Вам также может понравиться

- Non Destructive Evaluation MethodsДокумент1 страницаNon Destructive Evaluation MethodsPrateek VyasОценок пока нет

- Non Destructive EvaluationДокумент1 страницаNon Destructive EvaluationPrateek VyasОценок пока нет

- NDT TestingДокумент1 страницаNDT TestingPrateek VyasОценок пока нет

- Testing of Concrete HandbookДокумент1 страницаTesting of Concrete HandbookPrateek VyasОценок пока нет

- NDT Testing Standard For Steel TanksДокумент1 страницаNDT Testing Standard For Steel TanksPrateek VyasОценок пока нет

- Testing of Concrete Tank InspectionДокумент1 страницаTesting of Concrete Tank InspectionPrateek VyasОценок пока нет

- NDT Testing Standard For TanksДокумент1 страницаNDT Testing Standard For TanksPrateek VyasОценок пока нет

- Steel Tanks QualityДокумент1 страницаSteel Tanks QualityPrateek VyasОценок пока нет

- NDT Testing Standard For Steel Tanks QualityДокумент1 страницаNDT Testing Standard For Steel Tanks QualityPrateek VyasОценок пока нет

- NDT Testing StandardДокумент1 страницаNDT Testing StandardPrateek VyasОценок пока нет

- Testing of Concrete Handbook For ProceduresДокумент1 страницаTesting of Concrete Handbook For ProceduresPrateek VyasОценок пока нет

- NDT Testing of Concrete Handbook For ProceduresДокумент1 страницаNDT Testing of Concrete Handbook For ProceduresPrateek VyasОценок пока нет

- Testing of Concrete DIN Guide InspectionДокумент1 страницаTesting of Concrete DIN Guide InspectionPrateek VyasОценок пока нет

- Testing of Concrete Tank Inspection and ProceduresДокумент1 страницаTesting of Concrete Tank Inspection and ProceduresPrateek VyasОценок пока нет

- Testing of Concrete GuidebookДокумент1 страницаTesting of Concrete GuidebookPrateek VyasОценок пока нет

- NDT Testing of Concrete Structures GuideДокумент1 страницаNDT Testing of Concrete Structures GuidePrateek VyasОценок пока нет

- Testing of ConcreteДокумент1 страницаTesting of ConcretePrateek VyasОценок пока нет

- Testing of Concrete DIN GuideДокумент1 страницаTesting of Concrete DIN GuidePrateek VyasОценок пока нет

- NDT of ConcreteДокумент1 страницаNDT of ConcretePrateek VyasОценок пока нет

- NDT of Concrete MethodsДокумент1 страницаNDT of Concrete MethodsPrateek VyasОценок пока нет

- QMS ISO 9004 Code Implementation PaperДокумент1 страницаQMS ISO 9004 Code Implementation PaperPrateek VyasОценок пока нет

- Non Destructive Testing of Concrete MethodsДокумент1 страницаNon Destructive Testing of Concrete MethodsPrateek VyasОценок пока нет

- QMS Awareness ISO 9001 2015 CodeДокумент1 страницаQMS Awareness ISO 9001 2015 CodePrateek VyasОценок пока нет

- Non Destructive Testing MethodsДокумент1 страницаNon Destructive Testing MethodsPrateek VyasОценок пока нет

- QMS ISO 9004 2015 Implementation WorkshopДокумент1 страницаQMS ISO 9004 2015 Implementation WorkshopPrateek Vyas0% (1)

- Effect of QMSДокумент1 страницаEffect of QMSPrateek VyasОценок пока нет

- Non Destructive TestingДокумент1 страницаNon Destructive TestingPrateek VyasОценок пока нет

- QMS Awareness ISO 9001 2015 Implementation GuidanceДокумент1 страницаQMS Awareness ISO 9001 2015 Implementation GuidancePrateek VyasОценок пока нет

- Effect of QMS Awareness ISO 9001Документ1 страницаEffect of QMS Awareness ISO 9001Prateek VyasОценок пока нет

- Effect of QMS AwarenessДокумент1 страницаEffect of QMS AwarenessPrateek VyasОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Concentrated Photovoltaic: 02 March 2017Документ33 страницыConcentrated Photovoltaic: 02 March 2017sohaibОценок пока нет

- Argumentative Essay Outline and WCДокумент2 страницыArgumentative Essay Outline and WCOscar Cruz83% (6)

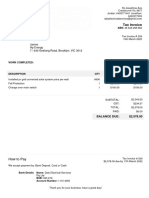

- Daly Electrical Services PTY LTD Invoice #329Документ1 страницаDaly Electrical Services PTY LTD Invoice #329artemopamintaОценок пока нет

- Solarkitchen 141024035618 Conversion Gate01Документ16 страницSolarkitchen 141024035618 Conversion Gate01bushra sayyadОценок пока нет

- ZnshinesolarДокумент4 страницыZnshinesolarVedant KОценок пока нет

- PVPS_Trends_Report_2023_WEBДокумент96 страницPVPS_Trends_Report_2023_WEBCristian BogoiОценок пока нет

- UntitledДокумент6 страницUntitledPrincess Arielle KintanarОценок пока нет

- Converteam Annual Report 2010Документ101 страницаConverteam Annual Report 2010tarangireОценок пока нет

- EB 2 Petition Letter 1Документ20 страницEB 2 Petition Letter 1oluwabusayoforsuccessОценок пока нет

- 21-Suzlon PresentationДокумент21 страница21-Suzlon PresentationMohit KansalОценок пока нет

- Top 10 Global Issues InsightsДокумент85 страницTop 10 Global Issues InsightsRACU 4A ACGОценок пока нет

- 2022 Torqeedo Catalog en InternationalДокумент56 страниц2022 Torqeedo Catalog en InternationalNegrea RobertОценок пока нет

- The U.S. Virgin Islands Renewable and Alternative Energy Act of 2009Документ28 страницThe U.S. Virgin Islands Renewable and Alternative Energy Act of 2009Detlef LoyОценок пока нет

- Lecture 1 New - Solar-Powered Pumping SystemДокумент181 страницаLecture 1 New - Solar-Powered Pumping Systemapi-620585842Оценок пока нет

- รวมดาวCДокумент22 страницыรวมดาวCD 9Оценок пока нет

- Geothermal Energy Poster 2Документ1 страницаGeothermal Energy Poster 2api-298575301100% (2)

- The Umrao (Solar Quote)Документ3 страницыThe Umrao (Solar Quote)Seema solar EnterprisesОценок пока нет

- Availability Factor - Wikipedia, The Free EncyclopediaДокумент2 страницыAvailability Factor - Wikipedia, The Free EncyclopediaSujeet KumarОценок пока нет

- LANDY Hydropower ScrewsДокумент12 страницLANDY Hydropower Screwslifemillion2847Оценок пока нет

- Financing Sources for Energy Projects in Developing CountriesДокумент57 страницFinancing Sources for Energy Projects in Developing Countrieshunter8213Оценок пока нет

- Thesis On Solar Power SystemДокумент8 страницThesis On Solar Power Systemfjjf1zqp100% (2)

- Fossil Fuels vs Renewable Energy: A ComparisonДокумент1 страницаFossil Fuels vs Renewable Energy: A ComparisonXin Zheng100% (3)

- Foysal 2018.10Документ4 страницыFoysal 2018.10All in AllОценок пока нет

- Biomass-Industry CARINOДокумент4 страницыBiomass-Industry CARINOCriselda CarinoОценок пока нет

- Desert Claim Farm Map - Original - Map 2006Документ1 страницаDesert Claim Farm Map - Original - Map 2006Ellensburg Daily RecordОценок пока нет

- EV ReportДокумент3 страницыEV ReportBavithra KОценок пока нет

- Generation Plan - Sri LankaДокумент7 страницGeneration Plan - Sri LankaKawshyОценок пока нет

- Techlife News July 01 2023Документ206 страницTechlife News July 01 2023JulianSantosMoralesОценок пока нет

- Reading Passage 1: IELTS Mock Test 2020 OctoberДокумент19 страницReading Passage 1: IELTS Mock Test 2020 OctoberEDWIN M.PОценок пока нет

- H14.72.HR.090702.PE Data SheetДокумент5 страницH14.72.HR.090702.PE Data SheeteekamaleshОценок пока нет