Вам также может понравиться

- Superior Grammar School Project CharterДокумент2 страницыSuperior Grammar School Project CharterSehab SubhОценок пока нет

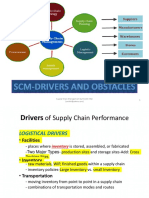

- SCM Fall 17 - 2 - Drivers and Obstacles-UpdatedДокумент15 страницSCM Fall 17 - 2 - Drivers and Obstacles-UpdatedMYawarMОценок пока нет

- Research Proposal and Report by Dr. Krisna MurtiДокумент87 страницResearch Proposal and Report by Dr. Krisna MurtiNovia WinardiОценок пока нет

- Soal Quiz AntrianДокумент1 страницаSoal Quiz AntrianDhaniya Tri WigatiОценок пока нет

- ABET Definition of EngineeringДокумент3 страницыABET Definition of EngineeringJose BarnabasОценок пока нет

- Practice ProblemsДокумент2 страницыPractice ProblemsIshak Firdauzi RuslanОценок пока нет

- Assessing Incentive-Based Motivation On The Team Productivity by An Agent-Based ModelДокумент5 страницAssessing Incentive-Based Motivation On The Team Productivity by An Agent-Based ModelInternational Journal of Innovative Science and Research TechnologyОценок пока нет

- INVENTORY PLANNINGДокумент7 страницINVENTORY PLANNINGandov9Оценок пока нет

- Chapter 15 Homework Due on September 5Документ5 страницChapter 15 Homework Due on September 5Pornpunsa WuttisanwattanaОценок пока нет

- Faktor-Faktor Yang Mempengaruhi Organizational: Citizenship Behavior (Ocb)Документ5 страницFaktor-Faktor Yang Mempengaruhi Organizational: Citizenship Behavior (Ocb)Sari Bionic SevenОценок пока нет

- LGC holiday chocolate box production and packaging optionsДокумент6 страницLGC holiday chocolate box production and packaging optionsSalman KhanОценок пока нет

- Pengaruh E-Service Quality Terhadap Perceived Value Dan E - (Survei Pada Pelanggan Go-Ride Yang Menggunakan Mobile Application Go-Jek Di Kota Malang)Документ10 страницPengaruh E-Service Quality Terhadap Perceived Value Dan E - (Survei Pada Pelanggan Go-Ride Yang Menggunakan Mobile Application Go-Jek Di Kota Malang)m.knoeri habibОценок пока нет

- LOMCДокумент3 страницыLOMCLINDA CAMELIAОценок пока нет

- Factors Influencing Online Shopping Motives on Kaskus Semarang CommunityДокумент32 страницыFactors Influencing Online Shopping Motives on Kaskus Semarang CommunityMillati AgisnaОценок пока нет

- Jurnal Makro ErgonomiДокумент8 страницJurnal Makro ErgonomiWidhani Putri100% (1)

- Chapter 1 The Manager and Management AccountingДокумент20 страницChapter 1 The Manager and Management AccountingRose McMahon0% (1)

- SCM Chapter 6Документ17 страницSCM Chapter 6Dito Eri BasyasyaОценок пока нет

- Application QuestionsДокумент3 страницыApplication QuestionsJonela LazaroОценок пока нет

- Analisis Kinerja Sistem Antrian PDFДокумент9 страницAnalisis Kinerja Sistem Antrian PDFAdam NugrahaОценок пока нет

- Perencanaan & Pengendalian ProduksiДокумент25 страницPerencanaan & Pengendalian ProduksiThesa Trinita HОценок пока нет

- Modular Layout Disertasi PDFДокумент169 страницModular Layout Disertasi PDFChristopher LeeОценок пока нет

- Hambatan Dan Dorongan Supply Chain ManagementДокумент4 страницыHambatan Dan Dorongan Supply Chain ManagementesiОценок пока нет

- Engineering Project Failures: Lessons from Titanic, Denver Airport, Berlin Airport & Airbus A380Документ2 страницыEngineering Project Failures: Lessons from Titanic, Denver Airport, Berlin Airport & Airbus A380krishna chaitanya0% (1)

- Risk Management AssignmentДокумент7 страницRisk Management AssignmentLahiru DabareОценок пока нет

- MRP Material Requirements PlanningДокумент36 страницMRP Material Requirements PlanningorbansaОценок пока нет

- An Analysis of Dematel Approaches For CriteriaДокумент21 страницаAn Analysis of Dematel Approaches For CriteriaLeonel Gonçalves DuqueОценок пока нет

- MCDM IntroductionДокумент23 страницыMCDM IntroductionWandhansari Sekar JatiningrumОценок пока нет

- Pengaruh Pemberian Tambahan Penghasilan Pegawai (TPP) Terhadap Kinerja Pegawai Di Dinas Pendidikan Dan Kebudayaan Kabupaten JenepontoДокумент146 страницPengaruh Pemberian Tambahan Penghasilan Pegawai (TPP) Terhadap Kinerja Pegawai Di Dinas Pendidikan Dan Kebudayaan Kabupaten JenepontoHengky SaputraОценок пока нет

- Kasus Sia Pert10 Siklus ProduksiДокумент100 страницKasus Sia Pert10 Siklus ProduksiAlda ArtantiОценок пока нет

- Perancangan Pengembangan Produk Powerbank Dengan Metode Quality Function Deployment (QFD)Документ13 страницPerancangan Pengembangan Produk Powerbank Dengan Metode Quality Function Deployment (QFD)TM AMarcellinus Tedy100% (1)

- Suply Chain ManagementДокумент10 страницSuply Chain Managementmuhammad rohmanОценок пока нет

- System Integrated Logistics Support (SILS) Policy Manual: COMDTINST M4105.8Документ71 страницаSystem Integrated Logistics Support (SILS) Policy Manual: COMDTINST M4105.8Nicolai TamataevОценок пока нет

- Manajemen Operasional dan Transformasi ProduksiДокумент19 страницManajemen Operasional dan Transformasi ProduksiFitriYaniОценок пока нет

- The Implementation of Quality Function Deployment (QFD) in Increasing Customer Satisfaction in PT PLN (Persero) Unit Induk Distribusi (UID) Jakarta Raya UP3 MentengДокумент11 страницThe Implementation of Quality Function Deployment (QFD) in Increasing Customer Satisfaction in PT PLN (Persero) Unit Induk Distribusi (UID) Jakarta Raya UP3 MentengInternational Journal of Innovative Science and Research TechnologyОценок пока нет

- Analisis Clustering Dokumen Tugas Akhir Mahasiswa Sistem Informasi Universitas Nasional Menggunakan Metode K-Means ClusteringДокумент7 страницAnalisis Clustering Dokumen Tugas Akhir Mahasiswa Sistem Informasi Universitas Nasional Menggunakan Metode K-Means ClusteringJurnal JTIK (Jurnal Teknologi Informasi dan Komunikasi)Оценок пока нет

- 7 Concept Generation New. Pengembangan Produk. Teknik IndustriДокумент55 страниц7 Concept Generation New. Pengembangan Produk. Teknik IndustriAisah Dirawidya0% (1)

- 7a. B2B Buying BehaviorДокумент19 страниц7a. B2B Buying BehaviorMirza Sher Afgan BabarОценок пока нет

- Line Balancing - Teknik Management Industri UPIДокумент43 страницыLine Balancing - Teknik Management Industri UPIUsepОценок пока нет

- Case Study On Application of ABC Analysis in Inventory ManagementДокумент5 страницCase Study On Application of ABC Analysis in Inventory ManagementIMSsecC Pgdm21-23officialОценок пока нет

- HiДокумент7 страницHisachinsaklani23Оценок пока нет

- Project Management Group Work 8: The Bathtub PeriodДокумент3 страницыProject Management Group Work 8: The Bathtub Periodpalak mohodОценок пока нет

- A Division Is Used To Represent The Way in Which Goods and Services Are Distributed To CustomersДокумент33 страницыA Division Is Used To Represent The Way in Which Goods and Services Are Distributed To Customerssmiti84Оценок пока нет

- Analisis Implementasi Sistem Just in Time (Jit) Pada Persediaan Bahan Baku Untuk Memenuhi Kebutuhan Produksi (Документ8 страницAnalisis Implementasi Sistem Just in Time (Jit) Pada Persediaan Bahan Baku Untuk Memenuhi Kebutuhan Produksi (Feby Hariska100% (1)

- ACCT 557 Final ExamДокумент18 страницACCT 557 Final Examlynnturner123Оценок пока нет

- Managerial Accounting and Cost ConceptsДокумент85 страницManagerial Accounting and Cost ConceptsCatherine DelRayОценок пока нет

- Operations Management 1Документ67 страницOperations Management 1apoorvbabel0% (1)

- ME477 Machining Operations and Product DesignДокумент3 страницыME477 Machining Operations and Product Designاحمد عمر حديدОценок пока нет

- An Approach For Condition Monitoring of Rolling Stock Sub-SystemsДокумент12 страницAn Approach For Condition Monitoring of Rolling Stock Sub-SystemsDamigo DiegoОценок пока нет

- Positioning MapsДокумент5 страницPositioning MapsthuanvltkОценок пока нет

- Structure of Report 12th August 2020Документ4 страницыStructure of Report 12th August 2020Eka Puspa Krisna MurtiОценок пока нет

- Transportation and Supply Chain ManagementДокумент25 страницTransportation and Supply Chain ManagementMedika SihombingОценок пока нет

- AGV Problems: Calculating Vehicle RequirementsДокумент1 страницаAGV Problems: Calculating Vehicle RequirementsLương Bảo HânОценок пока нет

- Critical Factors in Managing TechnologyДокумент15 страницCritical Factors in Managing TechnologyMekh Raj JaishiОценок пока нет

- Order Winners N Order QualifiersДокумент4 страницыOrder Winners N Order QualifiersMeet SampatОценок пока нет

- Yash Sampat Literature Review AcountsДокумент4 страницыYash Sampat Literature Review AcountsYash SampatОценок пока нет

- Business Intelligence Unit 2 Chapter 1Документ7 страницBusiness Intelligence Unit 2 Chapter 1vivek100% (1)

- A Study On Inventory ManagementДокумент22 страницыA Study On Inventory ManagementMehul Panchal100% (1)

- MEANING AND TYPES OF INVENTORYДокумент49 страницMEANING AND TYPES OF INVENTORYTeena ChawlaОценок пока нет

- Stores 1Документ12 страницStores 1James BoruОценок пока нет

- Inventory and Warehousing ManagementДокумент10 страницInventory and Warehousing Managementshabeena shahОценок пока нет

- Sources of New Ideas For Entrepreneurs: Are Keen To Encourage CreativityДокумент13 страницSources of New Ideas For Entrepreneurs: Are Keen To Encourage CreativityAarthy ChandranОценок пока нет

- Report Emp EngagementДокумент56 страницReport Emp EngagementAarthy ChandranОценок пока нет

- Entrepreneurshipandinnovation 091206034558 Phpapp02Документ20 страницEntrepreneurshipandinnovation 091206034558 Phpapp02Sushil ChaurasiyaОценок пока нет

- Dairy IndustryДокумент95 страницDairy IndustryAarthy ChandranОценок пока нет

- ADW 622 - Management Project - Khor Eng TattДокумент34 страницыADW 622 - Management Project - Khor Eng TattMomin Tariq100% (1)

- IPR PowerpointДокумент14 страницIPR PowerpointAarthy ChandranОценок пока нет

- The Consumer Perception of Design - Case SДокумент29 страницThe Consumer Perception of Design - Case SAarthy Chandran100% (1)

- 08 Chapter 3Документ52 страницы08 Chapter 3Aarthy ChandranОценок пока нет

- Smart Alex's TasksДокумент1 страницаSmart Alex's TasksAarthy ChandranОценок пока нет

- Regression - TaskДокумент1 страницаRegression - TaskAarthy ChandranОценок пока нет

- Percentage On SPSS ExamДокумент6 страницPercentage On SPSS ExamAarthy ChandranОценок пока нет

- Percentage On SPSS ExamДокумент6 страницPercentage On SPSS ExamAarthy ChandranОценок пока нет

- Percentage On SPSS ExamДокумент6 страницPercentage On SPSS ExamAarthy ChandranОценок пока нет

- Project Report On Financial Statement Analysis of Kajaria Ceramics Ltd.Документ121 страницаProject Report On Financial Statement Analysis of Kajaria Ceramics Ltd.Syed Mohd Ziya86% (83)

- Sciencedirect: Multicriteria Inventory Abc Classification in An Automobile Rubber Components Manufacturing IndustryДокумент6 страницSciencedirect: Multicriteria Inventory Abc Classification in An Automobile Rubber Components Manufacturing IndustryAarthy ChandranОценок пока нет

- 1 s2.0 S2212827116309155 MainДокумент6 страниц1 s2.0 S2212827116309155 MainAarthy ChandranОценок пока нет

- Final Glossary For Strategic ManagementДокумент11 страницFinal Glossary For Strategic ManagementAarthy ChandranОценок пока нет

- 1 s2.0 S0959652616304395 MainДокумент15 страниц1 s2.0 S0959652616304395 MainAarthy ChandranОценок пока нет

- Development of Kanban System at Local Manufacturing Company in Malaysia - Case StudyДокумент6 страницDevelopment of Kanban System at Local Manufacturing Company in Malaysia - Case StudyAarthy ChandranОценок пока нет

- HP Case RevisedДокумент6 страницHP Case RevisedKenneth ChuaОценок пока нет

- Project Term ReportДокумент29 страницProject Term ReportM Hammad KothariОценок пока нет

- ALKO Case Final ReportДокумент7 страницALKO Case Final ReportSamarth Jain100% (1)

- Management Accounting: Student EditionДокумент26 страницManagement Accounting: Student Editionannisah nsa20Оценок пока нет

- Inventory Management's Impact on Organizational PerformanceДокумент68 страницInventory Management's Impact on Organizational PerformanceJoseph Mburu80% (5)

- Safety StockДокумент6 страницSafety Stockkumar325Оценок пока нет

- Interrobang Case Study ProposalДокумент11 страницInterrobang Case Study ProposalKapil VermaОценок пока нет

- Sap Erp 6.0: Rajesh SharmaДокумент42 страницыSap Erp 6.0: Rajesh SharmadineshОценок пока нет

- Risk Pool GameДокумент5 страницRisk Pool GameTú TúОценок пока нет

- Addisalem Assefa PDFДокумент54 страницыAddisalem Assefa PDFKefi BelayОценок пока нет

- Economic Order QuantityДокумент6 страницEconomic Order QuantityJelay QuilatanОценок пока нет

- Inventory Management Techniques & CostsДокумент5 страницInventory Management Techniques & CostsAngela Shaine Castro GarciaОценок пока нет

- SparcoДокумент3 страницыSparcoAli HaiderОценок пока нет

- Inventory ManagementДокумент12 страницInventory ManagementJoshua CabinasОценок пока нет

- 72 Inventory Management and Financial PeДокумент22 страницы72 Inventory Management and Financial PeKiersteen AnasОценок пока нет

- SecA Group01 PlazaДокумент8 страницSecA Group01 PlazaAvinash Topno100% (1)

- Pdfcoffee.com Technical English Vocabulary and Grammar Alison Pohl Nick Brieger 2002 PDF FreeДокумент148 страницPdfcoffee.com Technical English Vocabulary and Grammar Alison Pohl Nick Brieger 2002 PDF FreeDima IlyinОценок пока нет

- Module IiДокумент12 страницModule IiArlan Joseph LopezОценок пока нет

- Logistics 1Документ36 страницLogistics 1Quỳnh Nguyễn NhưОценок пока нет

- Six Sigma Approach For Replenishment in Supply ChainДокумент52 страницыSix Sigma Approach For Replenishment in Supply ChainAbhishek KumarОценок пока нет

- TSU-CBA Working Capital ManagementДокумент7 страницTSU-CBA Working Capital Managementangelika dijamcoОценок пока нет

- Chapter 2 Study Questions Solution ManualДокумент12 страницChapter 2 Study Questions Solution ManualSebastiàn Valle100% (3)

- Material Master Hierarchy: Configuration Steps For Defining Output Format of Material NumberДокумент36 страницMaterial Master Hierarchy: Configuration Steps For Defining Output Format of Material NumberSambit Mohanty100% (1)

- Group 9 - Section E - HPДокумент12 страницGroup 9 - Section E - HPShubham ShuklaОценок пока нет

- Inventory Control and Management 2 PDF FreeДокумент61 страницаInventory Control and Management 2 PDF FreePenelope Delos SantosОценок пока нет

- Master Schedule and RCCP Course - Very Awesome PDFДокумент176 страницMaster Schedule and RCCP Course - Very Awesome PDFeternal_rhymes6972100% (1)

- Hi Mix Low VolumeДокумент20 страницHi Mix Low VolumeKC KiewОценок пока нет

- Kontus Eleonora PDFДокумент12 страницKontus Eleonora PDFHarjot SinghОценок пока нет

- Data Hackathon: Bc3406 Business Analytics ConsultingДокумент175 страницData Hackathon: Bc3406 Business Analytics ConsultingjohnconnorОценок пока нет

- Chapter 4 - Single Item - Probabilistic DemandДокумент96 страницChapter 4 - Single Item - Probabilistic DemandKhánh Đoan Lê ĐìnhОценок пока нет