Вам также может понравиться

- FMP Assignement Key - Cases Fall 10Документ16 страницFMP Assignement Key - Cases Fall 10ahsan_anwar_1Оценок пока нет

- Mercury Athletic Footwear Case SolutionДокумент3 страницыMercury Athletic Footwear Case SolutionDI WU100% (2)

- Mercuryathleticfootwera Case AnalysisДокумент8 страницMercuryathleticfootwera Case AnalysisNATOEEОценок пока нет

- Mercury Athletic (Student Templates) FinalДокумент6 страницMercury Athletic (Student Templates) FinalGarland GayОценок пока нет

- Airthread SolutionДокумент30 страницAirthread SolutionSrikanth VasantadaОценок пока нет

- Online AnswerДокумент4 страницыOnline AnswerYiru Pan100% (2)

- Mercury Athletic Historical Income StatementsДокумент18 страницMercury Athletic Historical Income StatementskarthikawarrierОценок пока нет

- HBS Mercury CaseДокумент4 страницыHBS Mercury CaseDavid Petru100% (1)

- Ameritrade Case SolutionДокумент34 страницыAmeritrade Case SolutionAbhishek GargОценок пока нет

- CASE Exhibits - HertzДокумент15 страницCASE Exhibits - HertzSeemaОценок пока нет

- Michael McClintock Case1Документ2 страницыMichael McClintock Case1Mike MCОценок пока нет

- Mercury Athletic FootwearДокумент9 страницMercury Athletic Footwearandy117950% (2)

- Hola Kola CaseДокумент4 страницыHola Kola CaseSwaraj Dhar25% (4)

- Mercury Athletic Footwear Case (Work Sheet)Документ16 страницMercury Athletic Footwear Case (Work Sheet)Bharat KoiralaОценок пока нет

- Mercury CaseДокумент23 страницыMercury Caseuygh gОценок пока нет

- Mercury Athletic QuestionsДокумент1 страницаMercury Athletic QuestionsRazi UllahОценок пока нет

- MercuryДокумент5 страницMercuryமுத்துக்குமார் செОценок пока нет

- Ib Case MercuryДокумент9 страницIb Case MercuryGovind Saboo100% (2)

- Airthread Acquisition Operating AssumptionsДокумент27 страницAirthread Acquisition Operating AssumptionsnidhidОценок пока нет

- Mercury Athletic CaseДокумент3 страницыMercury Athletic Casekrishnakumar rОценок пока нет

- Mercury Athletic FootwearДокумент4 страницыMercury Athletic FootwearAbhishek KumarОценок пока нет

- Assumptions: Comparable Companies:Market ValueДокумент18 страницAssumptions: Comparable Companies:Market ValueTanya YadavОценок пока нет

- Strategic ManagementДокумент9 страницStrategic ManagementdiddiОценок пока нет

- AirThread Class 2020Документ21 страницаAirThread Class 2020Son NguyenОценок пока нет

- Mercury Athletic Case SectionBДокумент15 страницMercury Athletic Case SectionBVinith VemanaОценок пока нет

- Valuation of Airthread April 2012Документ26 страницValuation of Airthread April 2012Perumalla Pradeep KumarОценок пока нет

- New Heritage DoolДокумент9 страницNew Heritage DoolVidya Sagar KonaОценок пока нет

- MW SolutionДокумент19 страницMW SolutionDhiren GalaОценок пока нет

- Fin 321 Case PresentationДокумент19 страницFin 321 Case PresentationJose ValdiviaОценок пока нет

- Mercury QuestionsДокумент6 страницMercury Questionsapi-239586293Оценок пока нет

- WrigleyДокумент28 страницWrigleyKaran Rana100% (1)

- Airthread Valuation Group#2Документ24 страницыAirthread Valuation Group#2Himanshu AgrawalОценок пока нет

- Pacific Grove Spice Company CalculationsДокумент12 страницPacific Grove Spice Company CalculationsJuan Jose Acero CaballeroОценок пока нет

- Midland Energy SolutionДокумент3 страницыMidland Energy SolutionAditya BansalОценок пока нет

- DC 51: Busi 640 Case 3: Valuation of Airthread ConnectionsДокумент4 страницыDC 51: Busi 640 Case 3: Valuation of Airthread ConnectionsTunzala ImanovaОценок пока нет

- Tire City AssignmentДокумент6 страницTire City AssignmentXRiloXОценок пока нет

- HP Case Competition PresentationДокумент17 страницHP Case Competition PresentationNatalia HernandezОценок пока нет

- Sampa Video Case ExhibitsДокумент1 страницаSampa Video Case ExhibitsOnal RautОценок пока нет

- Sampa Video: Project ValuationДокумент18 страницSampa Video: Project Valuationkrissh_87Оценок пока нет

- BurtonsДокумент6 страницBurtonsKritika GoelОценок пока нет

- Investment Analysis Polar Sports AДокумент9 страницInvestment Analysis Polar Sports AtalabreОценок пока нет

- Sampa Video Case SolutionДокумент6 страницSampa Video Case SolutionRahul SinhaОценок пока нет

- Mercury Athletic FootwearДокумент9 страницMercury Athletic FootwearJon BoОценок пока нет

- Sterling Student ManikДокумент23 страницыSterling Student ManikManik BajajОценок пока нет

- Mercury Athletic Footwear - Valuing The Opportunity: FINS 3625 - Case Study Written ComponentДокумент9 страницMercury Athletic Footwear - Valuing The Opportunity: FINS 3625 - Case Study Written ComponentBharat KoiralaОценок пока нет

- OceanCarriers KenДокумент24 страницыOceanCarriers KensaaaruuuОценок пока нет

- Polar Sports X Ls StudentДокумент9 страницPolar Sports X Ls StudentBilal Ahmed Shaikh0% (1)

- Group19 Mercury AthleticДокумент11 страницGroup19 Mercury AthleticpmcsicОценок пока нет

- Burton SensorsДокумент2 страницыBurton SensorsSankalp MishraОценок пока нет

- Valuation of Airthread Connections Questions TraductionДокумент2 страницыValuation of Airthread Connections Questions TraductionNatalia HernandezОценок пока нет

- AirThread G015Документ6 страницAirThread G015Kunal MaheshwariОценок пока нет

- Income Statement: Actual Estimated Projected Fiscal 2008 Projection Notes RevenueДокумент10 страницIncome Statement: Actual Estimated Projected Fiscal 2008 Projection Notes RevenueAleksandar ZvorinjiОценок пока нет

- Airline AnalysisДокумент20 страницAirline Analysisapi-314693711Оценок пока нет

- Income Statement For StartupsДокумент3 страницыIncome Statement For StartupsBiki BhaiОценок пока нет

- Financial ReportДокумент135 страницFinancial ReportleeeeОценок пока нет

- Financial ReportДокумент135 страницFinancial ReportleeeeОценок пока нет

- 1Документ617 страниц1Nelz CayabyabОценок пока нет

- Parent, Inc Actual Financial Statements For 2012 and OlsenДокумент23 страницыParent, Inc Actual Financial Statements For 2012 and OlsenManal ElkhoshkhanyОценок пока нет

- Cover Sheet: General InputsДокумент10 страницCover Sheet: General InputsBobby ChristiantoОценок пока нет

- Growth Rates (%) % To Net Sales % To Net SalesДокумент21 страницаGrowth Rates (%) % To Net Sales % To Net Salesavinashtiwari201745Оценок пока нет

- Gemini Electronics Template and Raw DataДокумент9 страницGemini Electronics Template and Raw Datapierre balentineОценок пока нет

- BNI 111709 v2Документ2 страницыBNI 111709 v2fcfroicОценок пока нет

- Credit Risk ModellingДокумент40 страницCredit Risk ModellingSwaraj Dhar100% (2)

- 3SCM Lecture3S PDFДокумент15 страниц3SCM Lecture3S PDFSwaraj DharОценок пока нет

- Pipe Dimensions - CS - SS - HDPE100 - HDPE80Документ16 страницPipe Dimensions - CS - SS - HDPE100 - HDPE80Swaraj DharОценок пока нет

- Derivative OIДокумент255 страницDerivative OISwaraj DharОценок пока нет

- Cooper Spreadsheet SolutionДокумент23 страницыCooper Spreadsheet SolutionSwaraj DharОценок пока нет

- Power SectorДокумент56 страницPower SectorSwaraj DharОценок пока нет

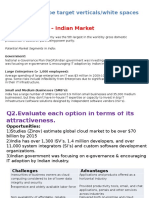

- Q1.What Could Be Target Verticals/white Spaces Options?Документ2 страницыQ1.What Could Be Target Verticals/white Spaces Options?Swaraj DharОценок пока нет

- How Can Analytics and Data Science Leverage Machine Learning in Future - Swaraj - MDIДокумент7 страницHow Can Analytics and Data Science Leverage Machine Learning in Future - Swaraj - MDISwaraj DharОценок пока нет

- Group 8 Section B Submitted To: Dr. Anand K Sharma: Professor - Marketing, Mdi, GurgaonДокумент9 страницGroup 8 Section B Submitted To: Dr. Anand K Sharma: Professor - Marketing, Mdi, GurgaonSwaraj DharОценок пока нет

- Case Study On Natureview Farm: Group 10 Section B Submitted To: Prof. Vibhava SrivastavaДокумент19 страницCase Study On Natureview Farm: Group 10 Section B Submitted To: Prof. Vibhava SrivastavaSwaraj DharОценок пока нет

- Group4 SectionA SampavideoДокумент5 страницGroup4 SectionA Sampavideokarthikmaddula007_66Оценок пока нет

- Capital Structure Decisions: Assignment - 1Документ18 страницCapital Structure Decisions: Assignment - 1khan mandyaОценок пока нет

- Financing Decisions 10-12Документ48 страницFinancing Decisions 10-12Rajat ShrinetОценок пока нет

- Cost of CapitalДокумент114 страницCost of CapitalNamra ImranОценок пока нет

- CapstructДокумент17 страницCapstructPushpraj Singh BaghelОценок пока нет

- Financial Management - 2 Marks Questions and AnswersДокумент2 страницыFinancial Management - 2 Marks Questions and AnswersKumara Kannan Rengasamy100% (4)

- Chap 14Документ59 страницChap 14DEVYANI WANKHEDEОценок пока нет

- Assessment Case Paper Analysis / Tutorialoutlet Dot ComДокумент37 страницAssessment Case Paper Analysis / Tutorialoutlet Dot Comjorge0048Оценок пока нет

- Financial ParametersДокумент43 страницыFinancial ParametersJivaansha SinhaОценок пока нет

- Concept Questions: Chapter Twelve The Analysis of Growth and Sustainable EarningsДокумент64 страницыConcept Questions: Chapter Twelve The Analysis of Growth and Sustainable EarningsceojiОценок пока нет

- Worksheet in FMChap4Документ3 страницыWorksheet in FMChap4Nguyên ThảoОценок пока нет

- Chap 14 SolutionsДокумент10 страницChap 14 SolutionsMiftahudin Miftahudin100% (1)

- CA Inter FMEF Suggested Answers For May 2019Документ19 страницCA Inter FMEF Suggested Answers For May 2019Sayyamee BedmuthaОценок пока нет

- Huaneng Power IntlДокумент30 страницHuaneng Power Intlshovon mukit0% (1)

- Chapter 2Документ90 страницChapter 2Sky walkingОценок пока нет

- Paper H.V. (Honours) Corporate Accounting & Reporting MODULE I - 50 MarksДокумент12 страницPaper H.V. (Honours) Corporate Accounting & Reporting MODULE I - 50 MarkssangkitaОценок пока нет

- Investments Quiz 3-Key-1Документ6 страницInvestments Quiz 3-Key-1Hashaam JavedОценок пока нет

- International Financial Management 13 Edition: by Jeff MaduraДокумент36 страницInternational Financial Management 13 Edition: by Jeff MaduraJaime SerranoОценок пока нет

- Capital Structure DecisionДокумент18 страницCapital Structure DecisionFALAK OBERAIОценок пока нет

- Session 18 Risk Return Portfolio BetaДокумент157 страницSession 18 Risk Return Portfolio BetahimanshОценок пока нет

- Chapter 7Документ22 страницыChapter 7Celestine MoonОценок пока нет

- Acc501 Final Term Current Solved Paper 2011Документ6 страницAcc501 Final Term Current Solved Paper 2011Ab DulОценок пока нет

- Monno Ceramic ValuationДокумент47 страницMonno Ceramic ValuationMahmudul HassanОценок пока нет

- Sanjay Saraf SFM Volume 3 Equity and BondДокумент251 страницаSanjay Saraf SFM Volume 3 Equity and BondShubham AgrawalОценок пока нет

- Investment Analysis & Portfolio Management: Equity ValuationДокумент5 страницInvestment Analysis & Portfolio Management: Equity ValuationNitesh Kirar100% (1)

- Jun18l1equ-C03 QaДокумент7 страницJun18l1equ-C03 Qarafav10Оценок пока нет

- LAS Applied Econ Q4 Week 1-4Документ92 страницыLAS Applied Econ Q4 Week 1-4Luis Dominic A. CrisostomoОценок пока нет

- Part I. Multiple Choice Questions: Select The Best Statement or Words That Corresponds To The QuestionДокумент8 страницPart I. Multiple Choice Questions: Select The Best Statement or Words That Corresponds To The QuestionNhel AlvaroОценок пока нет

- Corporate Finance Present ValueДокумент37 страницCorporate Finance Present ValueTalib DoaОценок пока нет