Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Mercader v. DBPДокумент3 страницыMercader v. DBPReina MarieОценок пока нет

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Wooley v. Maynard Case BriefДокумент3 страницыWooley v. Maynard Case BriefReina MarieОценок пока нет

- First Batch DigestsДокумент9 страницFirst Batch DigestsReina MarieОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Tax DigestsДокумент16 страницTax DigestsReina MarieОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- PolicyДокумент5 страницPolicyRichard WijayaОценок пока нет

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

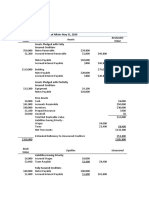

- Financial Accounting and Reporting Final ExaminationДокумент13 страницFinancial Accounting and Reporting Final ExaminationBernardino PacificAce100% (1)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- A Study On Financial Performance of Salem District Co-Operative Milk Producers Union Limited at SalemДокумент5 страницA Study On Financial Performance of Salem District Co-Operative Milk Producers Union Limited at Salemgvani3333Оценок пока нет

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Acc 101Документ24 страницыAcc 101Shyam RathiОценок пока нет

- Business Plan ShelbyДокумент44 страницыBusiness Plan ShelbyHạng VũОценок пока нет

- Unit 1 Sales & Distribution ManagementДокумент19 страницUnit 1 Sales & Distribution Managementमयंक पाण्डेयОценок пока нет

- Events Checklist 01Документ1 страницаEvents Checklist 01Neri ErinОценок пока нет

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- 2018 Compendium Volume 2 UpstreamДокумент437 страниц2018 Compendium Volume 2 UpstreamLoren SanapoОценок пока нет

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Managing RestructuringДокумент140 страницManaging RestructuringCollinson GrantОценок пока нет

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- ORGANISATION STRUCTURE TRAINING at Manjilas Double Horse For MBA Christ UniversityДокумент36 страницORGANISATION STRUCTURE TRAINING at Manjilas Double Horse For MBA Christ UniversityVishnu Raj86% (29)

- Mmpi v. Sec of DSWDДокумент18 страницMmpi v. Sec of DSWDArianneParalisanОценок пока нет

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Auditibg Problems Purchase CommitmentДокумент1 страницаAuditibg Problems Purchase Commitmentnivea gumayagay0% (1)

- Solution Chapter 13 ADVAC2Документ24 страницыSolution Chapter 13 ADVAC2Princess50% (2)

- Economics MCQДокумент36 страницEconomics MCQAnonymous WtjVcZCgОценок пока нет

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- 6.3. Burden of Out-Of-Pocket Health Expenditure: 6. Access To CareДокумент3 страницы6.3. Burden of Out-Of-Pocket Health Expenditure: 6. Access To CareNawaz RasoolОценок пока нет

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- 03 Financial AnalysisДокумент55 страниц03 Financial Analysisselcen sarıkayaОценок пока нет

- C4 PDFДокумент373 страницыC4 PDFIssa Adiema100% (4)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- INVENTORIESДокумент4 страницыINVENTORIESHANZ JOSHUA P ESTERBANОценок пока нет

- Review Patricia Crone S Book Arabia Without SpicesДокумент35 страницReview Patricia Crone S Book Arabia Without SpicesphotopemОценок пока нет

- Book Value Assets Realizable Value: Nama: Firda Arfianti NIM: 2301949596Документ2 страницыBook Value Assets Realizable Value: Nama: Firda Arfianti NIM: 2301949596FirdaОценок пока нет

- Caribbean Internet Café, CVP Analysis - Accurate EssaysДокумент2 страницыCaribbean Internet Café, CVP Analysis - Accurate EssaysVishali ChandrasekaranОценок пока нет

- HSC Commerce 2015 March BK PDFДокумент5 страницHSC Commerce 2015 March BK PDFShaiviОценок пока нет

- Test Bank For Financial Management Principles and Applications 10th Edition by KeownДокумент19 страницTest Bank For Financial Management Principles and Applications 10th Edition by KeownPria Aji PamungkasОценок пока нет

- Company Structure. Q1) A Company S Balance Sheet Shows The Following Capital StructureДокумент6 страницCompany Structure. Q1) A Company S Balance Sheet Shows The Following Capital StructureDullah AllyОценок пока нет

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Irrevocable Master Fee Protection Agreement IMFPA & NCNDAДокумент11 страницIrrevocable Master Fee Protection Agreement IMFPA & NCNDAMohamed E. Saber100% (4)

- The Murder of Sherry JacksonДокумент15 страницThe Murder of Sherry JacksonAhmed Hadi100% (1)

- BCG MatrixДокумент22 страницыBCG Matrixnomanfaisal1Оценок пока нет

- FIORI Apps in Simple FinanceДокумент13 страницFIORI Apps in Simple FinancesaavbОценок пока нет

- GrowRichPinoy E-BookДокумент59 страницGrowRichPinoy E-BookRose Ann63% (8)

- Chapter 12 Differential Analysis STDДокумент15 страницChapter 12 Differential Analysis STDjacks ocОценок пока нет