Вам также может понравиться

- Suggested Answers To 2014 Remedial Law Bar ExamДокумент1 страницаSuggested Answers To 2014 Remedial Law Bar ExamDennise TalanОценок пока нет

- Before The Court Is The Petition For Review OnДокумент1 страницаBefore The Court Is The Petition For Review OnDennise TalanОценок пока нет

- Suggested Answers To 2014 Remedial Law Bar ExamДокумент1 страницаSuggested Answers To 2014 Remedial Law Bar ExamDennise TalanОценок пока нет

- SfewfrwrsfasdaДокумент1 страницаSfewfrwrsfasdaDennise TalanОценок пока нет

- Suggested Answers To 2014 Remedial Law Bar ExamДокумент1 страницаSuggested Answers To 2014 Remedial Law Bar ExamDennise TalanОценок пока нет

- Ujbefoiwekdsgueild, Mnnhyueio 123456789 SDFGHCVBNMДокумент1 страницаUjbefoiwekdsgueild, Mnnhyueio 123456789 SDFGHCVBNMDennise TalanОценок пока нет

- Burdens of EvidenceДокумент1 страницаBurdens of EvidenceDennise TalanОценок пока нет

- Suggested Answers To 2014 Remedial Law Bar ExamДокумент1 страницаSuggested Answers To 2014 Remedial Law Bar ExamDennise TalanОценок пока нет

- Suggested Answers To 2014 Remedial Law Bar ExamДокумент1 страницаSuggested Answers To 2014 Remedial Law Bar ExamDennise TalanОценок пока нет

- Termination of EmploymentДокумент1 страницаTermination of EmploymentDennise TalanОценок пока нет

- Suggested Answers To 2014 Remedial Law Bar ExamДокумент1 страницаSuggested Answers To 2014 Remedial Law Bar ExamDennise TalanОценок пока нет

- Not Be Financially Interested, Directly or Indirectly, in Any Contract With, or in Any Franchise or Special Privilege GrantedДокумент1 страницаNot Be Financially Interested, Directly or Indirectly, in Any Contract With, or in Any Franchise or Special Privilege GrantedDennise TalanОценок пока нет

- Suggested Answers To 2014 Remedial Law Bar ExamДокумент1 страницаSuggested Answers To 2014 Remedial Law Bar ExamDennise TalanОценок пока нет

- 4 Rfbni 765 Edvbnlpr OiuytДокумент1 страница4 Rfbni 765 Edvbnlpr OiuytDennise TalanОценок пока нет

- Burdens of EvidenceДокумент1 страницаBurdens of EvidenceDennise TalanОценок пока нет

- Angeles v. Secretary of Justice G. R. No. 142549. March 9, 2010Документ1 страницаAngeles v. Secretary of Justice G. R. No. 142549. March 9, 2010Dennise TalanОценок пока нет

- Burdens of EvidenceДокумент1 страницаBurdens of EvidenceDennise TalanОценок пока нет

- Burdens of EvidenceДокумент1 страницаBurdens of EvidenceDennise TalanОценок пока нет

- Burdens of EvidenceДокумент1 страницаBurdens of EvidenceDennise TalanОценок пока нет

- Burdens of EvidenceДокумент1 страницаBurdens of EvidenceDennise TalanОценок пока нет

- When Right To Speedy Disposition of Cases Is ViolatedДокумент1 страницаWhen Right To Speedy Disposition of Cases Is ViolatedDennise TalanОценок пока нет

- Decisive Legal Assistance and NotДокумент1 страницаDecisive Legal Assistance and NotDennise TalanОценок пока нет

- Right To Be Informed of The Nature and Cause of ActionДокумент1 страницаRight To Be Informed of The Nature and Cause of ActionDennise TalanОценок пока нет

- Burdens of EvidenceДокумент1 страницаBurdens of EvidenceDennise TalanОценок пока нет

- Burdens of EvidenceДокумент1 страницаBurdens of EvidenceDennise TalanОценок пока нет

- IssueДокумент1 страницаIssueDennise TalanОценок пока нет

- They Shall Not, Directly or Indirectly, Have Any Financial Material Interest in Any Transaction Requiring The Approval of Their OfficeДокумент1 страницаThey Shall Not, Directly or Indirectly, Have Any Financial Material Interest in Any Transaction Requiring The Approval of Their OfficeDennise TalanОценок пока нет

- HeldДокумент1 страницаHeldDennise TalanОценок пока нет

- Issue: Is Ynchausti Liable For The Loss? YES. RatioДокумент1 страницаIssue: Is Ynchausti Liable For The Loss? YES. RatioDennise TalanОценок пока нет

- HeldДокумент1 страницаHeldDennise TalanОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (120)

- Petitioners vs. vs. Respondents Estratonico Añano Gaudencio P. LaguaДокумент7 страницPetitioners vs. vs. Respondents Estratonico Añano Gaudencio P. LaguaAriel Conrad MalimasОценок пока нет

- Taylor's Hostel Management ApplicationДокумент2 страницыTaylor's Hostel Management ApplicationFahad FarhanОценок пока нет

- Heirs of Reyes v. CAДокумент9 страницHeirs of Reyes v. CASJ Normando CatubayОценок пока нет

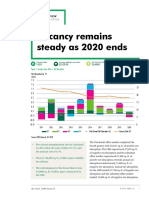

- Cincinnati Office MarketView Q4 2020Документ6 страницCincinnati Office MarketView Q4 2020WCPO 9 NewsОценок пока нет

- Chapter-5: Linear Functions Linear Cost Functions Linear Revenue Functions Linear Profit Functions Break Even 182Документ11 страницChapter-5: Linear Functions Linear Cost Functions Linear Revenue Functions Linear Profit Functions Break Even 182Najia SalmanОценок пока нет

- Letter To NICДокумент2 страницыLetter To NICJustin DukeОценок пока нет

- Lease AgreementДокумент5 страницLease AgreementSridhara babu. N - ಶ್ರೀಧರ ಬಾಬು. ಎನ್86% (7)

- Philippine Real Estate Market 3Q 2012Документ14 страницPhilippine Real Estate Market 3Q 2012joni_p9mОценок пока нет

- Property Yields As Tools For Valuation andДокумент64 страницыProperty Yields As Tools For Valuation andbiarhCОценок пока нет

- Chapter 5 - TBTДокумент8 страницChapter 5 - TBTKatKat Olarte100% (2)

- MHCFS Credit App SHORT FORMДокумент1 страницаMHCFS Credit App SHORT FORMnavu_uppalОценок пока нет

- Hired and Non-Owned Auto Liability Supplemental ApplicationДокумент3 страницыHired and Non-Owned Auto Liability Supplemental ApplicationSuReSh DodiyaОценок пока нет

- Advantages Disadvantages SmartДокумент6 страницAdvantages Disadvantages SmartrbhavishОценок пока нет

- FR Pipfa Paper CompleteДокумент20 страницFR Pipfa Paper CompleteGENIUS15070% (1)

- Commercial Property Management Director in Los Angeles CA Resume Michael KeurjianДокумент3 страницыCommercial Property Management Director in Los Angeles CA Resume Michael KeurjianMichaelKeurjian2Оценок пока нет

- MWC - CRA Economic Incentive Agreement Dated 2015-03-02Документ109 страницMWC - CRA Economic Incentive Agreement Dated 2015-03-02Ilde Brando Leoncito AdarloОценок пока нет

- Nicole Reese SBA2Документ1 страницаNicole Reese SBA2ColeReeseОценок пока нет

- SapphireReserveCard V0000039 BGC10582 Eng PDFДокумент56 страницSapphireReserveCard V0000039 BGC10582 Eng PDFamir.workОценок пока нет

- Problem 1: ComputationsДокумент6 страницProblem 1: ComputationsClarissa BorbonОценок пока нет

- Acct 3151 Notes 2Документ16 страницAcct 3151 Notes 2Donald YumОценок пока нет

- Pershing Square's Latest Presentation On General Growth PropertiesДокумент55 страницPershing Square's Latest Presentation On General Growth PropertiesDealBookОценок пока нет

- EOF Lecture Notes - Rent vs. Buy - Sep 8Документ28 страницEOF Lecture Notes - Rent vs. Buy - Sep 8碧莹成Оценок пока нет

- Cesar C. Peralejo For Plaintiffs-Appellees. Francisco Carreon & Renato E. Tañada For Defendant-AppellantДокумент11 страницCesar C. Peralejo For Plaintiffs-Appellees. Francisco Carreon & Renato E. Tañada For Defendant-AppellantMei-Ann Caña EscobedoОценок пока нет

- Felxible Realestate ManagementДокумент42 страницыFelxible Realestate ManagementrambabumekaОценок пока нет

- LEASE1Документ3 страницыLEASE1Ana Leah DelfinОценок пока нет

- Work Submission 2 - Puri and Rajput Law ConsultantsДокумент8 страницWork Submission 2 - Puri and Rajput Law ConsultantsManasa CheekatlaОценок пока нет

- NCM22385Документ6 страницNCM22385Martin SimpsonОценок пока нет

- Azcuna, Jr. v. CAДокумент2 страницыAzcuna, Jr. v. CAKrisha Marie CarlosОценок пока нет

- Sellers Property Information Form PDFДокумент16 страницSellers Property Information Form PDFPuiDeMatzaОценок пока нет

- Management Accounting For Financial ServicesДокумент4 страницыManagement Accounting For Financial ServicesMuhammad KashifОценок пока нет