Вам также может понравиться

- Betterworks Goal Setting Ebook PDFДокумент13 страницBetterworks Goal Setting Ebook PDFArtur Furtado100% (3)

- International Marketing Research: A Global Project Management PerspectiveДокумент10 страницInternational Marketing Research: A Global Project Management Perspectivelifeis1enjoyОценок пока нет

- Literature Review About Marketing Strategies and A Firms PerformanceДокумент7 страницLiterature Review About Marketing Strategies and A Firms PerformanceBabur Farrukh76% (34)

- Lunar Rubbers PVT LTDДокумент76 страницLunar Rubbers PVT LTDSabeer Hamsa67% (3)

- Handbook for Strategic HR - Section 7: Globalization, Cross-Cultural Interaction, and Virtual Working ArrangementsОт EverandHandbook for Strategic HR - Section 7: Globalization, Cross-Cultural Interaction, and Virtual Working ArrangementsОценок пока нет

- The Entrepreneurial ProcessДокумент13 страницThe Entrepreneurial ProcessNgoni Mukuku100% (1)

- Debt Collector Disclosure StatementДокумент8 страницDebt Collector Disclosure StatementGreg WilderОценок пока нет

- Competitive Strategy: Techniques for Analyzing Industries and CompetitorsОт EverandCompetitive Strategy: Techniques for Analyzing Industries and CompetitorsРейтинг: 4.5 из 5 звезд4.5/5 (31)

- International Pricing StrategyДокумент16 страницInternational Pricing StrategyJobeer DahmanОценок пока нет

- Internationalization and Firm Performance: Meta-Analytic Review and Future Research DirectionsДокумент62 страницыInternationalization and Firm Performance: Meta-Analytic Review and Future Research DirectionsAbhishek Singh100% (1)

- GRC Expert - User Access Reviews1Документ11 страницGRC Expert - User Access Reviews1Rohit KumarОценок пока нет

- Iso 37001 Anti Bribery Mss PDFДокумент5 страницIso 37001 Anti Bribery Mss PDFDana NedeaОценок пока нет

- 115 Practical SAP HANA ABAP Interview Q&AДокумент25 страниц115 Practical SAP HANA ABAP Interview Q&AsuryaОценок пока нет

- Constitutional Provisions For Labor Law PhilippinesДокумент1 страницаConstitutional Provisions For Labor Law PhilippinesAgnes GamboaОценок пока нет

- Lazaro Vs SSSДокумент2 страницыLazaro Vs SSSFatima Briones100% (1)

- Appointment Letter To A Clerk, Office AssistantДокумент2 страницыAppointment Letter To A Clerk, Office AssistantPalash Banerjee80% (5)

- 13 JurnalДокумент7 страниц13 JurnalHaidar BugzОценок пока нет

- International Pricing StrategyДокумент16 страницInternational Pricing StrategyArkadeep Paul ChoudhuryОценок пока нет

- Interfunctional Dynamics and Firm Performance: A Comparison Between Firms in Poland and The United StatesДокумент19 страницInterfunctional Dynamics and Firm Performance: A Comparison Between Firms in Poland and The United StatesLeila BenmansourОценок пока нет

- JHD DP 2011-003Документ46 страницJHD DP 2011-003s_arshad12Оценок пока нет

- Organizing and Implementing Export Pricing: Performance Effects and Moderating FactorsДокумент21 страницаOrganizing and Implementing Export Pricing: Performance Effects and Moderating FactorsPetru FercalОценок пока нет

- 04 Khan Et AlДокумент23 страницы04 Khan Et AlEngr Fizza AkbarОценок пока нет

- Marketing Mix and Brand Sales in Global Markets - Examining The CoДокумент48 страницMarketing Mix and Brand Sales in Global Markets - Examining The CovyapakОценок пока нет

- 2017 JIntlMktg ChabowskiMena Oct2017 PDFДокумент26 страниц2017 JIntlMktg ChabowskiMena Oct2017 PDFPranav SharmaОценок пока нет

- 08 - Chapter 2 PDFДокумент21 страница08 - Chapter 2 PDFJAI SHANKAR 2Оценок пока нет

- Effects On Innovation and Firm Performance in Product-Diversified FirmsДокумент33 страницыEffects On Innovation and Firm Performance in Product-Diversified FirmsThảo LưuОценок пока нет

- 2010 BJM Gonzalez-PadronChabowskiHultKetchen Nov2010Документ17 страниц2010 BJM Gonzalez-PadronChabowskiHultKetchen Nov2010janrivai adimanОценок пока нет

- SSRN Id961477Документ51 страницаSSRN Id961477AGBA NJI THOMASОценок пока нет

- Zabkar@uni-Lj - Si Maja - Makovec@uni-Lj - SiДокумент20 страницZabkar@uni-Lj - Si Maja - Makovec@uni-Lj - SiAna SyazanaОценок пока нет

- Purpose: What Are They Researching, 2-What Is The Core and Embedded Questions They Are Trying To Answer, 3-What Are The Hypotheses They Are Trying To Test or Prove and 4-WhyДокумент7 страницPurpose: What Are They Researching, 2-What Is The Core and Embedded Questions They Are Trying To Answer, 3-What Are The Hypotheses They Are Trying To Test or Prove and 4-Whyazade azamiОценок пока нет

- SSRN Id881841Документ46 страницSSRN Id881841Yash GuptaОценок пока нет

- JIM Lages Silva Styles 2009Документ24 страницыJIM Lages Silva Styles 2009beriОценок пока нет

- The Relationship Between Manufacturing Integration and Performance From An Activity-Oriented PerspectiveДокумент19 страницThe Relationship Between Manufacturing Integration and Performance From An Activity-Oriented PerspectiveHélio Oliveira FerrariОценок пока нет

- Levels of StrategyДокумент37 страницLevels of StrategyMelessa AtkinsonОценок пока нет

- Mergers AcquisitionsДокумент41 страницаMergers AcquisitionsEmmanuel Bedjina MadjiteyОценок пока нет

- Cultural vs. Operational Market Orientation and Objective vs. Subjective Performance: Perspective of Production and OperationsДокумент33 страницыCultural vs. Operational Market Orientation and Objective vs. Subjective Performance: Perspective of Production and Operationssamas7480Оценок пока нет

- Growth Willingness and Market Orientation As Antecedents of Brand OrientationДокумент9 страницGrowth Willingness and Market Orientation As Antecedents of Brand OrientationmikhakjОценок пока нет

- Power MarketДокумент21 страницаPower MarketCẩm Anh ĐỗОценок пока нет

- GlobalizationДокумент53 страницыGlobalizationGaurav JainОценок пока нет

- Where To Internationalise and Why - Country Selection byДокумент11 страницWhere To Internationalise and Why - Country Selection byoscarmpabon248Оценок пока нет

- Grin Stein 2007Документ8 страницGrin Stein 2007indriОценок пока нет

- S. Promosi 1Документ23 страницыS. Promosi 1Nofi Nur AmalinaОценок пока нет

- Critical Analysis of Strategic Aspects of IKEA and McDonaldsДокумент13 страницCritical Analysis of Strategic Aspects of IKEA and McDonaldsIsiaku E Jimmy-Braimah100% (1)

- Lin 2014Документ7 страницLin 2014david herrera sotoОценок пока нет

- Determinants of SME Brand Adaptation in Global MarketingДокумент34 страницыDeterminants of SME Brand Adaptation in Global MarketingAbdul GhaniОценок пока нет

- Economics and Political EconomyДокумент22 страницыEconomics and Political Economyfisayobabs11Оценок пока нет

- Westjohn & Magnusson 2017 Adaptation Strategy Laws & Marketing MixДокумент19 страницWestjohn & Magnusson 2017 Adaptation Strategy Laws & Marketing MixShannaОценок пока нет

- Journal of World Business: David A. Griffith, Goksel Yalcinkaya, Roger J. CalantoneДокумент11 страницJournal of World Business: David A. Griffith, Goksel Yalcinkaya, Roger J. CalantonewolfОценок пока нет

- Rah Edu 1841Документ9 страницRah Edu 1841Makhdoom Zain Ul AbdinОценок пока нет

- Software Firm Evolution and Innovation-OrientationДокумент25 страницSoftware Firm Evolution and Innovation-Orientationapi-3851548Оценок пока нет

- Julian Et Al-2014-Thunderbird International Business ReviewДокумент14 страницJulian Et Al-2014-Thunderbird International Business ReviewNicОценок пока нет

- A ContingencyДокумент35 страницA ContingencyVinu JosephОценок пока нет

- Are Growing SMEs More Market-Oriented and Brand-Oriented?Документ18 страницAre Growing SMEs More Market-Oriented and Brand-Oriented?Dana NedeaОценок пока нет

- 9393 - Lancioni Schau Smith Intra b2b PricingДокумент9 страниц9393 - Lancioni Schau Smith Intra b2b PricingVaibhav JainОценок пока нет

- Ikea Ki Kya Aat GeДокумент37 страницIkea Ki Kya Aat GeFurqangreatОценок пока нет

- Factors Influencing Brand Launch in A GLДокумент15 страницFactors Influencing Brand Launch in A GLBenedictus Rosario ArdeliantoОценок пока нет

- A Global Market Advantage Framework The Role of Global Market Knowledge CompetenciesДокумент19 страницA Global Market Advantage Framework The Role of Global Market Knowledge CompetenciesWesam AlaghaОценок пока нет

- Industrial Marketing Management: Anna Kaleka, Neil A. MorganДокумент14 страницIndustrial Marketing Management: Anna Kaleka, Neil A. MorganHendriОценок пока нет

- Strategic Marketing Patterns and Performance ImplicationsДокумент26 страницStrategic Marketing Patterns and Performance Implicationsfajriatinazula02Оценок пока нет

- Palgrave Jibs 8491006Документ19 страницPalgrave Jibs 8491006midmlcepeajaeargieОценок пока нет

- Marketing Resources Globalization and PerformanceДокумент16 страницMarketing Resources Globalization and Performancezeebee17Оценок пока нет

- Resumo AlargadoДокумент10 страницResumo AlargadoAnoushkaBanavarОценок пока нет

- Marketing StrategyДокумент13 страницMarketing StrategyBoОценок пока нет

- Strategic Agility, Environmental Uncertainties and International PerformanceДокумент13 страницStrategic Agility, Environmental Uncertainties and International PerformanceMohamed AdelОценок пока нет

- The Effect of Marketing Efficiency, Brand Equity and Customer Satisfaction On Firm PerformanceДокумент21 страницаThe Effect of Marketing Efficiency, Brand Equity and Customer Satisfaction On Firm PerformanceSenzo MbewaОценок пока нет

- The Regional and Global Competitiveness of Multinational FirmsДокумент18 страницThe Regional and Global Competitiveness of Multinational FirmsalexaОценок пока нет

- The Impact of Sales Promotion On Brand EДокумент14 страницThe Impact of Sales Promotion On Brand ESunny SinghalОценок пока нет

- Strategy, Value and Risk: Industry Dynamics and Advanced Financial ManagementОт EverandStrategy, Value and Risk: Industry Dynamics and Advanced Financial ManagementОценок пока нет

- Concentration and Price-Cost Margins in Manufacturing IndustriesОт EverandConcentration and Price-Cost Margins in Manufacturing IndustriesОценок пока нет

- Brand Extension Effects On Brand Equity: A Cross-National StudyДокумент20 страницBrand Extension Effects On Brand Equity: A Cross-National StudyBatica MitrovicОценок пока нет

- Brand Social PowerДокумент32 страницыBrand Social PowerBatica MitrovicОценок пока нет

- Consumer Based GloblaДокумент20 страницConsumer Based GloblaBatica MitrovicОценок пока нет

- Effect Ofnon ProfitДокумент16 страницEffect Ofnon ProfitBatica MitrovicОценок пока нет

- Tarbucks Brand Equity Innovation Brand Image: Keywords: SДокумент13 страницTarbucks Brand Equity Innovation Brand Image: Keywords: SBatica MitrovicОценок пока нет

- Drivers of Brand EquityДокумент6 страницDrivers of Brand EquityBatica MitrovicОценок пока нет

- Ad Tracking, Brand Equity Research, and - . - Your Honors Program?Документ12 страницAd Tracking, Brand Equity Research, and - . - Your Honors Program?Batica MitrovicОценок пока нет

- Consumer Based Brand EquityДокумент25 страницConsumer Based Brand EquityBatica Mitrovic100% (1)

- Integrated Brand EquityДокумент19 страницIntegrated Brand EquityBatica MitrovicОценок пока нет

- Communication and Brand KnowledgeДокумент16 страницCommunication and Brand KnowledgeBatica MitrovicОценок пока нет

- Monitoring The Dynamics of Brand Equity Using Store-Level DataДокумент18 страницMonitoring The Dynamics of Brand Equity Using Store-Level DataBatica MitrovicОценок пока нет

- K Q1 10 Printable SlidesДокумент10 страницK Q1 10 Printable SlidesBatica MitrovicОценок пока нет

- Brand Equity Professional ServicesДокумент4 страницыBrand Equity Professional ServicesBatica MitrovicОценок пока нет

- Holistic View of Brand - 4.07Документ9 страницHolistic View of Brand - 4.07Batica MitrovicОценок пока нет

- Kellogg Company Full AR and 10KДокумент82 страницыKellogg Company Full AR and 10KBatica MitrovicОценок пока нет

- Docs 3584505 Kellogg S-MarketingДокумент2 страницыDocs 3584505 Kellogg S-MarketingBatica MitrovicОценок пока нет

- Chapter 1Документ4 страницыChapter 1Micaela BakerОценок пока нет

- XII Acc CH 4 and 5 Study Material 2024Документ28 страницXII Acc CH 4 and 5 Study Material 2024bhawanar674Оценок пока нет

- ADS Landscape RecommendationsДокумент7 страницADS Landscape Recommendationslkumar_inОценок пока нет

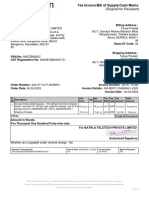

- InvoiceДокумент1 страницаInvoicetanya.prasadОценок пока нет

- Mms-Ente-Case StudyДокумент2 страницыMms-Ente-Case Studyvivek ghatbandheОценок пока нет

- Chapter 1 Global ServiceДокумент23 страницыChapter 1 Global ServiceRandeep SinghОценок пока нет

- Part One: Overture and Pageantry: TenderlyДокумент3 страницыPart One: Overture and Pageantry: TenderlyEneas Augusto100% (1)

- Construction International Innovation Ability - The Mode of Huawei Abstract After Reviewing Huawei's Twenty Years of Innovation andДокумент1 страницаConstruction International Innovation Ability - The Mode of Huawei Abstract After Reviewing Huawei's Twenty Years of Innovation andDwitya AribawaОценок пока нет

- Test Bank For Financial Reporting and Analysis 13th Edition Charles H GibsonДокумент36 страницTest Bank For Financial Reporting and Analysis 13th Edition Charles H Gibsonbdelliumtiliairwoct100% (42)

- Appendix V-Honda CSR 003Документ11 страницAppendix V-Honda CSR 003SowdayyaОценок пока нет

- OTS Prepay and Valuing Individual Mortgage Servicing Contracts - A Comparison Between Adjust Rate Mortgages and Fixed Rate MortgagesДокумент16 страницOTS Prepay and Valuing Individual Mortgage Servicing Contracts - A Comparison Between Adjust Rate Mortgages and Fixed Rate MortgagesfhdeutschmannОценок пока нет

- Online Shopping and Its ImpactДокумент33 страницыOnline Shopping and Its ImpactAkhil MohananОценок пока нет

- 4b18 PDFДокумент5 страниц4b18 PDFAnonymous lN5DHnehwОценок пока нет

- Wordpress - The StoryДокумент3 страницыWordpress - The Storydinucami62Оценок пока нет

- Analysis On Apollo Tyres LTDДокумент43 страницыAnalysis On Apollo Tyres LTDCHAITANYA ANNEОценок пока нет

- DP World Internship ReportДокумент40 страницDP World Internship ReportSaurabh100% (1)

- Jafza Rules 6th Edition 2016Документ58 страницJafza Rules 6th Edition 2016Binoy PsОценок пока нет

- Data Warehousing & DATA MINING (SE-409) : Lecture-2Документ36 страницData Warehousing & DATA MINING (SE-409) : Lecture-2Huma Qayyum MohyudDinОценок пока нет

- Gain Sheet - 2020 - FormatДокумент5 страницGain Sheet - 2020 - FormatMohd MazidОценок пока нет

- EXPORTДокумент99 страницEXPORTdhruv81275Оценок пока нет