Вам также может понравиться

- Shorting Home Equity Mezzanine TranchesДокумент73 страницыShorting Home Equity Mezzanine Tranchesسید ہارون حیدر گیلانیОценок пока нет

- ACCA F7 Mock Exam QuestionsДокумент18 страницACCA F7 Mock Exam QuestionsGeo Don100% (1)

- CFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)От EverandCFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)Рейтинг: 5 из 5 звезд5/5 (1)

- Investment PropertyДокумент7 страницInvestment PropertyKate Fernandez50% (4)

- Basic Debt Reduction Snowball - TemplateДокумент41 страницаBasic Debt Reduction Snowball - TemplatetognibeneОценок пока нет

- Receivables ProblemsДокумент13 страницReceivables ProblemsIris Mnemosyne0% (1)

- Module 13 Notes Payable - Debt ResructuringДокумент10 страницModule 13 Notes Payable - Debt ResructuringryanОценок пока нет

- Britannia Industries Ltd. (India) Ratio AnalysisДокумент35 страницBritannia Industries Ltd. (India) Ratio AnalysisMansiShahОценок пока нет

- 2019 UVA-FRS AND All HC ContractsДокумент241 страница2019 UVA-FRS AND All HC ContractsMatt BrownОценок пока нет

- Black Box WorkbookДокумент381 страницаBlack Box Workbookznhtogex33% (3)

- 1 - Summary - Inside Job - IntroductionДокумент7 страниц1 - Summary - Inside Job - IntroductionArslan ArainОценок пока нет

- Chapters 7 and 8 EditedДокумент20 страницChapters 7 and 8 Editedomar_geryesОценок пока нет

- Quizzer 1Документ4 страницыQuizzer 1Arvin John MasuelaОценок пока нет

- Drills Acc 108 Sem EnderДокумент10 страницDrills Acc 108 Sem Enderbrmo.amatorio.uiОценок пока нет

- 9.liability Questionnaire QUIZДокумент10 страниц9.liability Questionnaire QUIZMark GaerlanОценок пока нет

- 103 CompilationДокумент12 страниц103 CompilationLyn AbudaОценок пока нет

- Afar QuestionsДокумент16 страницAfar Questionspopsie tulalianОценок пока нет

- Financial Accounting IIДокумент16 страницFinancial Accounting IIMiguel BuenoОценок пока нет

- Financial Accounting IIДокумент16 страницFinancial Accounting IIMiguel BuenoОценок пока нет

- CPA ReviewДокумент14 страницCPA ReviewnikkaaaОценок пока нет

- Acc204 Midterm Exam Set BДокумент5 страницAcc204 Midterm Exam Set BJudy Ann Imus0% (1)

- ASSET 2019 Mock Boards - FARДокумент7 страницASSET 2019 Mock Boards - FARKenneth Christian WilburОценок пока нет

- Ia 2 Compilation of Quiz and ExercisesДокумент16 страницIa 2 Compilation of Quiz and ExercisesclairedennprztananОценок пока нет

- ACCExpanded Opportunity Part 1Документ4 страницыACCExpanded Opportunity Part 1Hilarie JeanОценок пока нет

- MC FinalДокумент14 страницMC Finalahmed arfanОценок пока нет

- Intermediate 1Документ11 страницIntermediate 1Mary Anne ManaoisОценок пока нет

- Gen008 P1 ExamДокумент11 страницGen008 P1 ExamMary Lyn DatuinОценок пока нет

- AFAR FinalMockBoard AДокумент11 страницAFAR FinalMockBoard ACattleyaОценок пока нет

- 2nd Yr Midterm (2nd Sem) ReviewerДокумент19 страниц2nd Yr Midterm (2nd Sem) ReviewerC H ♥ N T Z60% (5)

- Instructions: Answer The Following Carefully. Highlight Your Answer With Color Yellow. AfterДокумент9 страницInstructions: Answer The Following Carefully. Highlight Your Answer With Color Yellow. AfterMIKASAОценок пока нет

- Far Review - Notes and Receivable AssessmentДокумент6 страницFar Review - Notes and Receivable AssessmentLuisa Janelle BoquirenОценок пока нет

- Prelim Lecture 1 Assignment: Multiple ChoiceДокумент4 страницыPrelim Lecture 1 Assignment: Multiple Choicelinkin soyОценок пока нет

- Intermediate AccountingДокумент9 страницIntermediate AccountingpolxrixОценок пока нет

- Audit of Liabilities QuizДокумент2 страницыAudit of Liabilities QuizCattleyaОценок пока нет

- Problems - Docx 1Документ25 страницProblems - Docx 1You Knock On My DoorОценок пока нет

- Financial Accounting Vol. 2 Example QuestionsДокумент8 страницFinancial Accounting Vol. 2 Example QuestionsMarisolОценок пока нет

- FAR First Pre BoardДокумент18 страницFAR First Pre BoardKIM RAGAОценок пока нет

- Acc 108 Emp Bene. Bonus Debt RestrДокумент2 страницыAcc 108 Emp Bene. Bonus Debt Restrbrmo.amatorio.uiОценок пока нет

- 206B 3rd Preboard ActivityДокумент9 страниц206B 3rd Preboard ActivityJERROLD EIRVIN PAYOPAYОценок пока нет

- AFAR FinalMockBoard BДокумент11 страницAFAR FinalMockBoard BCattleyaОценок пока нет

- Review Session1-MidtermДокумент7 страницReview Session1-MidtermBich VietОценок пока нет

- Chapter 1 - LiabilitiesДокумент8 страницChapter 1 - LiabilitiesHerrika Red Gullon RoseteОценок пока нет

- Financial Accounting Midterm ExamДокумент20 страницFinancial Accounting Midterm ExamkimkimОценок пока нет

- Level 1 AVERAGEДокумент4 страницыLevel 1 AVERAGEJaime II LustadoОценок пока нет

- Self Test 9 - LiabilitiesДокумент4 страницыSelf Test 9 - LiabilitiesBasketball WorldОценок пока нет

- Self Test 9 - LiabilitiesДокумент4 страницыSelf Test 9 - LiabilitiesLennier ArvinОценок пока нет

- Compre23 FARДокумент12 страницCompre23 FARchristinemariet.ramirezОценок пока нет

- Usc Part 2020 (Far) - RetakeДокумент25 страницUsc Part 2020 (Far) - RetakeVince AbabonОценок пока нет

- Accounting For Income Tax ExamДокумент6 страницAccounting For Income Tax ExamAnn Christine C. Chua100% (2)

- FAR Summary Lecture (14 May 2021)Документ10 страницFAR Summary Lecture (14 May 2021)rav danoОценок пока нет

- AUDIT PROBS-2nd MONTHLY ASSESSMENTДокумент7 страницAUDIT PROBS-2nd MONTHLY ASSESSMENTGRACELYN SOJORОценок пока нет

- Semi-Finals Financial Accounting and ReportingДокумент23 страницыSemi-Finals Financial Accounting and Reportingjoyce KimОценок пока нет

- FA - Adjusting EntriesДокумент14 страницFA - Adjusting EntriesaleezaОценок пока нет

- QUIZ-current Liability TEACHERДокумент3 страницыQUIZ-current Liability TEACHERpadayonmhieОценок пока нет

- Orca Share Media1605010109407 6731900321930361605Документ37 страницOrca Share Media1605010109407 6731900321930361605MARY JUSTINE PAQUIBOTОценок пока нет

- Quiz-Current Liability MULTIPLE CHOICE. Select The Best Answer For Each of The Following QuestionsДокумент3 страницыQuiz-Current Liability MULTIPLE CHOICE. Select The Best Answer For Each of The Following QuestionsNicole Anne Santiago Sibulo0% (1)

- Intermediate Accounting 2 Reviewer PDFДокумент133 страницыIntermediate Accounting 2 Reviewer PDFCarl CagampzОценок пока нет

- D. Discounted - YES Pledged - NOДокумент9 страницD. Discounted - YES Pledged - NOJasper LuagueОценок пока нет

- AfarДокумент18 страницAfarFleo GardivoОценок пока нет

- Borrowing Cost Problem Solutions - CompressДокумент16 страницBorrowing Cost Problem Solutions - CompressSyreОценок пока нет

- Compre 2 - Far1Документ5 страницCompre 2 - Far1Mary Alyssa Claire Capate IIОценок пока нет

- Quiz Intermediate Accounting 1Документ3 страницыQuiz Intermediate Accounting 1Pineda, King Moises PangilinanОценок пока нет

- 2ND Online Quiz Level 1 Set B (Answers)Документ5 страниц2ND Online Quiz Level 1 Set B (Answers)Vincent Larrie Moldez100% (1)

- Final Exam Cfas WoДокумент11 страницFinal Exam Cfas WoAndrei GoОценок пока нет

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionОт EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionОценок пока нет

- A Comparative Analysis of Tax Administration in Asia and the Pacific: 2016 EditionОт EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: 2016 EditionОценок пока нет

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionОт EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionОценок пока нет

- A Comparative Analysis of Tax Administration in Asia and the Pacific-Seventh EditionОт EverandA Comparative Analysis of Tax Administration in Asia and the Pacific-Seventh EditionОценок пока нет

- CASE 3 Managers Have FeelingsДокумент1 страницаCASE 3 Managers Have FeelingsKate FernandezОценок пока нет

- Third Exam QuizzerДокумент1 страницаThird Exam QuizzerKate FernandezОценок пока нет

- BM 100 Journal Writing - FernandezДокумент9 страницBM 100 Journal Writing - FernandezKate FernandezОценок пока нет

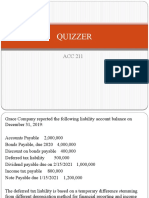

- Acc 223 1ST ExamДокумент3 страницыAcc 223 1ST ExamKate FernandezОценок пока нет

- Acc 211 Activity - Debt RestructuringДокумент1 страницаAcc 211 Activity - Debt RestructuringKate FernandezОценок пока нет

- ACC 211 - Seventh QuizzerДокумент1 страницаACC 211 - Seventh QuizzerKate FernandezОценок пока нет

- LIABILITIESДокумент5 страницLIABILITIESKate FernandezОценок пока нет

- Government Accounting QuizДокумент2 страницыGovernment Accounting QuizKate Fernandez100% (2)

- Gujarat Microwax R 02032017Документ6 страницGujarat Microwax R 02032017Saurabh JainОценок пока нет

- CA Short Form Deed of TrustДокумент3 страницыCA Short Form Deed of TrustAxisvipОценок пока нет

- Students and Money Management Behavior of A Malaysian Public UniversityДокумент9 страницStudents and Money Management Behavior of A Malaysian Public UniversityjoyОценок пока нет

- Accounting Research Journal September 2015Документ25 страницAccounting Research Journal September 2015Firehun GichiloОценок пока нет

- Compound InterestДокумент35 страницCompound InterestToukaОценок пока нет

- C C CCC C CCCCCCCC CДокумент45 страницC C CCC C CCCCCCCC Cdevraj537853Оценок пока нет

- TIRSA Rate ManualДокумент266 страницTIRSA Rate ManualcsadkinsОценок пока нет

- CT Pret 2Документ1 страницаCT Pret 2Ablo AblaОценок пока нет

- SIP (Aayush)Документ59 страницSIP (Aayush)Aayush PasawalaОценок пока нет

- Economics 1st Edition Karlan Test BankДокумент35 страницEconomics 1st Edition Karlan Test Banksalariedshopbook.gczx100% (31)

- Financial Statement Analysis - CPARДокумент13 страницFinancial Statement Analysis - CPARxxxxxxxxx100% (2)

- McLeavey, Dennis W. - Solnik, Bruno H - Global Investments (2013 - 2014, Pearson) - Libgen - LiДокумент591 страницаMcLeavey, Dennis W. - Solnik, Bruno H - Global Investments (2013 - 2014, Pearson) - Libgen - Liphoebe8soh100% (1)

- CocДокумент47 страницCocUmesh ChandraОценок пока нет

- Pidilite Industries Management Accounting Ratio Analysis Project FileДокумент180 страницPidilite Industries Management Accounting Ratio Analysis Project FileAlok jha100% (4)

- 9105 - Corporate LiquidationДокумент4 страницы9105 - Corporate LiquidationGo FarОценок пока нет

- SMC-SEC FORM 17-A (04.25.2022) Part 2-FINAL - RemovedДокумент182 страницыSMC-SEC FORM 17-A (04.25.2022) Part 2-FINAL - RemovedJM MontanoОценок пока нет

- Via E-Mail To Rule-Comments@sec - Gov: ASSOCIATION YEAR 2010-2011 ChairДокумент7 страницVia E-Mail To Rule-Comments@sec - Gov: ASSOCIATION YEAR 2010-2011 ChairMarketsWikiОценок пока нет

- Punjab National Bank Versus Surendra Prasad SinhaДокумент6 страницPunjab National Bank Versus Surendra Prasad SinhaHimanshu MishraОценок пока нет

- Correspondence With Shareholders and Debenture Holders Relating To Dividends and Interest, Transfer and TransmissionДокумент4 страницыCorrespondence With Shareholders and Debenture Holders Relating To Dividends and Interest, Transfer and TransmissiondaiarisaОценок пока нет

- Santosh Shekar ShettyДокумент6 страницSantosh Shekar ShettyAnurag MishraОценок пока нет

- 4 Valuation of SecuritiesДокумент13 страниц4 Valuation of SecuritiesPhạm Trần Thanh TúОценок пока нет

- Y Combinator Guide To Seed FundraisingДокумент12 страницY Combinator Guide To Seed FundraisingOluwasegun OluwaletiОценок пока нет

- Financial Statements and Ratio Analysis NEWДокумент108 страницFinancial Statements and Ratio Analysis NEWDina Adel DawoodОценок пока нет