Вам также может понравиться

- Estmt - 2022 03 31Документ12 страницEstmt - 2022 03 31Laura MCGОценок пока нет

- Account Summary - 7902819734Документ2 страницыAccount Summary - 7902819734Heather Franks0% (1)

- Release 13 21.B UK Payroll SetupДокумент146 страницRelease 13 21.B UK Payroll SetupKiran JОценок пока нет

- Invoice Zoom YKB 2022Документ2 страницыInvoice Zoom YKB 2022Dian ElgaОценок пока нет

- 0af1012a0000000409264 ESTATEMENT 082022 0af1012a00000004Документ4 страницы0af1012a0000000409264 ESTATEMENT 082022 0af1012a00000004Rahul RajОценок пока нет

- FlexiДокумент4 страницыFlexiManish Mani100% (1)

- Taxa TionДокумент24 страницыTaxa TionkannadhassОценок пока нет

- Prelim. Module 2. Lesson 5 - 8 Rate, Tax, and Expenses (Legal Aspects) PDFДокумент6 страницPrelim. Module 2. Lesson 5 - 8 Rate, Tax, and Expenses (Legal Aspects) PDFMARITONI MEDALLAОценок пока нет

- INFINITI RETAIL LIMITED (Trading As Cromā) : Tax InvoiceДокумент3 страницыINFINITI RETAIL LIMITED (Trading As Cromā) : Tax Invoice2018hw70285Оценок пока нет

- Taxation Suggested Solution: LessДокумент9 страницTaxation Suggested Solution: LesskannadhassОценок пока нет

- CIR Vs Soriano TAX DigestДокумент3 страницыCIR Vs Soriano TAX DigestGeorge PandaОценок пока нет

- Draft Thesis E Invoicing 09052022Документ33 страницыDraft Thesis E Invoicing 09052022Michael Jay KennedyОценок пока нет

- Tax PunishmentДокумент7 страницTax PunishmentkannadhassОценок пока нет

- Sciencedirect: The Role of Tax Agents in Sustaining The Malaysian Tax SystemДокумент6 страницSciencedirect: The Role of Tax Agents in Sustaining The Malaysian Tax SystemNadiatul WardinaОценок пока нет

- Stella Work 3Документ20 страницStella Work 3Cletus OgeibiriОценок пока нет

- Fraser Institute: The Cost To Canadians of Complying With Personal Income TaxesДокумент53 страницыFraser Institute: The Cost To Canadians of Complying With Personal Income TaxesInvestor Relations VancouverОценок пока нет

- Tax Knowledge, Tax Complexity and Tax Compliance: Taxpayers' ViewДокумент7 страницTax Knowledge, Tax Complexity and Tax Compliance: Taxpayers' Viewabbey89Оценок пока нет

- Jurnal Internasional Tenang Pajak Di Nigeria - Id.enДокумент8 страницJurnal Internasional Tenang Pajak Di Nigeria - Id.enMrX GamingОценок пока нет

- Dlsu Thesis Paper FormatДокумент7 страницDlsu Thesis Paper Formatkatyanalondonomiramar100% (2)

- EditsДокумент5 страницEditsTanya TanyaОценок пока нет

- Perception of Taxpayers' Towards E-File Adoption: ManagementДокумент8 страницPerception of Taxpayers' Towards E-File Adoption: ManagementVijaykumar ChalwadiОценок пока нет

- Perception of Taxpayers' Towards E-File Adoption: ManagementДокумент8 страницPerception of Taxpayers' Towards E-File Adoption: ManagementVijaykumar ChalwadiОценок пока нет

- "Comparative Study of Physical Filing and E-Filing of Returns Through Spa Capital Services Ltd. A SynopsisДокумент6 страниц"Comparative Study of Physical Filing and E-Filing of Returns Through Spa Capital Services Ltd. A SynopsisriyaОценок пока нет

- Taxation AgentДокумент35 страницTaxation AgentyukeОценок пока нет

- Samuel Tax Fairness Perception and Compliance Behavior PDFДокумент11 страницSamuel Tax Fairness Perception and Compliance Behavior PDFneysaryОценок пока нет

- Categorizing Taxpayers - A Mixed-Method Study On Small Business TaДокумент24 страницыCategorizing Taxpayers - A Mixed-Method Study On Small Business Tala_icankОценок пока нет

- DARSHAN P Project Report On TAX PAYERS PERSEPTION TOWARDS E - FILING SYSTEM OF INCOME TAX" (IN CASE STUDY OF BELLARI CITY)Документ73 страницыDARSHAN P Project Report On TAX PAYERS PERSEPTION TOWARDS E - FILING SYSTEM OF INCOME TAX" (IN CASE STUDY OF BELLARI CITY)DARSHAN PОценок пока нет

- Desrir-Tax Non-Compliance Among Smcs in MalaysiaДокумент23 страницыDesrir-Tax Non-Compliance Among Smcs in Malaysialily suryaniОценок пока нет

- Fountain Journalof Managementand Social SciencesДокумент12 страницFountain Journalof Managementand Social SciencesMebratu BirhanuОценок пока нет

- 2894 5651 1 SMДокумент11 страниц2894 5651 1 SMMuhammad Iqbal Asy SyauqiОценок пока нет

- Impact of Taxation On The Performance On SmesДокумент50 страницImpact of Taxation On The Performance On SmesJulius YarОценок пока нет

- Effect of Taxation Modernization On Tax Compliance: International Research Journal of Management, IT & Social SciencesДокумент7 страницEffect of Taxation Modernization On Tax Compliance: International Research Journal of Management, IT & Social SciencesDaniel MuchaiОценок пока нет

- Public Awareness of TaxДокумент12 страницPublic Awareness of TaxDilli Raj PandeyОценок пока нет

- Factors Affecting Tax Compliance Behaviour in SelfДокумент10 страницFactors Affecting Tax Compliance Behaviour in SelfKhadija SyedОценок пока нет

- 114-Article Text-209-1-10-20201106Документ18 страниц114-Article Text-209-1-10-20201106stunner_1994Оценок пока нет

- Jurnal PajakДокумент12 страницJurnal PajakkrisnasavitriОценок пока нет

- Article On Income Tax Comparison Between India and United StatesДокумент18 страницArticle On Income Tax Comparison Between India and United StatesRohit HalwaiОценок пока нет

- Ifmis ResearchДокумент15 страницIfmis ResearchDavid MichaelsОценок пока нет

- Vetjeh DKK 2022Документ14 страницVetjeh DKK 2022yuliana jaengОценок пока нет

- INCOMETTTTTTTTTДокумент25 страницINCOMETTTTTTTTTJayvee JoseОценок пока нет

- E-Filing of Taxes - A Research PaperДокумент8 страницE-Filing of Taxes - A Research PaperRieke Savitri Agustin0% (1)

- Adoption and Impact of E-AccountingДокумент9 страницAdoption and Impact of E-Accountingsan0z100% (1)

- The Experience of SelfДокумент6 страницThe Experience of SelfAbdulmalik Ibn SalauОценок пока нет

- School of Business and Economics Submitted To: Dr. AbebawДокумент5 страницSchool of Business and Economics Submitted To: Dr. AbebawMarcОценок пока нет

- 1 - Full TextДокумент22 страницы1 - Full TextDI UJUNG PENANTIAN CHANNELОценок пока нет

- 124 425 1 PB1 PDFДокумент26 страниц124 425 1 PB1 PDFKristy Dela CernaОценок пока нет

- E-Filing, Kepatuhan Wajib Pajak, Sosialisasi Perpajakan, Pemahaman InternetДокумент20 страницE-Filing, Kepatuhan Wajib Pajak, Sosialisasi Perpajakan, Pemahaman InternetBaguzОценок пока нет

- JASF Template English Jan2022Документ12 страницJASF Template English Jan2022Rizky Rizky NurdiansyahОценок пока нет

- Measures of Tax Compliance Among Small and Medium Enterprises in Tagum City: An Exploratory Factor AnalysisДокумент10 страницMeasures of Tax Compliance Among Small and Medium Enterprises in Tagum City: An Exploratory Factor AnalysisThe IjbmtОценок пока нет

- BayraktarДокумент7 страницBayraktarKoo KooОценок пока нет

- Design and Development of An E-Taxation System: April 2015Документ26 страницDesign and Development of An E-Taxation System: April 2015Jay ParmarОценок пока нет

- Asgmnt 1Документ5 страницAsgmnt 1shahida_zulkifliОценок пока нет

- Tax Administration Reform in IndiaДокумент26 страницTax Administration Reform in IndiaDwijottam BhattacharjeeОценок пока нет

- Tax Technology, Fairness Perception and Tax Compliance Among Individual TaxpayersДокумент21 страницаTax Technology, Fairness Perception and Tax Compliance Among Individual TaxpayersAudit and Accounting ReviewОценок пока нет

- Issn (P) : 2355-9993 (E) : 2527-953XДокумент13 страницIssn (P) : 2355-9993 (E) : 2527-953Xtaufiq arrahmanОценок пока нет

- Aronmwan Et al-2015-SSRN Electronic JournalДокумент18 страницAronmwan Et al-2015-SSRN Electronic JournalHakeem MichealОценок пока нет

- AMERICAN College of Tecnolg Course Business Research Method Factors That Influence Business Income Taxpayers Compliance in EthiopiaДокумент29 страницAMERICAN College of Tecnolg Course Business Research Method Factors That Influence Business Income Taxpayers Compliance in EthiopiaBewuket MazieОценок пока нет

- Self-Assessment System of Taxation As A Challenge For IndiaДокумент3 страницыSelf-Assessment System of Taxation As A Challenge For IndiaLoukya PabbathiОценок пока нет

- Critical Analysis of Perception of Government Officials in Vidarbha Region Towards Tax Evasion in The Context of Recent Direct Tax CodeДокумент18 страницCritical Analysis of Perception of Government Officials in Vidarbha Region Towards Tax Evasion in The Context of Recent Direct Tax CodeImpact JournalsОценок пока нет

- E Flling of Income TaxДокумент6 страницE Flling of Income TaxVijaykumar ChalwadiОценок пока нет

- Does Tax Knowledge Motivate Tax Compliance in Malaysia?: Research in World Economy Vol. 12, No. 1, Special Issue 2021Документ14 страницDoes Tax Knowledge Motivate Tax Compliance in Malaysia?: Research in World Economy Vol. 12, No. 1, Special Issue 2021Vcnes VikiОценок пока нет

- Ipjas 3 2 2019 4 14Документ11 страницIpjas 3 2 2019 4 14Raga VenthiniОценок пока нет

- Can E-Filing Reduce Tax Compliance Costs in Developing Countries?Документ59 страницCan E-Filing Reduce Tax Compliance Costs in Developing Countries?Ma Joyce ImperialОценок пока нет

- Esut 009Документ11 страницEsut 009paulevbadeeseosaОценок пока нет

- ACCOUNTING AND FINANCE Research WGДокумент12 страницACCOUNTING AND FINANCE Research WGggeb_827217490% (1)

- Journal of Tax Perception and Tax EvasionДокумент15 страницJournal of Tax Perception and Tax EvasionkurniОценок пока нет

- Tax EvasionДокумент21 страницаTax EvasionChelsea BorbonОценок пока нет

- Jurnal Internasional PerpajakanДокумент9 страницJurnal Internasional PerpajakanNurul MutiaraОценок пока нет

- Tax Policy and the Economy, Volume 37От EverandTax Policy and the Economy, Volume 37Robert A. MoffittОценок пока нет

- Tax Policy and the Economy: Volume 32От EverandTax Policy and the Economy: Volume 32Robert A. MoffittОценок пока нет

- A Guide to Ethical Practices in the United States Tax IndustryОт EverandA Guide to Ethical Practices in the United States Tax IndustryОценок пока нет

- 7110 s13 Ms 12Документ2 страницы7110 s13 Ms 12Ahmed JavedОценок пока нет

- 7110 s13 QP 22Документ20 страниц7110 s13 QP 22kannadhassОценок пока нет

- 7110 s13 QP 12 PDFДокумент12 страниц7110 s13 QP 12 PDFkannadhassОценок пока нет

- Accounting WorksheetДокумент2 страницыAccounting WorksheetkannadhassОценок пока нет

- Taxation AnswerДокумент13 страницTaxation AnswerkannadhassОценок пока нет

- 7010 s13 Ms 12Документ17 страниц7010 s13 Ms 12Melvyn MardamootooОценок пока нет

- Ejournal of Tax ResearchДокумент16 страницEjournal of Tax ResearchkannadhassОценок пока нет

- Test 2 Y10Документ3 страницыTest 2 Y10kannadhassОценок пока нет

- L2 Passport To Success Solutions L2 Book-Keeping & Accounts V2Документ81 страницаL2 Passport To Success Solutions L2 Book-Keeping & Accounts V2Loceng RouqianОценок пока нет

- Tax GST PDFДокумент12 страницTax GST PDFkannadhassОценок пока нет

- 7110 w11 QP 21Документ20 страниц7110 w11 QP 21kannadhassОценок пока нет

- Tax Exam AttachementДокумент3 страницыTax Exam AttachementkannadhassОценок пока нет

- Computation of MR Amman Statutory Income From Employment For The Year of Assessment 2015Документ2 страницыComputation of MR Amman Statutory Income From Employment For The Year of Assessment 2015kannadhassОценок пока нет

- Qpe CaДокумент1 страницаQpe CakannadhassОценок пока нет

- Accounts AssignmentДокумент6 страницAccounts AssignmentkannadhassОценок пока нет

- Test 1 Y10Документ3 страницыTest 1 Y10kannadhassОценок пока нет

- Qpe CaДокумент1 страницаQpe CakannadhassОценок пока нет

- MRSM Trial Akaun 2013 - JawapanДокумент20 страницMRSM Trial Akaun 2013 - JawapanLauHuiPingОценок пока нет

- Refferance LetterДокумент3 страницыRefferance LetterkannadhassОценок пока нет

- Day 6 Cash BookДокумент2 страницыDay 6 Cash BookkannadhassОценок пока нет

- AssignmentДокумент5 страницAssignmentkannadhassОценок пока нет

- Taxation - Answer Sept 2012Документ12 страницTaxation - Answer Sept 2012kannadhassОценок пока нет

- Tax 2014Документ12 страницTax 2014kannadhassОценок пока нет

- Tax 2003Документ11 страницTax 2003kannadhassОценок пока нет

- Perniagaan Budak Hensem Am Penghutang Q Penghutang R Penghutang SДокумент66 страницPerniagaan Budak Hensem Am Penghutang Q Penghutang R Penghutang SkannadhassОценок пока нет

- Taxation - Questions Sepr 2012Документ17 страницTaxation - Questions Sepr 2012kannadhassОценок пока нет

- Max's Audit Rating - Effective April 1, 2016Документ8 страницMax's Audit Rating - Effective April 1, 2016Noel BactonОценок пока нет

- Introduction To Income TaxДокумент36 страницIntroduction To Income TaxDeep ShahОценок пока нет

- Test Series: August, 2018 Mock Test Paper - 1 Final (New) Course: Group - Ii Paper - 7: Direct Tax Laws & International TaxationДокумент6 страницTest Series: August, 2018 Mock Test Paper - 1 Final (New) Course: Group - Ii Paper - 7: Direct Tax Laws & International TaxationRobinxyОценок пока нет

- New Income Tax Calculator For Old & New Tax Regime For Salaried EmployeeДокумент4 страницыNew Income Tax Calculator For Old & New Tax Regime For Salaried EmployeeKiran KumarОценок пока нет

- BWG B Si - 91772 1Документ1 страницаBWG B Si - 91772 1Azaz ShaikhОценок пока нет

- Sample of Contract With Direct Sellers PDFДокумент2 страницыSample of Contract With Direct Sellers PDFPankaj PandeyОценок пока нет

- MicrosoftДокумент2 страницыMicrosoftKrisi MartinezОценок пока нет

- GSTДокумент200 страницGSTyoussefОценок пока нет

- Ministry of Corporate Affairs: Only For Pay Later Payment. Not For Payment at Branch Counter E-Challan For Paying LaterДокумент2 страницыMinistry of Corporate Affairs: Only For Pay Later Payment. Not For Payment at Branch Counter E-Challan For Paying LaterPrakashОценок пока нет

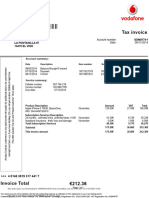

- Spain Vodavone 2 PDFДокумент1 страницаSpain Vodavone 2 PDFNext ServiceОценок пока нет

- HDFC ReportДокумент9 страницHDFC ReportronaktejaniОценок пока нет

- Gmail - Booking Confirmation On IRCTC, Train - 09314, 10-Sep-2021, 2S, LKO - UJNДокумент1 страницаGmail - Booking Confirmation On IRCTC, Train - 09314, 10-Sep-2021, 2S, LKO - UJNSumitОценок пока нет

- GST ChallanДокумент2 страницыGST ChallanATUL NAGORIОценок пока нет

- Document Remitly Western Union SendwaveДокумент5 страницDocument Remitly Western Union SendwaveEvans SolianОценок пока нет

- Petitioners vs. vs. Respondents: en BancДокумент18 страницPetitioners vs. vs. Respondents: en BancPaul EsparagozaОценок пока нет

- Offer Phenom ProX-2252020pdfДокумент4 страницыOffer Phenom ProX-2252020pdfP NAVEEN KUMARОценок пока нет

- 6072 p1 Lembar JawabanДокумент49 страниц6072 p1 Lembar JawabanAhmad Nur Safi'i100% (2)

- Global Remittance:: SGD (Singapore Dollar) Is An Eligible Currency For Wire Transfers.21Документ7 страницGlobal Remittance:: SGD (Singapore Dollar) Is An Eligible Currency For Wire Transfers.21Susmita JakkinapalliОценок пока нет

- Fast Cables LTD: QuotationДокумент1 страницаFast Cables LTD: QuotationAli ShahzadОценок пока нет

- Wa0004.Документ1 страницаWa0004.Reetesh ChandraОценок пока нет

- TC 0040202-20201127Документ1 страницаTC 0040202-20201127DarmawansyahОценок пока нет