Вам также может понравиться

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Right of Access To Information Act 2017 GazetteДокумент16 страницThe Right of Access To Information Act 2017 GazetteSyed Moazzam AbbasОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Handicrafts in PakistanДокумент18 страницHandicrafts in PakistanSyed Moazzam AbbasОценок пока нет

- The Muqaddimah Volume 1Документ606 страницThe Muqaddimah Volume 1Syed Moazzam Abbas100% (5)

- Processed Food Industry PakistanДокумент6 страницProcessed Food Industry PakistanSyed Moazzam Abbas0% (1)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Phone No. 051-9205075 Ext. 385, 377,236,243,241 & 298Документ4 страницыPhone No. 051-9205075 Ext. 385, 377,236,243,241 & 298Syed Moazzam AbbasОценок пока нет

- S. No Case No. F.4-Particulars of Post(s) Qualifications For Posts Test Specification Topics of Syllabi Part-I Part-II (Bachelor's Level)Документ41 страницаS. No Case No. F.4-Particulars of Post(s) Qualifications For Posts Test Specification Topics of Syllabi Part-I Part-II (Bachelor's Level)Hamid MasoodОценок пока нет

- In The Supreme Court of PakistanДокумент22 страницыIn The Supreme Court of PakistanSyed Moazzam AbbasОценок пока нет

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- FPSC Advt - No - 5-2016Документ8 страницFPSC Advt - No - 5-2016Syed Moazzam AbbasОценок пока нет

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- FPSC Newsletter - 35thДокумент8 страницFPSC Newsletter - 35thSyed Moazzam AbbasОценок пока нет

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Century of English EssaysДокумент247 страницA Century of English EssaysSyed Moazzam AbbasОценок пока нет

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

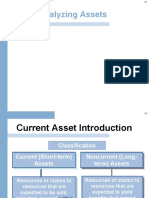

- AssetsДокумент37 страницAssetsSyed Moazzam AbbasОценок пока нет

- Business Plan 22Документ46 страницBusiness Plan 22asmi100% (3)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- 4067 XLS EngДокумент11 страниц4067 XLS EngMILIND SHEKHARОценок пока нет

- Gea Westfalia Separator Group Company Portrait WS 12 10Документ52 страницыGea Westfalia Separator Group Company Portrait WS 12 10ElizavetaYarovaiaОценок пока нет

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Food Safety Programs A Guide To Standard 3.2.1 Food Safety ProgramsДокумент52 страницыFood Safety Programs A Guide To Standard 3.2.1 Food Safety ProgramsmikeОценок пока нет

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- Cost Allocation: Joint-Products & Byproducts: Chapter SixДокумент13 страницCost Allocation: Joint-Products & Byproducts: Chapter SixalemayehuОценок пока нет

- Avelino Et Al - 2019 - Transformative Social InnovationДокумент12 страницAvelino Et Al - 2019 - Transformative Social InnovationJessica PerezОценок пока нет

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Sensory Analysis - Teacher's ManualДокумент88 страницSensory Analysis - Teacher's ManualesjayemОценок пока нет

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Ioan Constant in CVДокумент2 страницыIoan Constant in CVJitariu Ioan CatalinОценок пока нет

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- 6th MAy, 2021Документ4 страницы6th MAy, 2021gohoji4169Оценок пока нет

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- ChaleurRegion-PoirierДокумент88 страницChaleurRegion-PoirierMehdi Bel HajОценок пока нет

- FNB Training Service UpsellingДокумент38 страницFNB Training Service Upsellingmackyamores100% (2)

- Livestock Marketing Performance Evaluation in Afar Region, EthiopiaДокумент9 страницLivestock Marketing Performance Evaluation in Afar Region, EthiopiaPremier PublishersОценок пока нет

- John Uff - Construction Law - 11th Edition 2013 23Документ1 страницаJohn Uff - Construction Law - 11th Edition 2013 23VarunОценок пока нет

- Mindanao Halal Food Corporation: Executive SummaryДокумент3 страницыMindanao Halal Food Corporation: Executive SummaryJossie EjercitoОценок пока нет

- Ch06 PRДокумент11 страницCh06 PRGreigh TenОценок пока нет

- Harvard Business Case: Yum! Brands SolutionДокумент3 страницыHarvard Business Case: Yum! Brands Solutionpolobook3782Оценок пока нет

- Connie Mason - Shadow WalkerДокумент174 страницыConnie Mason - Shadow WalkerFedocea Pearl100% (2)

- ShwapnoДокумент3 страницыShwapnoMahbub TalukderОценок пока нет

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Internal SwotДокумент3 страницыInternal SwotMicah CarpioОценок пока нет

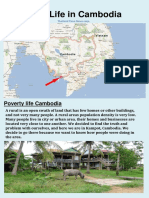

- Cambodia NewspaperДокумент6 страницCambodia Newspaperapi-343706830Оценок пока нет

- Electronica Plastic Machines Limited: Kind Attn: Mr. Dnyaneshwar PhadatareДокумент8 страницElectronica Plastic Machines Limited: Kind Attn: Mr. Dnyaneshwar PhadatareDnyaneshwar Dattatraya PhadatareОценок пока нет

- Business in OmanДокумент16 страницBusiness in OmanVishnu PillaiОценок пока нет

- Written Report About DIДокумент13 страницWritten Report About DIAnne Nicole A CagulangОценок пока нет

- IFAS and EFAS TemplateДокумент3 страницыIFAS and EFAS Templatefirmansyah ramlanОценок пока нет

- Agree or Disangree With The Statement Television Advertising Directed Toward Young Children (Aged Two To Five) Should Not Be AllowedДокумент1 страницаAgree or Disangree With The Statement Television Advertising Directed Toward Young Children (Aged Two To Five) Should Not Be Allowedyoan mellyОценок пока нет

- Amul MarketingДокумент10 страницAmul MarketingvarshabopteОценок пока нет

- Sheet#6 - Matrices and DeterminantsДокумент11 страницSheet#6 - Matrices and DeterminantsMuhammad RakibОценок пока нет

- MM TPДокумент26 страницMM TPmadhumithaОценок пока нет

- FSSC Version 6 Requirements (Foodkida)Документ6 страницFSSC Version 6 Requirements (Foodkida)jacky786Оценок пока нет

- BOONDДокумент45 страницBOONDNitinAgnihotriОценок пока нет