Вам также может понравиться

- 2017 Cognizant Application FormДокумент4 страницы2017 Cognizant Application FormBipin Bansal AgarwalОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Steel June 2017Документ54 страницыSteel June 2017Bipin Bansal AgarwalОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Gyan Capsule 1 - Introduction To ConsultingДокумент7 страницGyan Capsule 1 - Introduction To ConsultingBipin Bansal AgarwalОценок пока нет

- Cloud ComputingДокумент10 страницCloud ComputingBipin Bansal AgarwalОценок пока нет

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Assignment For Activity I - Empathy WalkДокумент5 страницAssignment For Activity I - Empathy WalkBipin Bansal AgarwalОценок пока нет

- Batch Profile: MBA-FT-Class of 2016Документ34 страницыBatch Profile: MBA-FT-Class of 2016Bipin Bansal AgarwalОценок пока нет

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Aggregate PlanningДокумент10 страницAggregate PlanningBipin Bansal AgarwalОценок пока нет

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Iiimaabm Call LetterДокумент1 страницаIiimaabm Call LetterBipin Bansal AgarwalОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Economic Growth: (Continued)Документ13 страницEconomic Growth: (Continued)Bipin Bansal AgarwalОценок пока нет

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- 06Документ7 страниц06Bipin Bansal AgarwalОценок пока нет

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Indian Institute of Management Bangalore Declaration by Parent/GuardianДокумент2 страницыIndian Institute of Management Bangalore Declaration by Parent/GuardianBipin Bansal AgarwalОценок пока нет

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Altisource IIM A JDДокумент2 страницыAltisource IIM A JDBipin Bansal AgarwalОценок пока нет

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Bipin Bansal HR QuestionsДокумент12 страницBipin Bansal HR QuestionsBipin Bansal AgarwalОценок пока нет

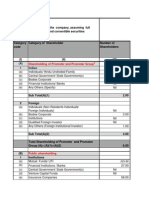

- Shareholding 316 BipinBansalAgarwalДокумент6 страницShareholding 316 BipinBansalAgarwalBipin Bansal AgarwalОценок пока нет

- Brand Loyalty & Competitive Analysis of Pankaj NamkeenДокумент59 страницBrand Loyalty & Competitive Analysis of Pankaj NamkeenBipin Bansal Agarwal100% (1)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- 2 Enron ScamДокумент5 страниц2 Enron ScamBipin Bansal AgarwalОценок пока нет

- BADVAC1X - Quiz 2 Finals: (1 Point)Документ9 страницBADVAC1X - Quiz 2 Finals: (1 Point)Darius DelacruzОценок пока нет

- Strategies Affecting Stock MarketДокумент9 страницStrategies Affecting Stock MarketAditya Kanchan BarasОценок пока нет

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- Vimal Dairy MbaДокумент81 страницаVimal Dairy MbaViral Chaudhari0% (1)

- Group 5 FabmДокумент33 страницыGroup 5 FabmHanissandra Franz V. DalanОценок пока нет

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Basic Concepts and Job Order Cost CycleДокумент15 страницBasic Concepts and Job Order Cost CycleGlaiza Lipana Pingol100% (2)

- CH 17Документ6 страницCH 17Rabie HarounОценок пока нет

- Ias 40 QuestionsДокумент6 страницIas 40 QuestionsFrank AlexanderОценок пока нет

- Warren Sports Supply Worksheet - Amber GarnerДокумент8 страницWarren Sports Supply Worksheet - Amber Garnerapi-456188291100% (1)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- 4A8 DissolutionДокумент20 страниц4A8 DissolutionCarl Dhaniel Garcia SalenОценок пока нет

- Cost Accounting Foundations and EvolutionsДокумент49 страницCost Accounting Foundations and EvolutionsTina LlorcaОценок пока нет

- Notes Adjusting EntriesДокумент14 страницNotes Adjusting EntriesGelesabeth Garcia100% (1)

- Introduction To Consolidated Financial StatementsДокумент6 страницIntroduction To Consolidated Financial StatementsNirali MakwanaОценок пока нет

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Gi I BT TCDN1Документ19 страницGi I BT TCDN1Ly TrươngОценок пока нет

- WAC TemplateДокумент18 страницWAC Templatemian hussainОценок пока нет

- Assignment Accounting Merchendising #2Документ1 страницаAssignment Accounting Merchendising #2NELVA QABLINAОценок пока нет

- Redemption of Preference Shares Format of Balance Sheet Particulars Note No. I Equity & Liabilities 1. Shareholders FundДокумент2 страницыRedemption of Preference Shares Format of Balance Sheet Particulars Note No. I Equity & Liabilities 1. Shareholders FundhanumanthaiahgowdaОценок пока нет

- MKLHB Audited Accounts FYE2012Документ0 страницMKLHB Audited Accounts FYE2012tajuddin8Оценок пока нет

- Class Exercise Session 1,2Документ7 страницClass Exercise Session 1,2sheheryar50% (4)

- Lecture Slides - Chapter 1 2Документ66 страницLecture Slides - Chapter 1 2Van Dat100% (1)

- Module 7Документ5 страницModule 7trixie maeОценок пока нет

- Chapter 05: Absorption Costing and Variable CostingДокумент169 страницChapter 05: Absorption Costing and Variable CostingNgan Tran Ngoc ThuyОценок пока нет

- 2022 Financial StatementsДокумент19 страниц2022 Financial StatementsThe King's UniversityОценок пока нет

- Chapter 4: Financial Planning and Forecasting: Multiple ChoiceДокумент19 страницChapter 4: Financial Planning and Forecasting: Multiple ChoiceFarhanie Nordin100% (1)

- Capital Structure Analysis of Hero HondaДокумент7 страницCapital Structure Analysis of Hero HondaNiklesh ChandakОценок пока нет

- Class No 14 & 15Документ31 страницаClass No 14 & 15WILD๛SHOTッ tanvirОценок пока нет

- Regression Analysis MethodДокумент6 страницRegression Analysis MethodMiccah Jade CastilloОценок пока нет

- EFM4, CH 20, Slides, 07-02-18Документ30 страницEFM4, CH 20, Slides, 07-02-18SyifaОценок пока нет

- Cashflow Projection ChacabriДокумент1 страницаCashflow Projection ChacabriBrian Okuku OwinohОценок пока нет

- SET A ACC 110 - CFE - SY 2023 2024 1st Sem - Answer KeyДокумент19 страницSET A ACC 110 - CFE - SY 2023 2024 1st Sem - Answer KeyJomar RabiaОценок пока нет

- Session-16-17-18-CVP AnalysisДокумент78 страницSession-16-17-18-CVP Analysis020Abhisek KhadangaОценок пока нет