Вам также может понравиться

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Bank Statement PDFДокумент5 страницBank Statement PDFIrfanLoneОценок пока нет

- Biblical Strategies For Financial Recovery & RestorationДокумент14 страницBiblical Strategies For Financial Recovery & RestorationIsaac Abayomi OshinОценок пока нет

- Chapter 10 - Contract Catering (Non-Crl) : Sponsor - DIOДокумент8 страницChapter 10 - Contract Catering (Non-Crl) : Sponsor - DIOCANDYОценок пока нет

- Case Study Ratio AnalysisДокумент6 страницCase Study Ratio Analysisash867240% (1)

- Accounting Concepts and ConventionsДокумент22 страницыAccounting Concepts and ConventionsMishal SiddiqueОценок пока нет

- Tata Consultancy Services Ltd. Company AnalysisДокумент70 страницTata Consultancy Services Ltd. Company AnalysisPiyush ThakarОценок пока нет

- BSBTEC601 - Review Organisational Digital Strategy: Task SummaryДокумент8 страницBSBTEC601 - Review Organisational Digital Strategy: Task SummaryHabibi AliОценок пока нет

- Batch Process Presentation)Документ17 страницBatch Process Presentation)Telse Simon100% (1)

- Financial Accounting Theory Craig Deegan Chapter 8Документ47 страницFinancial Accounting Theory Craig Deegan Chapter 8Rob26in0983% (6)

- Forensic AccountingДокумент30 страницForensic Accountingparth_upadhyay_1Оценок пока нет

- Complete Revision Notes Auditing 1Документ90 страницComplete Revision Notes Auditing 1Marwin Ace100% (1)

- Creative AccountingДокумент40 страницCreative AccountingAirlanggaZakyОценок пока нет

- Sunday School Exam Papers-2Документ7 страницSunday School Exam Papers-2Harshini Ramas0% (2)

- Chapter 3 Fundamentals of Organization StructureДокумент21 страницаChapter 3 Fundamentals of Organization StructureKaye Adriana GoОценок пока нет

- ACC518 - Topic 09 - Critical Perspectives in AccountingДокумент22 страницыACC518 - Topic 09 - Critical Perspectives in AccountingRitesh Kumar Dubey100% (1)

- Financial Accounting Theory Craig Deegan Chapter 11Документ22 страницыFinancial Accounting Theory Craig Deegan Chapter 11Rob26in09100% (1)

- Accounts UNIT 1Документ13 страницAccounts UNIT 1ayushi dagarОценок пока нет

- Cecchetti 6e Chapter 02Документ46 страницCecchetti 6e Chapter 02Karthik LakshminarayanОценок пока нет

- Creative Accounting Tutor Master PDFДокумент12 страницCreative Accounting Tutor Master PDFJojo Josepha MariaОценок пока нет

- Chapter 2 Shipyard-Layout Lecture Notes From South Hampton UniversityДокумент10 страницChapter 2 Shipyard-Layout Lecture Notes From South Hampton UniversityJonnada KumarОценок пока нет

- Igcse Economics Revision NotesДокумент11 страницIgcse Economics Revision NotesJakub Kotas-Cvrcek100% (1)

- The Acceptance Level On GST Implementation in Malaysia: Gading Journal For The Social Sciences Vol 1 No 2 (2016)Документ6 страницThe Acceptance Level On GST Implementation in Malaysia: Gading Journal For The Social Sciences Vol 1 No 2 (2016)Harshini RamasОценок пока нет

- Unethical Business PracticesДокумент13 страницUnethical Business PracticesDheerajKumar100% (2)

- 2011 Accounting Standards in NigeriaДокумент70 страниц2011 Accounting Standards in Nigeriaoluomo1100% (1)

- Accounting Theory Approach PDFДокумент104 страницыAccounting Theory Approach PDFabiyya salsabilОценок пока нет

- Ch1 Financial Accounting and Accounting StandardsДокумент19 страницCh1 Financial Accounting and Accounting Standardssomething82Оценок пока нет

- Creative AccountingДокумент13 страницCreative Accountinghhazlina66Оценок пока нет

- Creative AccountingДокумент13 страницCreative AccountingMira CE100% (1)

- Creative - Accounting - Ms - Saloni Gupta & DR - Reshma RajaniДокумент9 страницCreative - Accounting - Ms - Saloni Gupta & DR - Reshma Rajanisalonigupta3Оценок пока нет

- Creative Accounting and Accounting Scandals: Case Lets of Indian CompaniesДокумент4 страницыCreative Accounting and Accounting Scandals: Case Lets of Indian Companiespranshu jaiswalОценок пока нет

- The Rise and Fall of Management AccountingДокумент9 страницThe Rise and Fall of Management AccountingHarshini RamasОценок пока нет

- Creative AccountingДокумент8 страницCreative AccountingRadhakrishna MishraОценок пока нет

- Corporate Governance and Creative AccountingДокумент10 страницCorporate Governance and Creative AccountingqwertyОценок пока нет

- Abstract This Study Was Designed To Establish The Effect of Creative Accounting On ShareholdersДокумент10 страницAbstract This Study Was Designed To Establish The Effect of Creative Accounting On ShareholdersAhmad KamalОценок пока нет

- Challenges of Ipsas Implementation in TanzaniaДокумент17 страницChallenges of Ipsas Implementation in TanzaniaSteven Kisamo Ambrose100% (5)

- Creative Accounting: Just or UnjustДокумент38 страницCreative Accounting: Just or Unjustfaraazxbox1100% (1)

- Creative Accounting, Ethics and Professional DevelomentДокумент21 страницаCreative Accounting, Ethics and Professional DevelomentFaiz FaisalОценок пока нет

- Creative Accounting - Thesis Discussion PDFДокумент38 страницCreative Accounting - Thesis Discussion PDFStefanus ardhanovaОценок пока нет

- Creative AccountingДокумент7 страницCreative Accountingeugeniastefania raduОценок пока нет

- Creative Accounting: A Literature ReviewДокумент13 страницCreative Accounting: A Literature ReviewthesijОценок пока нет

- Creative Accounting-Earning ManagementДокумент17 страницCreative Accounting-Earning ManagementAssad RafaqОценок пока нет

- Creative Accounting: & Earnings ManagementДокумент29 страницCreative Accounting: & Earnings ManagementrasheshpatelОценок пока нет

- Creative AccountingДокумент8 страницCreative Accountingpriteshvadera18791Оценок пока нет

- cREATIVE ACCOUNTINGДокумент12 страницcREATIVE ACCOUNTINGAshraful Jaygirdar0% (1)

- ACC702 Course Material & Study GuideДокумент78 страницACC702 Course Material & Study Guidelaukkeas100% (4)

- Chap 1 - Text Accounting TheoryДокумент36 страницChap 1 - Text Accounting TheoryAhmadYaseen100% (2)

- The Concept of Going ConcernДокумент6 страницThe Concept of Going ConcernMarilou Olaguir SañoОценок пока нет

- Lecture 11 - Audit in Public SectorДокумент56 страницLecture 11 - Audit in Public SectorChuah Chong Ann100% (2)

- CH 5 Accounting VeiwpointsДокумент12 страницCH 5 Accounting Veiwpointslenalena123100% (1)

- Accounting Theory Alumina CaseДокумент3 страницыAccounting Theory Alumina CaseLutfiana HermawatiОценок пока нет

- Principle-Based vs. Rule-Based AccountingДокумент2 страницыPrinciple-Based vs. Rule-Based AccountingPeter MastersОценок пока нет

- Development and Contemporary Issues in Management AccountingДокумент15 страницDevelopment and Contemporary Issues in Management AccountingFaizah MK67% (3)

- Decisions Under Risk and UncertaintyДокумент18 страницDecisions Under Risk and UncertaintyGloria JohnsonОценок пока нет

- 1-Introduction-to-StatisticsДокумент6 страниц1-Introduction-to-StatisticsMD TausifОценок пока нет

- Prudence and MatchingДокумент25 страницPrudence and MatchingAbdul_Ghaffar_agkОценок пока нет

- Importance of Accounting DataДокумент6 страницImportance of Accounting DataJawwalVasОценок пока нет

- Accounting Concepts and ConventionsДокумент2 страницыAccounting Concepts and ConventionsWelcome 1995Оценок пока нет

- Creative Accounting and Fraud (Aus) PDFДокумент37 страницCreative Accounting and Fraud (Aus) PDFmbjoshi555100% (1)

- Accounting TheoryДокумент47 страницAccounting Theorychoccolade100% (2)

- Aue2602 Topic 1 Summary PDFДокумент8 страницAue2602 Topic 1 Summary PDFoscar.matenguОценок пока нет

- Cost I Chapter 1Документ13 страницCost I Chapter 1Wonde BiruОценок пока нет

- International Accounting StandardizationДокумент190 страницInternational Accounting StandardizationChartridge Books Oxford100% (1)

- Accounting Theory Construction PDFДокумент23 страницыAccounting Theory Construction PDFPriyathasini ChandranОценок пока нет

- Accounting Ethics and Integrity StandardsДокумент6 страницAccounting Ethics and Integrity StandardsRowie Ann TapiaОценок пока нет

- Studiu de Caz XeroxДокумент10 страницStudiu de Caz XeroxMari TrifuОценок пока нет

- Determinants of Financial StructureДокумент15 страницDeterminants of Financial StructureAlexander DeckerОценок пока нет

- Regulation As Accounting Theory Gaffikiin - ReadДокумент21 страницаRegulation As Accounting Theory Gaffikiin - Reado_rilaОценок пока нет

- Business Strategy and Corporate Governance in the Chinese Consumer Electronics SectorОт EverandBusiness Strategy and Corporate Governance in the Chinese Consumer Electronics SectorОценок пока нет

- Defn CreativeДокумент11 страницDefn CreativeDamulira DavidОценок пока нет

- Shsconf Glob2020 01004Документ8 страницShsconf Glob2020 01004Thiviyani SivaguruОценок пока нет

- 1 s2.0 S1877042814012865 MainДокумент8 страниц1 s2.0 S1877042814012865 MainHarshini RamasОценок пока нет

- 10 1 50 1 10 20170807Документ13 страниц10 1 50 1 10 20170807Harshini RamasОценок пока нет

- Current IssuesДокумент9 страницCurrent IssuesNurulJannah NabihahОценок пока нет

- Audit and Assurance 1 Tutorial Answers PDFДокумент10 страницAudit and Assurance 1 Tutorial Answers PDFHarshini RamasОценок пока нет

- BUS201 202 Tutorial 03 SolutionsДокумент5 страницBUS201 202 Tutorial 03 SolutionsHarshini RamasОценок пока нет

- Megan MediaДокумент8 страницMegan Mediarose0% (1)

- Baby DumpingДокумент7 страницBaby DumpingRoobendhiran SethuramanОценок пока нет

- Business Basics 1.031Документ25 страницBusiness Basics 1.031Harshini RamasОценок пока нет

- QIUP Map 27-12-2012Документ1 страницаQIUP Map 27-12-2012Harshini RamasОценок пока нет

- Ice Cream Shops Final PaperДокумент20 страницIce Cream Shops Final PaperHarshini RamasОценок пока нет

- Armstrongmai12inppt01 141021092459 Conversion Gate02Документ38 страницArmstrongmai12inppt01 141021092459 Conversion Gate02Harshini RamasОценок пока нет

- Faculty of Business, Management and Social Sciences Bba 1103 Microeconomics September Semester 2015 Assignment Submission GuidelineДокумент2 страницыFaculty of Business, Management and Social Sciences Bba 1103 Microeconomics September Semester 2015 Assignment Submission GuidelineHarshini RamasОценок пока нет

- IFRS - The Inevitable Evolution of U.S. Accounting StandardsДокумент15 страницIFRS - The Inevitable Evolution of U.S. Accounting StandardsHarshini RamasОценок пока нет

- Ice Cream Shops Final PaperДокумент20 страницIce Cream Shops Final PaperHarshini RamasОценок пока нет

- Baby DumpingДокумент7 страницBaby DumpingRoobendhiran SethuramanОценок пока нет

- AnalysisДокумент1 страницаAnalysisHarshini RamasОценок пока нет

- Ice Cream Shops Final PaperДокумент20 страницIce Cream Shops Final PaperHarshini RamasОценок пока нет

- Students/: What The Best College Students DoДокумент2 страницыStudents/: What The Best College Students DoHarshini Ramas0% (1)

- Financial Formulas - Ratios (Sheet)Документ3 страницыFinancial Formulas - Ratios (Sheet)carmo-netoОценок пока нет

- IFRS For SMEs in SAДокумент18 страницIFRS For SMEs in SAHarshini Ramas100% (1)

- Itunes Software LicenseДокумент10 страницItunes Software Licensemirtesmarcineiro11Оценок пока нет

- Formula PMRДокумент4 страницыFormula PMRHarshini RamasОценок пока нет

- The Accounting EquationДокумент4 страницыThe Accounting EquationHarshini RamasОценок пока нет

- Pahang JUJ 2012 SPM Maths E15CC44CДокумент120 страницPahang JUJ 2012 SPM Maths E15CC44CHarshini RamasОценок пока нет

- Basic Accounting Concepts 1961Документ50 страницBasic Accounting Concepts 1961kushagra099Оценок пока нет

- Capability Guide NAV2013 R2 HIGHДокумент28 страницCapability Guide NAV2013 R2 HIGHNarendra KulkarniОценок пока нет

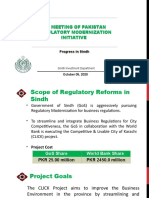

- Reforms Claimed by Provincial BOIs - Oct 219, 2020Документ37 страницReforms Claimed by Provincial BOIs - Oct 219, 2020Naeem AhmedОценок пока нет

- Understanding The Impact of COVID-19 On The Sports IndustryДокумент3 страницыUnderstanding The Impact of COVID-19 On The Sports IndustrySimona CuciureanuОценок пока нет

- JD-Global Lean ManagerДокумент2 страницыJD-Global Lean ManagerHimanshu JaiswalОценок пока нет

- 4strategic Analysis ToolsДокумент14 страниц4strategic Analysis ToolsHannahbea LindoОценок пока нет

- Quezon City Polytechnic University: Entrepreneurial BehaviorДокумент30 страницQuezon City Polytechnic University: Entrepreneurial BehaviorMarinel CorderoОценок пока нет

- Training ReportДокумент51 страницаTraining ReportShikhar SethiОценок пока нет

- Final Case Study Reqmt UnileverДокумент18 страницFinal Case Study Reqmt UnileverEarl Condeza100% (1)

- Avantage ESA95vsCashaccountingДокумент14 страницAvantage ESA95vsCashaccountingthowasОценок пока нет

- Red Ink Flows MateriДокумент15 страницRed Ink Flows MateriVelia MonicaОценок пока нет

- Leadership TeslaДокумент6 страницLeadership TeslaKendice ChanОценок пока нет

- Event After Reporting PeriodДокумент2 страницыEvent After Reporting PeriodHuỳnh Minh Gia HàoОценок пока нет

- Bill of Exchange 078Документ1 страницаBill of Exchange 078trung2iОценок пока нет

- Form 1 - Illustration Income Tax: For Individuals Earning Purely Compensation Income Accomplish BIR Form No. - 1700Документ3 страницыForm 1 - Illustration Income Tax: For Individuals Earning Purely Compensation Income Accomplish BIR Form No. - 1700Rea Rose TampusОценок пока нет

- Practical Guidelines in Reducing and Managing Business RisksДокумент6 страницPractical Guidelines in Reducing and Managing Business RisksSherilyn PicarraОценок пока нет

- Compensation 5Документ10 страницCompensation 5Pillos Jr., ElimarОценок пока нет

- Icici Bank Videocon Bribery Case A Case Analysis in Reference To Corporate GovernanceДокумент8 страницIcici Bank Videocon Bribery Case A Case Analysis in Reference To Corporate GovernanceSuneethaJagadeeshОценок пока нет

- Management Final Paper 27062020 044941pm PDFДокумент8 страницManagement Final Paper 27062020 044941pm PDFHuzaifa KhanОценок пока нет

- Customer Relationship and Wealth ManagementДокумент65 страницCustomer Relationship and Wealth ManagementbistamasterОценок пока нет

- Strategy Implementation - WalMartДокумент11 страницStrategy Implementation - WalMartSatyajitBeheraОценок пока нет