Вам также может понравиться

- As Boomers Slow DownДокумент5 страницAs Boomers Slow DownsonheungminmaxОценок пока нет

- El2016 32Документ5 страницEl2016 32TBP_Think_TankОценок пока нет

- Appraising Longer-Run Demand Prospects For Farm ProductsДокумент18 страницAppraising Longer-Run Demand Prospects For Farm ProductsChristos VoulgarisОценок пока нет

- 2014 Economy Vs PresentДокумент7 страниц2014 Economy Vs PresentIan Daniel RosarioОценок пока нет

- James H StockДокумент39 страницJames H StockTBP_Think_TankОценок пока нет

- Perspective: Economic and MarketДокумент4 страницыPerspective: Economic and MarketdpbasicОценок пока нет

- Long - Run Economic Growth: Intermediate MacroeconomicsДокумент6 страницLong - Run Economic Growth: Intermediate MacroeconomicsAerl XuanОценок пока нет

- Economic Growth of Non-Placed StudentsДокумент10 страницEconomic Growth of Non-Placed StudentsAnkurBanerjee202Оценок пока нет

- EPI - Trend and Structure of National Income - U1 - P2Документ12 страницEPI - Trend and Structure of National Income - U1 - P2SrikantОценок пока нет

- Bank of EnglandДокумент18 страницBank of EnglandWishfulDownloadingОценок пока нет

- Lam Leibbrandt Global Demographic Trends and Their Implications For EmploymentДокумент33 страницыLam Leibbrandt Global Demographic Trends and Their Implications For EmploymentprawadhanОценок пока нет

- Robert E HallДокумент32 страницыRobert E HallTBP_Think_TankОценок пока нет

- GDPДокумент5 страницGDPANNEОценок пока нет

- Some Effects of Demographic Change On The UK EconomyДокумент22 страницыSome Effects of Demographic Change On The UK EconomyHao WangОценок пока нет

- Productivity, Prices, and MeasurementДокумент24 страницыProductivity, Prices, and MeasurementAustin DrukkerОценок пока нет

- Growth Scenario: Is The Common Man in The Picture?: Arun KumarДокумент10 страницGrowth Scenario: Is The Common Man in The Picture?: Arun KumarDeepak VermaОценок пока нет

- Demographic Effects On Labor Force Participation RateДокумент7 страницDemographic Effects On Labor Force Participation RatemichaelОценок пока нет

- Bloom Et Al (2011) - Population Aging - Facts Challenges and Responses PDFДокумент11 страницBloom Et Al (2011) - Population Aging - Facts Challenges and Responses PDFFernando BarretoОценок пока нет

- GDP Growth, The Unemployment Rate, and Okun's Law: Patrick HigginsДокумент2 страницыGDP Growth, The Unemployment Rate, and Okun's Law: Patrick HigginsCansu TurgutОценок пока нет

- Inflation DynamicsДокумент85 страницInflation Dynamicsabdulwahab0015Оценок пока нет

- Dez Industria Liz AreДокумент18 страницDez Industria Liz AreMihaelaMarcuОценок пока нет

- Economics Structural Changes Indian EconomyДокумент2 страницыEconomics Structural Changes Indian Economysuprith suppyОценок пока нет

- BlanchflowerДокумент25 страницBlanchflowerAdminAliОценок пока нет

- Chapter 18 Economic GrowthДокумент50 страницChapter 18 Economic GrowthJemimah Rejoice LuangoОценок пока нет

- GY300 Reading Week 2Документ6 страницGY300 Reading Week 2Shaista FarooqОценок пока нет

- Secular Stagnation: A Supply-Side ViewДокумент6 страницSecular Stagnation: A Supply-Side ViewRodrigo GaОценок пока нет

- Weekly Economic Commentary 3/18/2013Документ7 страницWeekly Economic Commentary 3/18/2013monarchadvisorygroupОценок пока нет

- Advanced Economics QuestionsДокумент5 страницAdvanced Economics QuestionsIainОценок пока нет

- Levine - 2011 - Economic Growth and The Unemployment RateДокумент11 страницLevine - 2011 - Economic Growth and The Unemployment RateHaifeng WuОценок пока нет

- El2017 23Документ5 страницEl2017 23TBP_Think_TankОценок пока нет

- Inflation and Economic Growth in MalaysiaДокумент20 страницInflation and Economic Growth in MalaysiaNurulSyahidaHassanОценок пока нет

- Economy DA - DDI 2018Документ282 страницыEconomy DA - DDI 2018Curtis LiuОценок пока нет

- Employment (Vision 2020) : Current Employment and Unemployment SituationДокумент21 страницаEmployment (Vision 2020) : Current Employment and Unemployment Situationaman kumarОценок пока нет

- Intermediate Macro AssignmentДокумент13 страницIntermediate Macro AssignmentJuneid ImritОценок пока нет

- Has Austerity Worked in Spain?Документ14 страницHas Austerity Worked in Spain?Center for Economic and Policy ResearchОценок пока нет

- Chalie Endalew Advisor Bawoke AtnafuДокумент35 страницChalie Endalew Advisor Bawoke AtnafuENIYEW EYASUОценок пока нет

- Thinking About MacroeconomicsДокумент30 страницThinking About MacroeconomicsChi-Wa CWОценок пока нет

- Active Aging in Economy and Society: Carl Bertelsmann Prize 2006От EverandActive Aging in Economy and Society: Carl Bertelsmann Prize 2006Оценок пока нет

- R Islam 2010 Jobless Growth Occasional - PaperДокумент47 страницR Islam 2010 Jobless Growth Occasional - PaperFalguni PattanaikОценок пока нет

- Growth Report - SummaryДокумент3 страницыGrowth Report - Summarybullz eyeОценок пока нет

- Report EconomyДокумент11 страницReport EconomydanОценок пока нет

- Doon Business School Dehradun: Philippines Country AnalysisДокумент20 страницDoon Business School Dehradun: Philippines Country Analysisvaibhav bhardwajОценок пока нет

- Cutting To The CoreДокумент2 страницыCutting To The CoreSamuel RinesОценок пока нет

- Other Aging America Dominance Older Firms Hathaway LitanДокумент18 страницOther Aging America Dominance Older Firms Hathaway Litanrichardck61Оценок пока нет

- Van Hoisington Q3Документ6 страницVan Hoisington Q3ZerohedgeОценок пока нет

- Failure by Design: The Story behind America's Broken EconomyОт EverandFailure by Design: The Story behind America's Broken EconomyРейтинг: 4 из 5 звезд4/5 (2)

- De VERA Primer 20120908 Version01Документ21 страницаDe VERA Primer 20120908 Version01pmellaОценок пока нет

- El2010 26Документ5 страницEl2010 26Vlad PredaОценок пока нет

- The Demise of U. S. Economic Growth: Restatement, Rebuttal, and ReflectionsДокумент43 страницыThe Demise of U. S. Economic Growth: Restatement, Rebuttal, and ReflectionsThe Washington PostОценок пока нет

- Destablizing An Unstable EconomyДокумент20 страницDestablizing An Unstable EconomyfahdaliОценок пока нет

- Economic Assignment MaterialДокумент5 страницEconomic Assignment MaterialAnmol killerОценок пока нет

- Growth and Structural Change in The Indian EconomyДокумент12 страницGrowth and Structural Change in The Indian EconomyYashpal SinghviОценок пока нет

- Economic Growth Analysis of ChinaДокумент5 страницEconomic Growth Analysis of ChinaPravesh KumarОценок пока нет

- Chapter 1 - Monitoring Macroeconomic Performance PDFДокумент29 страницChapter 1 - Monitoring Macroeconomic Performance PDFshivam jangidОценок пока нет

- 6 2007 enДокумент5 страниц6 2007 ensolankivikramОценок пока нет

- Socio-Economic Update: 11.1 PovertyДокумент11 страницSocio-Economic Update: 11.1 PovertyMuhammad FaiqueОценок пока нет

- 1 - 5 Haziran 2020 PolonyaДокумент11 страниц1 - 5 Haziran 2020 PolonyaxoОценок пока нет

- 2020 SFWSC Tasting Packaging Entry Form Booklet 1 PDFДокумент9 страниц2020 SFWSC Tasting Packaging Entry Form Booklet 1 PDFxoОценок пока нет

- Tub II-44 - 20Документ1 страницаTub II-44 - 20xoОценок пока нет

- Bright Futures InformationДокумент2 страницыBright Futures InformationxoОценок пока нет

- 2020 SFWSC Tasting Packaging Entry Form Booklet 1 PDFДокумент9 страниц2020 SFWSC Tasting Packaging Entry Form Booklet 1 PDFxoОценок пока нет

- For GogsДокумент5 страницFor GogsxoОценок пока нет

- Terms Conditions Eng 20 20Документ1 страницаTerms Conditions Eng 20 20xoОценок пока нет

- Irgpdf For Dogs in HouseДокумент87 страницIrgpdf For Dogs in HousexoОценок пока нет

- Guided Tour of The Groups Benefits Site - AODAДокумент4 страницыGuided Tour of The Groups Benefits Site - AODAxoОценок пока нет

- Schools Adventure Competition 2020Документ10 страницSchools Adventure Competition 2020xoОценок пока нет

- Visual Organiser For SEND Survey One Year On RДокумент1 страницаVisual Organiser For SEND Survey One Year On RxoОценок пока нет

- ROGERS PDF Jake Thompson's Daily Scorecard 2020Документ1 страницаROGERS PDF Jake Thompson's Daily Scorecard 2020xoОценок пока нет

- Sensors For MotorsДокумент16 страницSensors For MotorsxoОценок пока нет

- Edna Cleaton Tu Rbo PressДокумент2 страницыEdna Cleaton Tu Rbo PressxoОценок пока нет

- Aqa As RL Gde Bdy Jun 2019Документ18 страницAqa As RL Gde Bdy Jun 2019xoОценок пока нет

- Integrated Final Report SA Black System 28 September 2016Документ273 страницыIntegrated Final Report SA Black System 28 September 2016xoОценок пока нет

- AL2019 Companiesattending 1208Документ7 страницAL2019 Companiesattending 1208xoОценок пока нет

- LSMS Volleyball 2019 Eliminations As of 2019.10.05Документ16 страницLSMS Volleyball 2019 Eliminations As of 2019.10.05xoОценок пока нет

- Media Release - SS 644Документ9 страницMedia Release - SS 644xoОценок пока нет

- TT Gce Summer19 Final v3Документ10 страницTT Gce Summer19 Final v3xoОценок пока нет

- Proposed Encroachment Over SA Water EasementsДокумент9 страницProposed Encroachment Over SA Water EasementsxoОценок пока нет

- Our CommitmentДокумент2 страницыOur CommitmentxoОценок пока нет

- Algebra IX 1996Документ17 страницAlgebra IX 1996stef11_127571Оценок пока нет

- Clinical Placement Deed PollДокумент4 страницыClinical Placement Deed PollxoОценок пока нет

- FlyerДокумент8 страницFlyerxoОценок пока нет

- Form1 SaДокумент4 страницыForm1 SaxoОценок пока нет

- Flyer Email Version 2018 WhiteДокумент1 страницаFlyer Email Version 2018 WhitexoОценок пока нет

- Clinical Placement Deed PollДокумент4 страницыClinical Placement Deed PollxoОценок пока нет

- FlyerДокумент8 страницFlyerxoОценок пока нет

- Intelligent Interactive Synthesizer Surface Mount Model:: LFSFN100200-100Документ7 страницIntelligent Interactive Synthesizer Surface Mount Model:: LFSFN100200-100xoОценок пока нет

- Area Handbook - IraqДокумент323 страницыArea Handbook - IraqRobert Vale100% (1)

- Malaysia'S Outward Foreign Affiliates Statistics: Norul Anisa Abu Safran and Hasnul Hadi JamaliДокумент14 страницMalaysia'S Outward Foreign Affiliates Statistics: Norul Anisa Abu Safran and Hasnul Hadi JamaliHusnaanaОценок пока нет

- Applied Economics Week 2Документ9 страницApplied Economics Week 2Frank Russel VillaniaОценок пока нет

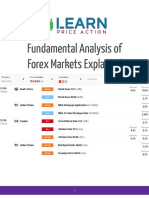

- Fundamental Analysis of Forex Markets ExplainedДокумент13 страницFundamental Analysis of Forex Markets ExplainedAar Rageedi0% (1)

- Macroeconomics 21st Edition Mcconnell Test BankДокумент38 страницMacroeconomics 21st Edition Mcconnell Test Bankiradelahay921100% (13)

- Bachelor Thesis Dipo DaramolaДокумент101 страницаBachelor Thesis Dipo DaramolaAjibolaОценок пока нет

- Macro Eco Complete Ques+NotesДокумент117 страницMacro Eco Complete Ques+NotesPiyush ChhajerОценок пока нет

- Economic DevelopmentДокумент20 страницEconomic DevelopmentDeepjyoti RoyОценок пока нет

- Calificación de Riesgo GuatemalaДокумент20 страницCalificación de Riesgo GuatemalaErickaОценок пока нет

- The Economic Impacts of Coronavirus Covid 19 Learning LossesДокумент24 страницыThe Economic Impacts of Coronavirus Covid 19 Learning LossesmanishaОценок пока нет

- UN - ESCAP (2011) Statistical-Yearbook-Asia-Pacific-Education-2011-En PDFДокумент312 страницUN - ESCAP (2011) Statistical-Yearbook-Asia-Pacific-Education-2011-En PDFlittleconspiratorОценок пока нет

- Measuring National Output and National Income: Chapter OutlineДокумент33 страницыMeasuring National Output and National Income: Chapter OutlinecharlotteОценок пока нет

- Ermias TamiruДокумент119 страницErmias TamiruAli HassenОценок пока нет

- Macro Economics 1Документ9 страницMacro Economics 1Deepak SinghОценок пока нет

- QTMДокумент8 страницQTMKhalid AzizОценок пока нет

- GLEC Gyan Kosh PDFДокумент39 страницGLEC Gyan Kosh PDFMihir VoraОценок пока нет

- The Circular Flow of Income Five-Sector ModelДокумент9 страницThe Circular Flow of Income Five-Sector ModelSamPetherbridge86% (7)

- ChikkamagaluruДокумент35 страницChikkamagalururanjith ananthОценок пока нет

- ECommerce Philippines Roadmap 2022Документ92 страницыECommerce Philippines Roadmap 2022Kay ZeeОценок пока нет

- Tourism Contribution To Economic Growth of Gondar CityДокумент26 страницTourism Contribution To Economic Growth of Gondar Cityselome NegatuОценок пока нет

- The Brazilian EconomyДокумент37 страницThe Brazilian Economyرامي أبو الفتوحОценок пока нет

- NCS E-Newsletter - June, 2019Документ14 страницNCS E-Newsletter - June, 2019Dheerendra YadavОценок пока нет

- Indian Logistics Industry: The Next Big Growth DriverДокумент13 страницIndian Logistics Industry: The Next Big Growth Driverpankajku2020100% (7)

- 801 Balancing BudgetsДокумент99 страниц801 Balancing BudgetsPiОценок пока нет

- Fiscal Policy Strategy 2020 21Документ24 страницыFiscal Policy Strategy 2020 21Lalmuanawma MualchinОценок пока нет

- Global and Caribbean Tourism and Its Contribution To The Global EconomyДокумент25 страницGlobal and Caribbean Tourism and Its Contribution To The Global EconomyDre's Graphic DesignsОценок пока нет

- Final Project Report - Blue Bird - 2201Документ58 страницFinal Project Report - Blue Bird - 2201Miftanur HusnaОценок пока нет

- Stakeholders of UnileverДокумент18 страницStakeholders of Unileverwonderboy_1791100% (1)

- DHL Global Connectedness Index 2011Документ242 страницыDHL Global Connectedness Index 2011bcrucqОценок пока нет

- MCB Focus: Mauritius Inc.: Engaging and Partnering With Africa On Its Transformative JourneyДокумент120 страницMCB Focus: Mauritius Inc.: Engaging and Partnering With Africa On Its Transformative JourneyL'express MauriceОценок пока нет