Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Solution Manual For Case Studies in Finance 8th BrunerДокумент8 страницSolution Manual For Case Studies in Finance 8th BrunerKeith Estrada100% (39)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- 2019 Survey of VC & PE FundsДокумент88 страниц2019 Survey of VC & PE FundsFazlur TSP100% (1)

- StudyQuestions 080118Документ6 страницStudyQuestions 080118Jamie Ross0% (3)

- Gaspar@essec - Edu, Bonville@essec - Edu: Playing The Field: Competing Bids For Anadarko PetroleumДокумент1 страницаGaspar@essec - Edu, Bonville@essec - Edu: Playing The Field: Competing Bids For Anadarko PetroleumSanjana AkkireddyОценок пока нет

- Cfi Business Valuation Modeling Final AssessmentДокумент3 страницыCfi Business Valuation Modeling Final AssessmentKARTHIK100% (2)

- Chapter 6 - Portfolio Evaluation and RevisionДокумент26 страницChapter 6 - Portfolio Evaluation and RevisionShahrukh ShahjahanОценок пока нет

- Solution of Finanical Statement AnalysisДокумент14 страницSolution of Finanical Statement AnalysisMUHAMMAD AZAM100% (2)

- Engineering Economic Analysis 13th Edition Ebook PDFДокумент41 страницаEngineering Economic Analysis 13th Edition Ebook PDFkaty.wilkins325100% (30)

- Using The Sociotechnical Approach in Global Software Developments: Is The Theory Relevant Today?Документ12 страницUsing The Sociotechnical Approach in Global Software Developments: Is The Theory Relevant Today?pankajpandeylkoОценок пока нет

- State of Punjab Vs Naib Din On 28 September, 2001Документ4 страницыState of Punjab Vs Naib Din On 28 September, 2001pankajpandeylkoОценок пока нет

- D6.1 Computational Behaviour of RadicalisationДокумент29 страницD6.1 Computational Behaviour of RadicalisationpankajpandeylkoОценок пока нет

- Gigital Rights Proposal - PeterДокумент2 страницыGigital Rights Proposal - PeterpankajpandeylkoОценок пока нет

- PDF Upload 355882Документ7 страницPDF Upload 355882pankajpandeylkoОценок пока нет

- Socio-Technical Grounded Theory For Software Engineering: March 2021Документ27 страницSocio-Technical Grounded Theory For Software Engineering: March 2021pankajpandeylkoОценок пока нет

- International Journal of Information Management: Opinion PaperДокумент55 страницInternational Journal of Information Management: Opinion PaperpankajpandeylkoОценок пока нет

- 02 Budget and Financial Report v.1.0Документ29 страниц02 Budget and Financial Report v.1.0pankajpandeylkoОценок пока нет

- SSRN Idfbzd2732350Документ32 страницыSSRN Idfbzd2732350pankajpandeylkoОценок пока нет

- 07467408blockchains and Smart Contracts ForДокумент12 страниц07467408blockchains and Smart Contracts ForricardoОценок пока нет

- The Government Grant Act 1895Документ3 страницыThe Government Grant Act 1895Haseeb HassanОценок пока нет

- Crla (L) 1031 2000Документ12 страницCrla (L) 1031 2000pankajpandeylkoОценок пока нет

- Digital Economy Outlook Oct15 Cap1 PDFДокумент5 страницDigital Economy Outlook Oct15 Cap1 PDFpankajpandeylkoОценок пока нет

- 1047Документ17 страниц1047pankajpandeylkoОценок пока нет

- CII Rinaldi PDFДокумент15 страницCII Rinaldi PDFpankajpandeylkoОценок пока нет

- Jainetal ChildFingerprintRecognition TechRep MSU CSE 16 5Документ13 страницJainetal ChildFingerprintRecognition TechRep MSU CSE 16 5pankajpandeylkoОценок пока нет

- Smart Contracts PDFДокумент28 страницSmart Contracts PDFpankajpandeylkoОценок пока нет

- Ruleml 16Документ17 страницRuleml 16pankajpandeylkoОценок пока нет

- 168Документ20 страниц168pankajpandeylkoОценок пока нет

- INCP Supported ProjectsДокумент2 страницыINCP Supported ProjectspankajpandeylkoОценок пока нет

- Predicting Terrorism From Big Data Challenges U.S. Intelligence - BloombergДокумент9 страницPredicting Terrorism From Big Data Challenges U.S. Intelligence - BloombergpankajpandeylkoОценок пока нет

- INTPART Programme Description 2016Документ6 страницINTPART Programme Description 2016pankajpandeylkoОценок пока нет

- F 4418 e PanoramaДокумент39 страницF 4418 e PanoramapankajpandeylkoОценок пока нет

- Macro-Economic Cyber Security ModelsДокумент8 страницMacro-Economic Cyber Security ModelsWisnu AjiОценок пока нет

- Grant of Arms Licences For Acquisition/ Possession of Arms MHA Advisory Dated 6.4.2010 and Amendments Dated 7/10.1.2011.Документ8 страницGrant of Arms Licences For Acquisition/ Possession of Arms MHA Advisory Dated 6.4.2010 and Amendments Dated 7/10.1.2011.Abhishek KadyanОценок пока нет

- Little Book of LegacyДокумент20 страницLittle Book of Legacyrhythems84Оценок пока нет

- MFin 2015 Employment ReportДокумент4 страницыMFin 2015 Employment ReportpankajpandeylkoОценок пока нет

- Marksans Pharma - DynamicДокумент19 страницMarksans Pharma - DynamicanjugaduОценок пока нет

- Resolution On Pensionary Matter On Recommendation of 7th CPCДокумент4 страницыResolution On Pensionary Matter On Recommendation of 7th CPCVigneshwar Raju PrathikantamОценок пока нет

- Unit 1 Vouching - 1 - FinalДокумент12 страницUnit 1 Vouching - 1 - Finalshoaib shaikhОценок пока нет

- Climate Tech TakeawaysДокумент14 страницClimate Tech TakeawaysShipra RajputОценок пока нет

- Sologenic OnepagerДокумент1 страницаSologenic OnepagerzhullkhadriansyaОценок пока нет

- Investors Server: Eagle GuideДокумент7 страницInvestors Server: Eagle GuideshahakadirОценок пока нет

- BA 385T - Financial Management MEX - R. Rao and J. NolenДокумент5 страницBA 385T - Financial Management MEX - R. Rao and J. Nolenaugustin217Оценок пока нет

- IFT Assignment 1 (Akhilesh Jajee)Документ3 страницыIFT Assignment 1 (Akhilesh Jajee)anushaОценок пока нет

- Nordic EquitiesДокумент2 страницыNordic EquitiesBeing VikramОценок пока нет

- Chapter 4 Solution Problem 4 5 Page 1Документ3 страницыChapter 4 Solution Problem 4 5 Page 1saphirejunelОценок пока нет

- Holding Co. QuestionsДокумент77 страницHolding Co. Questionsअक्षय गोयलОценок пока нет

- OPMT New QuizДокумент3 страницыOPMT New QuizBhogendra RimalОценок пока нет

- Kasiva - The Impact of Risk Based Audit On Financial Performance in Commercial Banks in KenyaДокумент88 страницKasiva - The Impact of Risk Based Audit On Financial Performance in Commercial Banks in KenyaFraol BalayОценок пока нет

- Getting Financing or Funding Ch10-BB 080422Документ38 страницGetting Financing or Funding Ch10-BB 080422SAQIB SALEEMОценок пока нет

- Time Is MoneyДокумент22 страницыTime Is MoneyRachit TiwariОценок пока нет

- "Systematic Investment Plan: Sbi Mutual FundДокумент60 страниц"Systematic Investment Plan: Sbi Mutual FundStudent ProjectsОценок пока нет

- Icicidirect Centre For Financial Learning Equity: Chapter 1 Module 4 Basics On The Stock MarketДокумент5 страницIcicidirect Centre For Financial Learning Equity: Chapter 1 Module 4 Basics On The Stock MarketKSОценок пока нет

- Advacc2 Guerrero Chapter 14Документ14 страницAdvacc2 Guerrero Chapter 14jediiik50% (2)

- Cost of Capital ReviewerДокумент3 страницыCost of Capital ReviewerIamnti domnateОценок пока нет

- Company LawДокумент390 страницCompany Lawchotu shahОценок пока нет

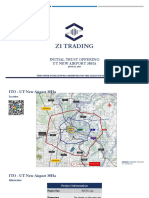

- UT New Airport 38ha - Project InformationДокумент10 страницUT New Airport 38ha - Project InformationPaul KitОценок пока нет

- Fundamentals of Accounting ReviewerДокумент3 страницыFundamentals of Accounting ReviewerRandy ParasОценок пока нет

- Stock ReturnДокумент7 страницStock ReturnHans Surya Candra DiwiryaОценок пока нет

- Market Maker TrapsДокумент109 страницMarket Maker TrapsFarid Taufiq93% (14)