОценок пока нет

- GM 19Документ3 страницыGM 19Bhavdeep singh sidhuОценок пока нет

- PCM Module 5 Notes-FinalДокумент8 страницPCM Module 5 Notes-FinalRevathiKumariОценок пока нет

- During The Current Year Blake Construction Disposed of Plant AssetsДокумент1 страницаDuring The Current Year Blake Construction Disposed of Plant Assetstrilocksp SinghОценок пока нет

- Financial Accounting and Reporting-IIДокумент5 страницFinancial Accounting and Reporting-IIHooriaОценок пока нет

- Intermediate Financial Accounting Study NotesДокумент23 страницыIntermediate Financial Accounting Study NotesSayTing ToonОценок пока нет

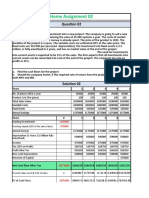

- Home Assignment 02: Total Sales Value Variable Costs Fixed Costs Annual Savings 1175000 1175000 1175000 1175000 1175000Документ2 страницыHome Assignment 02: Total Sales Value Variable Costs Fixed Costs Annual Savings 1175000 1175000 1175000 1175000 1175000Farzan Yahya HabibОценок пока нет

- Assignment I - Ashapura Minechem LimitedДокумент8 страницAssignment I - Ashapura Minechem LimitedSibika GadiaОценок пока нет

- Intangible MCДокумент49 страницIntangible MCAnonymous zpUO2SОценок пока нет

- PLDTДокумент16 страницPLDTPrince PerezОценок пока нет

- BC 202 Macro EconomicsДокумент171 страницаBC 202 Macro Economicsirfana hashmiОценок пока нет

- Inventories, Investments, Intangibles, & Property, Plant and Equipment - Quiz MaterialДокумент5 страницInventories, Investments, Intangibles, & Property, Plant and Equipment - Quiz MaterialMimiОценок пока нет

- Chapter 13 - Property, Plant, and Equipment: Depreciation and DepletionДокумент25 страницChapter 13 - Property, Plant, and Equipment: Depreciation and Depletionnavie VОценок пока нет

- Introduction To Accounting by Peter Scott Full ChapterДокумент41 страницаIntroduction To Accounting by Peter Scott Full Chapterjames.popp962100% (26)

- Amalgamation - Principles of AccountingДокумент4 страницыAmalgamation - Principles of AccountingAbdulla MaseehОценок пока нет

- PFS FINAL Chapter 1-7Документ36 страницPFS FINAL Chapter 1-7q24rzsxbr8Оценок пока нет

- Final Accounts of Banking Companies Problems and SolutionsДокумент27 страницFinal Accounts of Banking Companies Problems and Solutionsmy Vinay96% (57)

- You Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantОт EverandYou Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantРейтинг: 4 из 5 звезд4/5 (104)

- The Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsОт EverandThe Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsОценок пока нет

- ISO 27001 Controls – A guide to implementing and auditingОт EverandISO 27001 Controls – A guide to implementing and auditingРейтинг: 5 из 5 звезд5/5 (1)

- How To Budget And Manage Your Money In 7 Simple StepsОт EverandHow To Budget And Manage Your Money In 7 Simple StepsРейтинг: 5 из 5 звезд5/5 (4)

- Budget Management for Beginners: Proven Strategies to Revamp Business & Personal Finance Habits. Stop Living Paycheck to Paycheck, Get Out of Debt, and Save Money for Financial Freedom.От EverandBudget Management for Beginners: Proven Strategies to Revamp Business & Personal Finance Habits. Stop Living Paycheck to Paycheck, Get Out of Debt, and Save Money for Financial Freedom.Рейтинг: 5 из 5 звезд5/5 (89)

- Financial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassОт EverandFinancial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassОценок пока нет

- The Public School Advantage: Why Public Schools Outperform Private SchoolsОт EverandThe Public School Advantage: Why Public Schools Outperform Private SchoolsРейтинг: 4.5 из 5 звезд4.5/5 (3)

- The Best Team Wins: The New Science of High PerformanceОт EverandThe Best Team Wins: The New Science of High PerformanceРейтинг: 4.5 из 5 звезд4.5/5 (31)