Вам также может понравиться

- Capital Budgeting TechniquesДокумент8 страницCapital Budgeting Techniqueswaqaar raoОценок пока нет

- Financial Evaluation (Autorecovered)Документ4 страницыFinancial Evaluation (Autorecovered)rohin gargОценок пока нет

- Capital BudgetingДокумент14 страницCapital BudgetingD Y Patil Institute of MCA and MBAОценок пока нет

- Capital BudgetingДокумент6 страницCapital BudgetingKhushbu PriyadarshniОценок пока нет

- Technic of Cap BudДокумент6 страницTechnic of Cap BudAmar NathОценок пока нет

- FM AssignmentДокумент5 страницFM AssignmentMuhammad Haris Muhammad AslamОценок пока нет

- Year, Financial Management: Capital BudgetingДокумент9 страницYear, Financial Management: Capital BudgetingPooja KansalОценок пока нет

- Capital Budgeting-Theory and NumericalsДокумент47 страницCapital Budgeting-Theory and Numericalssaadsaaid50% (2)

- Capital Budgeting TechniquesДокумент4 страницыCapital Budgeting TechniquesVamsi SakhamuriОценок пока нет

- CHAPTER 2 - Investment AppraisalДокумент19 страницCHAPTER 2 - Investment AppraisalMaleoaОценок пока нет

- Capitalbudgeting 1227282768304644 8Документ27 страницCapitalbudgeting 1227282768304644 8Sumi LatheefОценок пока нет

- Fin3 Midterm ExamДокумент8 страницFin3 Midterm ExamBryan Lluisma100% (1)

- Investment Appraisal TechniquesДокумент6 страницInvestment Appraisal TechniquesERICK MLINGWAОценок пока нет

- Final ProjectДокумент65 страницFinal ProjectD PriyankaОценок пока нет

- Assignment On FaseelДокумент6 страницAssignment On FaseelAbdul KhanОценок пока нет

- Capital BudgetingДокумент9 страницCapital BudgetingHarshitaОценок пока нет

- Lecture Capital BudgetingДокумент5 страницLecture Capital BudgetingJenelyn FloresОценок пока нет

- FM AssДокумент3 страницыFM AssBitta Saha HridoyОценок пока нет

- Techniques of Capital BudgetingДокумент20 страницTechniques of Capital Budgetinggoogle BabaОценок пока нет

- 22 Capital Rationing and Criteria For Investment AnalysisДокумент10 страниц22 Capital Rationing and Criteria For Investment AnalysisManishKumarRoasanОценок пока нет

- Dr. Sandeep Malu Associate Professor SVIM, IndoreДокумент14 страницDr. Sandeep Malu Associate Professor SVIM, Indorechaterji_aОценок пока нет

- Dr. Sandeep Malu Associate Professor SVIM, IndoreДокумент14 страницDr. Sandeep Malu Associate Professor SVIM, Indorechaterji_aОценок пока нет

- Module in Financial Management - 09Документ7 страницModule in Financial Management - 09Karla Mae GammadОценок пока нет

- Capital Budgeting TechniquesДокумент3 страницыCapital Budgeting TechniquesPrateek YadavОценок пока нет

- Unit 2 Capital BudgetingДокумент24 страницыUnit 2 Capital BudgetingShreya DikshitОценок пока нет

- Capital Investment Factors - UST2021Документ19 страницCapital Investment Factors - UST2021Ey B0ssОценок пока нет

- Captai Budgeting AssignmentДокумент2 страницыCaptai Budgeting AssignmentPravanjan AumcapОценок пока нет

- Presentation On: Capital BudgetingДокумент23 страницыPresentation On: Capital Budgetingakhil_247Оценок пока нет

- CAPITAL BUDGETING LECTURE NOTES MAY 22 - DodomaДокумент5 страницCAPITAL BUDGETING LECTURE NOTES MAY 22 - DodomachabeОценок пока нет

- Capital BudgetingДокумент26 страницCapital BudgetingTisha SosaОценок пока нет

- Capital Investment Decisions: Chapte RДокумент95 страницCapital Investment Decisions: Chapte RMohammad Salim HossainОценок пока нет

- 09.1 Module in Financial Management 09Документ8 страниц09.1 Module in Financial Management 09Fire burnОценок пока нет

- BUAD 839 ASSIGNMENT (Group F)Документ4 страницыBUAD 839 ASSIGNMENT (Group F)Yemi Jonathan OlusholaОценок пока нет

- Vinay ProjectДокумент55 страницVinay ProjectD Priyanka100% (1)

- Assignment - Capital BudgetingДокумент9 страницAssignment - Capital BudgetingSahid KarimbanakkalОценок пока нет

- Financial Analysis: Alka Assistant Director Power System Training Institute BangaloreДокумент40 страницFinancial Analysis: Alka Assistant Director Power System Training Institute Bangaloregaurang1111Оценок пока нет

- Villa, Jesson Bsa2a Finman Information SheetДокумент4 страницыVilla, Jesson Bsa2a Finman Information SheetJESSON VILLAОценок пока нет

- Module 9Документ32 страницыModule 9Precious GiftsОценок пока нет

- Business Finance Investment Decision: Lecturer: Hibak A. NouhДокумент21 страницаBusiness Finance Investment Decision: Lecturer: Hibak A. NouhHibaaq AxmedОценок пока нет

- Capitalbudgeting 1227282768304644 8Документ27 страницCapitalbudgeting 1227282768304644 8durgesh dhumalОценок пока нет

- Evaluation of Capital Budgeting TechniquesДокумент36 страницEvaluation of Capital Budgeting TechniquesAshish GoelОценок пока нет

- Techniques of Investment AnalysisДокумент32 страницыTechniques of Investment AnalysisPranjal Verma0% (1)

- Capital Budgeting and Investment Analysis Question and AnswersДокумент12 страницCapital Budgeting and Investment Analysis Question and AnswersPushpendra Singh ShekhawatОценок пока нет

- Capital Investment Analysis: Reviewing The ChapterДокумент3 страницыCapital Investment Analysis: Reviewing The ChapterRea Mariz JordanОценок пока нет

- FFM Chapter 8Документ5 страницFFM Chapter 8Dawn CaldeiraОценок пока нет

- Capital Budgeting or InvesmentДокумент6 страницCapital Budgeting or Invesmenttkt ecОценок пока нет

- Investment Appraisal: Qs 435 Construction ECONOMICS IIДокумент38 страницInvestment Appraisal: Qs 435 Construction ECONOMICS IIGithu RobertОценок пока нет

- Capital BudgetingДокумент10 страницCapital BudgetingAnkit SathyaОценок пока нет

- Financial Management Case Study-2 The Investment DetectiveДокумент9 страницFinancial Management Case Study-2 The Investment DetectiveSushmita DikshitОценок пока нет

- Concept of Capital Budgeting: Capital Budgeting Is A Process of Planning That Is Used To AscertainДокумент11 страницConcept of Capital Budgeting: Capital Budgeting Is A Process of Planning That Is Used To AscertainLeena SachdevaОценок пока нет

- Investment Evaluation CriteriaДокумент15 страницInvestment Evaluation Criteriainq33108Оценок пока нет

- Capital Budgeting: Mrs Smita DayalДокумент23 страницыCapital Budgeting: Mrs Smita Dayalkaran katariaОценок пока нет

- CapitДокумент8 страницCapitjanice100% (1)

- Format of Project ReportДокумент3 страницыFormat of Project ReportalanОценок пока нет

- Unit 6 - Investment DecisionsДокумент28 страницUnit 6 - Investment Decisions2154 taibakhatunОценок пока нет

- Capital BudgetingДокумент35 страницCapital BudgetingShivam Goel100% (1)

- IRR, NPV and PBPДокумент13 страницIRR, NPV and PBPRajesh Shrestha100% (5)

- Applied Corporate Finance. What is a Company worth?От EverandApplied Corporate Finance. What is a Company worth?Рейтинг: 3 из 5 звезд3/5 (2)

- S. No. Name of The Faculty No. of Hours Handle D Initial of Facult yДокумент3 страницыS. No. Name of The Faculty No. of Hours Handle D Initial of Facult yNagarajan CheyurОценок пока нет

- BrochureДокумент4 страницыBrochureNagarajan CheyurОценок пока нет

- Calculation of InflationДокумент1 страницаCalculation of InflationNagarajan CheyurОценок пока нет

- Internet ProjectДокумент1 страницаInternet ProjectNagarajan CheyurОценок пока нет

- What Is Online Live Projects DevelopmentДокумент4 страницыWhat Is Online Live Projects DevelopmentNagarajan CheyurОценок пока нет

- ResearchДокумент9 страницResearchNagarajan CheyurОценок пока нет

- Chevron Philippines, Inc. vs. Bases Conversion Development Authority and Clark Development Corporation, G.R. No. 173863, September 15, 2010Документ1 страницаChevron Philippines, Inc. vs. Bases Conversion Development Authority and Clark Development Corporation, G.R. No. 173863, September 15, 2010Jeselle Ann VegaОценок пока нет

- Petty CashДокумент5 страницPetty CashBeyy Du BermoyОценок пока нет

- Name: Grade & Section: Score: Date:: Fundamentals of Accountancy and Business Management 2Документ7 страницName: Grade & Section: Score: Date:: Fundamentals of Accountancy and Business Management 2Twelve Forty-fourОценок пока нет

- CoMa Quiz 2Документ21 страницаCoMa Quiz 2Antriksh JohriОценок пока нет

- Ind As & Ifrs Unit 3Документ10 страницInd As & Ifrs Unit 3Dhatri LОценок пока нет

- Shareholders Equity NotesДокумент52 страницыShareholders Equity NotesDeepen Yay NebhwaniОценок пока нет

- UNIT 5.3: Break-Even AnalysisДокумент11 страницUNIT 5.3: Break-Even AnalysisSachin SahooОценок пока нет

- Internship Report On HBLДокумент79 страницInternship Report On HBLbbaahmad89Оценок пока нет

- Van - Oord - India P - LTD - 2023 - 155 - Taxmann - Com - 462 - Mumbai ITATДокумент9 страницVan - Oord - India P - LTD - 2023 - 155 - Taxmann - Com - 462 - Mumbai ITATAjay RottiОценок пока нет

- Major Companies Romania 2012 WebДокумент228 страницMajor Companies Romania 2012 WebTREND_7425Оценок пока нет

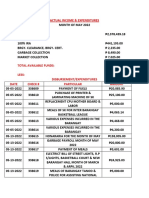

- Actual Income & ExpendituresДокумент5 страницActual Income & Expendituressan nicolas 2nd betis guagua pampangaОценок пока нет

- Cafe Paradiso Sample Business PlanДокумент48 страницCafe Paradiso Sample Business Planehsaanuk100% (6)

- Definition of MOOC - Loosely Defined As Online Courses Aimed at Large-Scale Interaction, Were SeenДокумент6 страницDefinition of MOOC - Loosely Defined As Online Courses Aimed at Large-Scale Interaction, Were SeenRajkumarОценок пока нет

- Circular - 109-03-2009-STДокумент2 страницыCircular - 109-03-2009-STjayamurli19547922100% (2)

- Sugar Cane Plantation and Processing in EthiopiaДокумент13 страницSugar Cane Plantation and Processing in EthiopiaEduardo AlcivarОценок пока нет

- A Dissertation Report OnДокумент111 страницA Dissertation Report OnshashankОценок пока нет

- Managing Liabilities and The Cost of FundsДокумент74 страницыManaging Liabilities and The Cost of FundsFrances Nicole MuldongОценок пока нет

- Loreal RisksДокумент16 страницLoreal RisksSofi_Smith100% (2)

- International Entry Modes: Shikha SharmaДокумент32 страницыInternational Entry Modes: Shikha SharmashikhagrawalОценок пока нет

- Second National Labour CommissionДокумент18 страницSecond National Labour CommissionAnirban ChakrabortyОценок пока нет

- Cost Accounting 3Документ13 страницCost Accounting 3Frenz VerdidaОценок пока нет

- CHAPTER 7 - Competition and Policies Toward Monopolies and Oligopolies Privatization and DeregulationДокумент30 страницCHAPTER 7 - Competition and Policies Toward Monopolies and Oligopolies Privatization and DeregulationCharlie Magne G. Santiaguel90% (10)

- LiabilitiesДокумент5 страницLiabilitiesmalaya negadОценок пока нет

- Funds Flow StatementДокумент67 страницFunds Flow Statementtulasinad123Оценок пока нет

- Embargo - Exhibit 99.3 FinalДокумент20 страницEmbargo - Exhibit 99.3 FinalABC Action NewsОценок пока нет

- Marginal Costing For Decision Making & CVP Analysis - BudgetingДокумент15 страницMarginal Costing For Decision Making & CVP Analysis - BudgetingSravya MagantiОценок пока нет

- Acm 701 2017-18-1-1-2Документ13 страницAcm 701 2017-18-1-1-2Utkarsh Kumar SrivastavОценок пока нет

- Analysis of The Competitive EnvironmentДокумент46 страницAnalysis of The Competitive Environmentshivbab1Оценок пока нет

- BIR FORM 1902 - Application For RegistrationДокумент1 страницаBIR FORM 1902 - Application For RegistrationJenny Racadio100% (1)

- Accounting For ManagersДокумент14 страницAccounting For ManagersKabo Lucas67% (3)