Вам также может понравиться

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Ordinary PostДокумент1 страницаOrdinary PostAsim JavedОценок пока нет

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Saif Ullah Khan: ObjectiveДокумент3 страницыSaif Ullah Khan: ObjectiveAsim JavedОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Jpqr9l104xgdt5lvxacedw IV GP PyslpДокумент1 страницаJpqr9l104xgdt5lvxacedw IV GP PyslpAsim JavedОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- ) /"2 B . - '.,r. L (,.fli) T J: - 6otffi""drt"jf"'u'" - ) I "-, N /s-U, GДокумент1 страница) /"2 B . - '.,r. L (,.fli) T J: - 6otffi""drt"jf"'u'" - ) I "-, N /s-U, GAsim JavedОценок пока нет

- Form 1 PDFДокумент1 страницаForm 1 PDFAsim JavedОценок пока нет

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Resume - CA7 SchedulerДокумент5 страницResume - CA7 SchedulerAsim JavedОценок пока нет

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- AS400 Job Scheduler PDFДокумент183 страницыAS400 Job Scheduler PDFAsim JavedОценок пока нет

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- SARFAESI Act in Layman WordsДокумент2 страницыSARFAESI Act in Layman WordsAsim Javed100% (1)

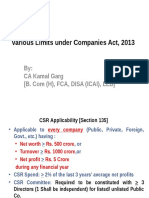

- Various Limits Under Companies Act, 2013 (CA Final)Документ61 страницаVarious Limits Under Companies Act, 2013 (CA Final)Asim JavedОценок пока нет

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Microsoft Word - Practice Paper Advanced Auditing Mock Test November 2016Документ4 страницыMicrosoft Word - Practice Paper Advanced Auditing Mock Test November 2016Asim JavedОценок пока нет

- FEMA Notes Comprehensive Summary For November 2016Документ7 страницFEMA Notes Comprehensive Summary For November 2016Asim JavedОценок пока нет

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Important Company Law Case Laws ListДокумент3 страницыImportant Company Law Case Laws ListAsim JavedОценок пока нет

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Solved International Paint Company Wants To Sell A Large Tract ofДокумент1 страницаSolved International Paint Company Wants To Sell A Large Tract ofAnbu jaromiaОценок пока нет

- BCK Test Paper (40 Marks) Nov 2023 With AnswersДокумент6 страницBCK Test Paper (40 Marks) Nov 2023 With Answersbaidshruti123Оценок пока нет

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- Post Transactions: Account Title Account Code Debit Credit Balance Date Item Ref Debit CreditДокумент5 страницPost Transactions: Account Title Account Code Debit Credit Balance Date Item Ref Debit CreditPaolo IcangОценок пока нет

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- PM Mudra Loan - How To Take Loan PDFДокумент9 страницPM Mudra Loan - How To Take Loan PDFbhramaniОценок пока нет

- Finance Car Leasing Final ProjectДокумент21 страницаFinance Car Leasing Final ProjectShehrozAyazОценок пока нет

- Training Manual Bookkeeping Financial & ManagementДокумент81 страницаTraining Manual Bookkeeping Financial & ManagementJhodie Anne Isorena100% (1)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- RBF Exchane Control BrochureДокумент24 страницыRBF Exchane Control BrochureRavineshОценок пока нет

- 39759Документ3 страницы39759MonikaОценок пока нет

- MANOJSING RAJPUT Affidavit As Per SC ORDERДокумент9 страницMANOJSING RAJPUT Affidavit As Per SC ORDERVarzan BodhanwalaОценок пока нет

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Taxation Situational ProblemsДокумент32 страницыTaxation Situational ProblemsMilo MilkОценок пока нет

- 2022 BIR Form 2316 - 2013650Документ1 страница2022 BIR Form 2316 - 2013650erik skiОценок пока нет

- Corrosion EconomicsДокумент9 страницCorrosion EconomicsEmmanuel EkongОценок пока нет

- Imp S - 4 HANA - New Asset Accounting - Considering Key Aspects - SAP BlogsДокумент39 страницImp S - 4 HANA - New Asset Accounting - Considering Key Aspects - SAP BlogsAnonymous X17EU0lFdОценок пока нет

- HUM-4717 Ch-5 Evaluating A Single Project 2020Документ47 страницHUM-4717 Ch-5 Evaluating A Single Project 2020SadatОценок пока нет

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Suryadev 75 InsuranceДокумент15 страницSuryadev 75 InsuranceKaran ChaudharyОценок пока нет

- EFIN542 U09 T01 PowerPointДокумент26 страницEFIN542 U09 T01 PowerPointcustomsgyanОценок пока нет

- PNB Vs AmoresДокумент3 страницыPNB Vs AmoresLea AndreleiОценок пока нет

- Chanda KochharДокумент39 страницChanda KochharviveknayeeОценок пока нет

- Mergers and AcquisitionДокумент61 страницаMergers and AcquisitionVarsha JaisinghaniОценок пока нет

- State Life Insurance Corporation of PakistanДокумент6 страницState Life Insurance Corporation of PakistanjahanloverОценок пока нет

- Talk About ImbalancesДокумент1 страницаTalk About ImbalancesforbesadminОценок пока нет

- Estate Tax-Handout 2Документ4 страницыEstate Tax-Handout 2Xerez SingsonОценок пока нет

- (Colliers) APAC Cap Rate Report Q4.2022Документ6 страниц(Colliers) APAC Cap Rate Report Q4.2022Khoi NguyenОценок пока нет

- Ibs The Reef, Rawang 1 30/04/23Документ3 страницыIbs The Reef, Rawang 1 30/04/23Suhail amdanОценок пока нет

- midChapterTest 1-1 1-4Документ1 страницаmidChapterTest 1-1 1-4VIPОценок пока нет

- Groww Nifty Total Market Index Fund KIMДокумент37 страницGroww Nifty Total Market Index Fund KIMG1 ROYALОценок пока нет

- Act512 - Assignment Chapter - 06Документ9 страницAct512 - Assignment Chapter - 06Rafin MahmudОценок пока нет

- Accounting For Installment SalesДокумент16 страницAccounting For Installment SalesLeimonadeОценок пока нет

- Advanced Management Accounting PDFДокумент204 страницыAdvanced Management Accounting PDFptgo100% (1)

- Tactical Analysis Strategy and SetupДокумент116 страницTactical Analysis Strategy and SetupAdi Podosu100% (2)