Вам также может понравиться

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Civil Law - Obligations & Contracts - Soriano Notes (Uribe Civil Law Review)Документ133 страницыCivil Law - Obligations & Contracts - Soriano Notes (Uribe Civil Law Review)freegalado95% (21)

- TAXREV SANTOSsyllabusДокумент7 страницTAXREV SANTOSsyllabusJoma CoronaОценок пока нет

- Sample Judicial AffДокумент6 страницSample Judicial AffJoma CoronaОценок пока нет

- Finals Study Sched 2017Документ2 страницыFinals Study Sched 2017Joma CoronaОценок пока нет

- Insurance ReviewerДокумент41 страницаInsurance Revieweroliefo100% (5)

- INS Batch 1 PDFДокумент30 страницINS Batch 1 PDFJoma CoronaОценок пока нет

- Specpro Last DigestsДокумент19 страницSpecpro Last DigestsJoma CoronaОценок пока нет

- Specpro DigestsДокумент46 страницSpecpro DigestsJoma CoronaОценок пока нет

- Specpro 2Документ43 страницыSpecpro 2Joma CoronaОценок пока нет

- HR Cases Post MTДокумент18 страницHR Cases Post MTJoma CoronaОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- 【2001】DS-PWA32 How to Add Wireless Control Panel to Hik-ConnectДокумент5 страниц【2001】DS-PWA32 How to Add Wireless Control Panel to Hik-ConnectLuis CastilloОценок пока нет

- HT101 - 1.2 Terminologies & Concept in Tourism & Hospitality IДокумент22 страницыHT101 - 1.2 Terminologies & Concept in Tourism & Hospitality IAnna UngОценок пока нет

- HSBC KM25502451 - StatementДокумент2 страницыHSBC KM25502451 - StatementbunnyОценок пока нет

- Module 3Документ127 страницModule 3nidhi goelОценок пока нет

- 0 - Anjali Sah AccountancyДокумент16 страниц0 - Anjali Sah AccountancySushmita BarlaОценок пока нет

- Autosweep Sept 1-Oct 16Документ44 страницыAutosweep Sept 1-Oct 16Genevieve-LhangLatorenoОценок пока нет

- Financing RequirementДокумент5 страницFinancing RequirementZinck HansenОценок пока нет

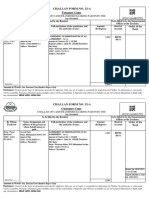

- Challan Form No. 32-A Treasury Copy: Challan of Cash/Transfer/Clearing Paid Into TheДокумент1 страницаChallan Form No. 32-A Treasury Copy: Challan of Cash/Transfer/Clearing Paid Into TheNoman Malik100% (2)

- Everest Group - Aware (Intelligent) IT Infrastructure Services Automation - Service Provider Compendium 2021 - CAДокумент9 страницEverest Group - Aware (Intelligent) IT Infrastructure Services Automation - Service Provider Compendium 2021 - CABschool caseОценок пока нет

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceДокумент24 страницыStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balancerizwana mukatiОценок пока нет

- PrathmeshДокумент5 страницPrathmeshprathmesh vaidyaОценок пока нет

- Alibaba Case Study Mid-Term ExamДокумент20 страницAlibaba Case Study Mid-Term ExamAudley R Grimes100% (5)

- VH7 IBZy JEQLl 4 NQXДокумент14 страницVH7 IBZy JEQLl 4 NQXmadhur chavanОценок пока нет

- Money and Banking NotesДокумент8 страницMoney and Banking NotesAdwaith c AnandОценок пока нет

- Urban MobilityДокумент2 страницыUrban MobilityHafiey EyzaОценок пока нет

- PunjabPolice DS PDFДокумент1 страницаPunjabPolice DS PDFHamza SheikhОценок пока нет

- Authorization Letter: Guidelines For LabsДокумент2 страницыAuthorization Letter: Guidelines For LabsshahaОценок пока нет

- GS Select InformationДокумент4 страницыGS Select InformationCrowdfundInsiderОценок пока нет

- Advertising PlaybookДокумент53 страницыAdvertising PlaybookMariana FerronatoОценок пока нет

- Alliance To Buy Reno's Sierra Design GroupДокумент2 страницыAlliance To Buy Reno's Sierra Design Groupkupa7Оценок пока нет

- Linkhub hh70vhДокумент35 страницLinkhub hh70vhMax LedererОценок пока нет

- Bank Audit-1.Документ7 страницBank Audit-1.Venkatraman ThiyagarajanОценок пока нет

- The Primary, Secondary and Tertiary Health Sectors in New Zealand With Specific Reference To Mental HealthДокумент5 страницThe Primary, Secondary and Tertiary Health Sectors in New Zealand With Specific Reference To Mental Healthfarah gohar100% (4)

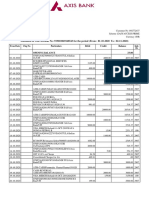

- Statement of Axis Account No:919010069168543 For The Period (From: 01-10-2020 To: 02-11-2020)Документ2 страницыStatement of Axis Account No:919010069168543 For The Period (From: 01-10-2020 To: 02-11-2020)minniОценок пока нет

- Auditing and Assurance Services Chapter 1Документ1 страницаAuditing and Assurance Services Chapter 1rathana_chea0% (1)

- Extras de Cont / Account: 2. Valuta / Currency 3. Data Extras / Statement DateДокумент2 страницыExtras de Cont / Account: 2. Valuta / Currency 3. Data Extras / Statement DateVictor Victor GruescuОценок пока нет

- Chapter 13: Retailers, Wholesalers, & Their Strategy PlanningДокумент24 страницыChapter 13: Retailers, Wholesalers, & Their Strategy PlanningKhánh MaiОценок пока нет

- Anthony Olvera - Psa Brochure Assignment - 4682908Документ5 страницAnthony Olvera - Psa Brochure Assignment - 4682908api-501232916Оценок пока нет

- Retail Shop Management: Unit - IvДокумент66 страницRetail Shop Management: Unit - IvmanopavanОценок пока нет

- Travelport Galileo Document Production Manual - 19 3Документ111 страницTravelport Galileo Document Production Manual - 19 3fauza0% (1)