Вам также может понравиться

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (120)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Algorithmic Trading Directory 2010Документ100 страницAlgorithmic Trading Directory 201017524100% (4)

- Navigator 2020 PDFДокумент24 страницыNavigator 2020 PDFSuryan KОценок пока нет

- 3464172Документ34 страницы3464172Aasri RОценок пока нет

- Help FileДокумент92 страницыHelp FileAnirudh NarlaОценок пока нет

- 2014 Giaa - Consol - 30062014Документ145 страниц2014 Giaa - Consol - 30062014yukeОценок пока нет

- 16 - Rahul Mundada - Mudita MathurДокумент8 страниц16 - Rahul Mundada - Mudita MathurRahul MundadaОценок пока нет

- Chapter 4 14Документ68 страницChapter 4 14Renz ManuelОценок пока нет

- Lean - Total Productive MaintenanceДокумент9 страницLean - Total Productive MaintenanceBalaji SОценок пока нет

- Insurance For Small BusinessesДокумент2 страницыInsurance For Small BusinessesTheodorah Gaelle MadzyОценок пока нет

- The Importance of Independence.: Q:-Who Is Subject To Independence Restrictions?Документ5 страницThe Importance of Independence.: Q:-Who Is Subject To Independence Restrictions?anon-583391Оценок пока нет

- IRAC Question Assessment Task 2 - Sem 1 2022Документ1 страницаIRAC Question Assessment Task 2 - Sem 1 2022Lương Nguyễn Khánh Bảo100% (1)

- NISHAT MILLS LTDTTДокумент29 страницNISHAT MILLS LTDTTramzanОценок пока нет

- Logical DWDesignДокумент5 страницLogical DWDesignbvishwanathrОценок пока нет

- Baf 222 Cost Accounting CatДокумент3 страницыBaf 222 Cost Accounting CatMartinez MachazОценок пока нет

- Balance of PaymentsДокумент4 страницыBalance of PaymentsOsman JallohОценок пока нет

- Pert and CPM: Projecct Management ToolsДокумент98 страницPert and CPM: Projecct Management Toolslakshmi dileepОценок пока нет

- Module 2a - AR RecapДокумент10 страницModule 2a - AR RecapChen HaoОценок пока нет

- 03 Bank ReconliationДокумент4 страницы03 Bank Reconliationsharielles /Оценок пока нет

- An Introduction To Integrated Marketing CommunicationsДокумент42 страницыAn Introduction To Integrated Marketing CommunicationsShuvroОценок пока нет

- Yvette Cyprian ElewaДокумент5 страницYvette Cyprian Elewaapi-535701983Оценок пока нет

- Integrated Marketing CommunicationДокумент22 страницыIntegrated Marketing CommunicationMallikarjun Reddy AvisalaОценок пока нет

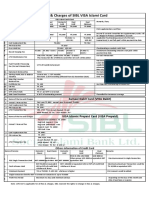

- Fees and Charges of SIBL Islami CardДокумент1 страницаFees and Charges of SIBL Islami CardMd YusufОценок пока нет

- Comm3201 Individual Case Study (June 2020)Документ3 страницыComm3201 Individual Case Study (June 2020)Scarlett WangОценок пока нет

- CDMДокумент2 страницыCDMi am tadaeiОценок пока нет

- Nptel: TopicДокумент104 страницыNptel: TopicRAJAT . 20GSOB1010459Оценок пока нет

- Five Steps To Effective Corporate GovernanceДокумент7 страницFive Steps To Effective Corporate Governanceneamma0% (1)

- Note Buad836 Mod1 Yj7myoyoou5ym38Документ150 страницNote Buad836 Mod1 Yj7myoyoou5ym38Adetunji TaiwoОценок пока нет

- Cost Management 2nd Edition Eldenburg Test BankДокумент40 страницCost Management 2nd Edition Eldenburg Test Bankaperez1105Оценок пока нет

- QUESTION BANK For Banking and Insurance MBA Sem IV-FinanceДокумент2 страницыQUESTION BANK For Banking and Insurance MBA Sem IV-FinanceAgnya PatelОценок пока нет

- How To Develop A CRM RoadmapДокумент3 страницыHow To Develop A CRM Roadmapfb3003Оценок пока нет