Вам также может понравиться

- Oil Well, Refinery Machinery & Equipment Wholesale Revenues World Summary: Market Values & Financials by CountryОт EverandOil Well, Refinery Machinery & Equipment Wholesale Revenues World Summary: Market Values & Financials by CountryОценок пока нет

- Pumps World Summary: Market Values & Financials by CountryОт EverandPumps World Summary: Market Values & Financials by CountryОценок пока нет

- Acct 2020 Excel Budget Problem Student Template 1 AutosavedДокумент10 страницAcct 2020 Excel Budget Problem Student Template 1 Autosavedapi-273073964Оценок пока нет

- Accounting Excel Budget ProjectДокумент8 страницAccounting Excel Budget Projectapi-242531880Оценок пока нет

- Acct 2020 Excel Budget ProblemДокумент10 страницAcct 2020 Excel Budget Problemapi-325362908Оценок пока нет

- Acct 2020 Emily RufenerДокумент4 страницыAcct 2020 Emily Rufenerapi-284746082Оценок пока нет

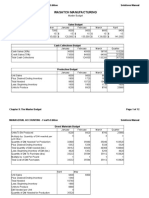

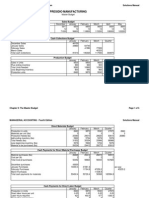

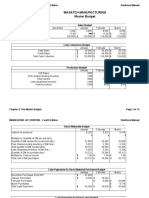

- Wasatch Manufacturing Master Budget: Managerial Accounting - Fourth Edition Solutions ManualДокумент12 страницWasatch Manufacturing Master Budget: Managerial Accounting - Fourth Edition Solutions Manualapi-242429455Оценок пока нет

- Acct 2020 Excel Budget Problem FinalДокумент12 страницAcct 2020 Excel Budget Problem Finalapi-301816205Оценок пока нет

- Acct 2020 Excel Budget Problem Student TemplateДокумент12 страницAcct 2020 Excel Budget Problem Student Templateapi-249190933Оценок пока нет

- Tori Kallerud Chapter 9 HWДокумент12 страницTori Kallerud Chapter 9 HWapi-325347697Оценок пока нет

- p9-60b TemplateДокумент5 страницp9-60b Templateapi-253078310Оценок пока нет

- Acct 2020 Excel Budget Problem Student TemplateДокумент12 страницAcct 2020 Excel Budget Problem Student Templateapi-242720692Оценок пока нет

- Wasatch Manufacturing Master Budget: Managerial Accounting - Fourth Edition Solutions ManualДокумент12 страницWasatch Manufacturing Master Budget: Managerial Accounting - Fourth Edition Solutions Manualapi-269073570Оценок пока нет

- Accounting Chapter 9 Eportfolio ExcelДокумент12 страницAccounting Chapter 9 Eportfolio Excelapi-273030710Оценок пока нет

- Final Project Master Budget by Amit ShankarДокумент9 страницFinal Project Master Budget by Amit Shankarapi-242858911Оценок пока нет

- Chapter 16Документ8 страницChapter 16Rahila RafiqОценок пока нет

- Wasatch Manufacturing Master Budget Q1 2015: Managerial Accounting - Fourth Edition Solutions ManualДокумент12 страницWasatch Manufacturing Master Budget Q1 2015: Managerial Accounting - Fourth Edition Solutions Manualapi-247933607Оценок пока нет

- p9-60 PsimasinghДокумент8 страницp9-60 Psimasinghapi-241811190Оценок пока нет

- Acct 2020 Excel Budget ProblemДокумент4 страницыAcct 2020 Excel Budget Problemapi-241815288Оценок пока нет

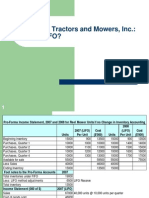

- FDP - Merrimack Tractors and Mowers, Inc.Документ13 страницFDP - Merrimack Tractors and Mowers, Inc.Devyani SinghОценок пока нет

- Master Budget Assignment CH 9Документ4 страницыMaster Budget Assignment CH 9api-240741436Оценок пока нет

- ch9 Final EditionДокумент6 страницch9 Final Editionapi-291516969Оценок пока нет

- EportfolioДокумент8 страницEportfolioapi-220792970Оценок пока нет

- Wasatch Manufacturing: Managerial Accounting - Fourth Edition Solutions ManualДокумент5 страницWasatch Manufacturing: Managerial Accounting - Fourth Edition Solutions Manualapi-284934265Оценок пока нет

- Wasatch Manufacturing Master Budget: Managerial Accounting - Fourth Edition Solutions ManualДокумент4 страницыWasatch Manufacturing Master Budget: Managerial Accounting - Fourth Edition Solutions Manualapi-240678692Оценок пока нет

- Wasatch ManufacturingДокумент12 страницWasatch Manufacturingapi-301899907Оценок пока нет

- Chapter 15Документ7 страницChapter 15Rahila RafiqОценок пока нет

- Acct 2020 Excel Budget Problem Student TemplateДокумент12 страницAcct 2020 Excel Budget Problem Student Templateapi-278341046Оценок пока нет

- Wasatch Manufacturing Master BudgetДокумент6 страницWasatch Manufacturing Master Budgetapi-255137286Оценок пока нет

- Financial WorkingДокумент3 страницыFinancial WorkingSiddiqui FaizanОценок пока нет

- Excel HomeworkДокумент9 страницExcel Homeworkapi-248528639Оценок пока нет

- Master BudgetДокумент4 страницыMaster Budgetapi-233205686Оценок пока нет

- MACS WAC Waltham Motors 12040029Документ5 страницMACS WAC Waltham Motors 12040029Zargham ShiraziОценок пока нет

- WilmontДокумент4 страницыWilmontAbinash BeheraОценок пока нет

- Carolyn Trowbridge Acct 2020 Excel Budget Problem Student Template 1Документ8 страницCarolyn Trowbridge Acct 2020 Excel Budget Problem Student Template 1api-284502690Оценок пока нет

- Vakho Tako SalomeДокумент27 страницVakho Tako SalomerbegalashviliОценок пока нет

- Prepare The Contribution Margin Income StatementДокумент4 страницыPrepare The Contribution Margin Income StatementCorvitz SamaritaОценок пока нет

- Book 1Документ2 страницыBook 1tuanОценок пока нет

- Coma - BlackHeath Manufacturing Company - Revisited (Has Errors)Документ44 страницыComa - BlackHeath Manufacturing Company - Revisited (Has Errors)Nitin Gavishter100% (1)

- Sales Budget Q1 Q2 Q3 Q4 Tottal Sales Unit 2500 2500 2500 2500 10000 800 800 800 800 800 2000000 2000000 2000000 2000000 8000000Документ4 страницыSales Budget Q1 Q2 Q3 Q4 Tottal Sales Unit 2500 2500 2500 2500 10000 800 800 800 800 800 2000000 2000000 2000000 2000000 8000000Kasim MalikОценок пока нет

- Hailey Fernelius ch9 Excel ProjectДокумент4 страницыHailey Fernelius ch9 Excel Projectapi-242652884Оценок пока нет

- Chapter 9 Excel Budget AssignmentДокумент4 страницыChapter 9 Excel Budget Assignmentapi-261038165Оценок пока нет

- New Microsoft Office Excel WorksheetДокумент4 страницыNew Microsoft Office Excel WorksheetFaiz AhmedОценок пока нет

- Cost Accounting 9 EditionДокумент11 страницCost Accounting 9 EditionRahila RafiqОценок пока нет

- Lady M Case - 08.07.2016Документ14 страницLady M Case - 08.07.2016Sabyasachi Mukerji40% (5)

- Wasatch Manufacturing: Managerial Accounting - Fourth Edition Solutions ManualДокумент10 страницWasatch Manufacturing: Managerial Accounting - Fourth Edition Solutions Manualapi-231890132100% (1)

- Sales (17143 99) 1697157 Less: Cost of Goods SoldДокумент5 страницSales (17143 99) 1697157 Less: Cost of Goods SoldSacrosanct Shahzaib BrooklynОценок пока нет

- Hardhat LTDДокумент4 страницыHardhat LTDSonaliОценок пока нет

- Financial PlanДокумент6 страницFinancial PlanRishika ShuklaОценок пока нет

- Financial Analysis: BALANCE SHEET (Construction Period) Liabilities Amount Assets AmountДокумент4 страницыFinancial Analysis: BALANCE SHEET (Construction Period) Liabilities Amount Assets Amountayushcool_00079934Оценок пока нет

- Management AccountingДокумент12 страницManagement AccountingKathlyn Ann MasilОценок пока нет

- Wasatch Manufacturing Master Budget: Managerial Accounting - Fourth Edition Solutions ManualДокумент12 страницWasatch Manufacturing Master Budget: Managerial Accounting - Fourth Edition Solutions Manualapi-239130031Оценок пока нет

- Merrimack Tractors and Mowers - LIFO or FIFOДокумент2 страницыMerrimack Tractors and Mowers - LIFO or FIFOPonu RanjanОценок пока нет

- Chapter 4 SolutionsДокумент12 страницChapter 4 SolutionsSoshiОценок пока нет

- Britannia DCF CapmДокумент12 страницBritannia DCF CapmRohit Kamble100% (1)

- Excell Budget Assignment-Master BudgetДокумент6 страницExcell Budget Assignment-Master Budgetapi-213470756Оценок пока нет

- Matzusry9theditionsolutions 131114003908 Phpapp01 140411230630 Phpapp01Документ101 страницаMatzusry9theditionsolutions 131114003908 Phpapp01 140411230630 Phpapp01Arslan AshfaqОценок пока нет

- Materials Handling Equipment Wholesale Revenues World Summary: Market Values & Financials by CountryОт EverandMaterials Handling Equipment Wholesale Revenues World Summary: Market Values & Financials by CountryОценок пока нет

- Fuel Pumps & Fuel Tanks (C.V. OE & Aftermarket) World Summary: Market Values & Financials by CountryОт EverandFuel Pumps & Fuel Tanks (C.V. OE & Aftermarket) World Summary: Market Values & Financials by CountryОценок пока нет

- Lathes World Summary: Market Sector Values & Financials by CountryОт EverandLathes World Summary: Market Sector Values & Financials by CountryОценок пока нет

- Acct 2020 Excel Budget Problem Description Master Version BДокумент7 страницAcct 2020 Excel Budget Problem Description Master Version Bapi-237087046Оценок пока нет

- Immigration Policy and Its Effects On The Economy - Patricia HallДокумент5 страницImmigration Policy and Its Effects On The Economy - Patricia Hallapi-237087046Оценок пока нет

- Patricia: (801) XXX-XXXXДокумент1 страницаPatricia: (801) XXX-XXXXapi-237087046Оценок пока нет

- Rhetorical Summary For Choosing Death by Nicholas D KristofДокумент4 страницыRhetorical Summary For Choosing Death by Nicholas D Kristofapi-237087046Оценок пока нет

- Books For TNPSCДокумент9 страницBooks For TNPSCAiam PandianОценок пока нет

- Reliability Evaluation of Grid-Connected Photovoltaic Power SystemsДокумент32 страницыReliability Evaluation of Grid-Connected Photovoltaic Power Systemssamsai88850% (2)

- 12 CONFUCIUS SY 2O23 For Insurance GPA TemplateДокумент9 страниц12 CONFUCIUS SY 2O23 For Insurance GPA TemplateIris Kayte Huesca EvicnerОценок пока нет

- MBBS MO OptionsДокумент46 страницMBBS MO Optionskrishna madkeОценок пока нет

- Pye, D.-1968-The Nature and Art of WorkmanshipДокумент22 страницыPye, D.-1968-The Nature and Art of WorkmanshipecoaletОценок пока нет

- Cir v. Citytrust InvestmentДокумент12 страницCir v. Citytrust InvestmentJor LonzagaОценок пока нет

- ISO Hole Limits TolerancesДокумент6 страницISO Hole Limits ToleranceskumarОценок пока нет

- Rich Dad Poor Dad: Book SummaryДокумент7 страницRich Dad Poor Dad: Book SummarySnehal YagnikОценок пока нет

- Sales Quotation: Kind Attn:: TelДокумент2 страницыSales Quotation: Kind Attn:: Telkiran rayan euОценок пока нет

- The Vertical Garden City: Towards A New Urban Topology: Chris AbelДокумент11 страницThe Vertical Garden City: Towards A New Urban Topology: Chris AbelDzemal SkreboОценок пока нет

- Table of ContentsДокумент6 страницTable of ContentsRakeshKumarОценок пока нет

- Extracted Pages From May-2023Документ4 страницыExtracted Pages From May-2023Muhammad UsmanОценок пока нет

- Certificate of Origin: Issued by The Busan Chamber of Commerce & IndustryДокумент11 страницCertificate of Origin: Issued by The Busan Chamber of Commerce & IndustryVu Thuy LinhОценок пока нет

- Mariana Mazzucato - The Value of Everything. Making and Taking in The Global Economy (2018, Penguin)Документ318 страницMariana Mazzucato - The Value of Everything. Making and Taking in The Global Economy (2018, Penguin)Jorge Echavarría Carvajal100% (19)

- PNB v. AtendidoДокумент2 страницыPNB v. AtendidoAntonio RebosaОценок пока нет

- Position PaperДокумент2 страницыPosition PaperMaria Marielle BucksОценок пока нет

- de Thi Chon HSG 8 - inДокумент4 страницыde Thi Chon HSG 8 - inPhương Chi NguyễnОценок пока нет

- Gold and InflationДокумент25 страницGold and InflationRaghu.GОценок пока нет

- 8 Trdln0610saudiДокумент40 страниц8 Trdln0610saudiJad SoaiОценок пока нет

- Report On Brick - 1Документ6 страницReport On Brick - 1Meghashree100% (1)

- 11th 12th Economics Q EM Sample PagesДокумент27 страниц11th 12th Economics Q EM Sample PagesKirthika RajaОценок пока нет

- Sim CBM 122 Lesson 3Документ9 страницSim CBM 122 Lesson 3Andrew Sy ScottОценок пока нет

- Apply Online Pradhan Mantri Awas Yojana (PMAY) Gramin (Application Form 2017) Using Pmaymis - Housing For All 2022 Scheme - PM Jan Dhan Yojana PDFДокумент103 страницыApply Online Pradhan Mantri Awas Yojana (PMAY) Gramin (Application Form 2017) Using Pmaymis - Housing For All 2022 Scheme - PM Jan Dhan Yojana PDFAnonymous dxsNnL6S8h0% (1)

- 13 Chapter V (Swot Analysis and Compitetor Analysis)Документ3 страницы13 Chapter V (Swot Analysis and Compitetor Analysis)hari tejaОценок пока нет

- Dornbusch Overshooting ModelДокумент17 страницDornbusch Overshooting Modelka2010cheungОценок пока нет

- Impact of Covid-19.Документ6 страницImpact of Covid-19.Pratik WankhedeОценок пока нет

- Chapter 01 - PowerPoint - Introduction To Taxation in Canada - 2013Документ32 страницыChapter 01 - PowerPoint - Introduction To Taxation in Canada - 2013melsun007Оценок пока нет

- Abstract, Attestation & AcknowledgementДокумент6 страницAbstract, Attestation & AcknowledgementDeedar.RaheemОценок пока нет

- Analysis of Monetary Policy of IndiaДокумент18 страницAnalysis of Monetary Policy of IndiaShashwat TiwariОценок пока нет

- Revised Analyst's Dilemma Analysis Pallab MishraДокумент2 страницыRevised Analyst's Dilemma Analysis Pallab Mishrapalros100% (1)