Вам также может понравиться

- Ma Simonova I 2015Документ84 страницыMa Simonova I 2015rajaniОценок пока нет

- An Empirical Research On Investor Biases in Financial Decision-Making, Financial Risk Tolerance and Financial PersonalityДокумент12 страницAn Empirical Research On Investor Biases in Financial Decision-Making, Financial Risk Tolerance and Financial PersonalityrajaniОценок пока нет

- Behavioral Biases in Investment Decision Making: A Literature ReviewДокумент7 страницBehavioral Biases in Investment Decision Making: A Literature ReviewrajaniОценок пока нет

- 18 SynopsisДокумент34 страницы18 SynopsisrajaniОценок пока нет

- 51 1 142 1 10 20180830 PDFДокумент27 страниц51 1 142 1 10 20180830 PDFrajaniОценок пока нет

- The International Journal of Human Resource Management: Click For UpdatesДокумент22 страницыThe International Journal of Human Resource Management: Click For UpdatesrajaniОценок пока нет

- Investment Avenues:: Chapter No.2Документ12 страницInvestment Avenues:: Chapter No.2rajaniОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- CRM Proof PDFДокумент404 страницыCRM Proof PDFtonicors_806375834Оценок пока нет

- Impact of Basel III On Financial MarketsДокумент4 страницыImpact of Basel III On Financial MarketsAnish JoshiОценок пока нет

- Literature Review Economic DevelopmentДокумент8 страницLiterature Review Economic Developmentc5pnw26s100% (1)

- JPM Accum TermsheetДокумент16 страницJPM Accum TermsheetPei Jing0% (1)

- A Study On Investors Perception Towards Mutual Funds in HyderabadДокумент61 страницаA Study On Investors Perception Towards Mutual Funds in HyderabadPreethu GowdaОценок пока нет

- Serious Ideas For Serious Investors: Index Nov-Dec Index - A PDFДокумент72 страницыSerious Ideas For Serious Investors: Index Nov-Dec Index - A PDFRyan ReitzОценок пока нет

- Trading Stock ETF DocumentДокумент38 страницTrading Stock ETF Documentraf keОценок пока нет

- Reading 35 Exchange-Traded Funds - Mechanics and Applications - AnswersДокумент10 страницReading 35 Exchange-Traded Funds - Mechanics and Applications - Answerstristan.riolsОценок пока нет

- 投資學期末報告Документ11 страниц投資學期末報告曾于芮Оценок пока нет

- A Study On Budgetary Control at HDFC1567681191 PDFДокумент28 страницA Study On Budgetary Control at HDFC1567681191 PDFNationalinstituteDsnrОценок пока нет

- Bogle InterviewДокумент8 страницBogle InterviewMatt EbrahimiОценок пока нет

- MSCI All Country World Index: Why Investors Use The ACWIДокумент4 страницыMSCI All Country World Index: Why Investors Use The ACWIRphddОценок пока нет

- SPDR S&P 500 ETF Trust SPY: Key FeaturesДокумент2 страницыSPDR S&P 500 ETF Trust SPY: Key FeaturesIsai Jesús Gomez MéndezОценок пока нет

- Nism NotesДокумент456 страницNism NotesVetri M Konar100% (4)

- Kim - Sbi Etf Sensex PDFДокумент45 страницKim - Sbi Etf Sensex PDFRmc RmcОценок пока нет

- Gold Survey 2009 Launch PresentationДокумент35 страницGold Survey 2009 Launch Presentationkunal_desai7447Оценок пока нет

- Idx Annually 2022Документ231 страницаIdx Annually 2022Ridla Data nomor satu100% (1)

- Quantech Investments Smart BetaДокумент16 страницQuantech Investments Smart BetaAnthony Fj Garner100% (1)

- Q&A With Li Lu (Himalaya Capital)Документ17 страницQ&A With Li Lu (Himalaya Capital)DiegoDiazPiñeiroОценок пока нет

- 5 Best Stock Trading Apps You Should Get in 2022Документ5 страниц5 Best Stock Trading Apps You Should Get in 2022Wahyu HidayatullahОценок пока нет

- Brand RelevanceДокумент16 страницBrand RelevancefmartinОценок пока нет

- HL Guide Retirement For Under 40s 1018Документ18 страницHL Guide Retirement For Under 40s 1018BenОценок пока нет

- Stock Market Terms and DefinitionsДокумент43 страницыStock Market Terms and DefinitionsK-Cube Morong0% (1)

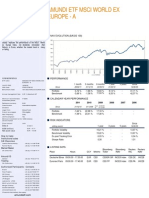

- Amundi Etf Msci World Ex Europe - A - Anglais - Eur - 3163!47!2!3!207 - MДокумент2 страницыAmundi Etf Msci World Ex Europe - A - Anglais - Eur - 3163!47!2!3!207 - Mhp24714303Оценок пока нет

- Exchange Traded FundДокумент17 страницExchange Traded FundChitwan AchantaniОценок пока нет

- Research SampleДокумент8 страницResearch SampleAngela Jesca Medina JabidoОценок пока нет

- 2023DEC Stocks&Commodities MagazineДокумент64 страницы2023DEC Stocks&Commodities MagazineNuria PuenteОценок пока нет

- CB Insights Disruption Investment BankingДокумент45 страницCB Insights Disruption Investment BankingbandarumanasaОценок пока нет

- Tutorials in Applied Technical Analysis: The Australian Internet Trading Weekly With Independent AnalysisДокумент25 страницTutorials in Applied Technical Analysis: The Australian Internet Trading Weekly With Independent AnalysismaddyraskalОценок пока нет

- Parkit Asset Management - Q4 - 13Документ12 страницParkit Asset Management - Q4 - 13st96dgx8Оценок пока нет