Вам также может понравиться

- asset-v1-IMF+FMAx+1T2017+type@asset+block@FMAx M1 CLEAN NewДокумент42 страницыasset-v1-IMF+FMAx+1T2017+type@asset+block@FMAx M1 CLEAN NewBURUNDI1Оценок пока нет

- Home Day Trading Technical Analysis Stocks Options Bonds Personal Finance Free Offers Scottrade: $7 Online Stock TradesДокумент11 страницHome Day Trading Technical Analysis Stocks Options Bonds Personal Finance Free Offers Scottrade: $7 Online Stock Tradesganesh061Оценок пока нет

- Lecture 5 InterestRateFutures (Part1)Документ36 страницLecture 5 InterestRateFutures (Part1)efflux 1990Оценок пока нет

- On The Purchase of 91-Day T-Bill, If The Face Value Is $3,000 and Purchase Price Is $2,900. (1QP)Документ8 страницOn The Purchase of 91-Day T-Bill, If The Face Value Is $3,000 and Purchase Price Is $2,900. (1QP)I IvaОценок пока нет

- Photographic LaboratoriesДокумент5 страницPhotographic LaboratoriesJosann WelchОценок пока нет

- How Bond Prices Are DeterminedДокумент5 страницHow Bond Prices Are DeterminedjujonetОценок пока нет

- Exchange Rate DeterminationДокумент14 страницExchange Rate DeterminationSaurabh BihaniОценок пока нет

- FNCE 30001 Investments: Fixed Income FundamentalsДокумент70 страницFNCE 30001 Investments: Fixed Income FundamentalsVrtpy CiurbanОценок пока нет

- Financial Markets: Dr. Katherine Sauer A Citizen's Guide To Economics ECO 1040Документ36 страницFinancial Markets: Dr. Katherine Sauer A Citizen's Guide To Economics ECO 1040Katherine SauerОценок пока нет

- International Bond Market ParticipantsДокумент6 страницInternational Bond Market ParticipantsNandini JaganОценок пока нет

- Techniques of Asset/liability Management: Futures, Options, and SwapsДокумент19 страницTechniques of Asset/liability Management: Futures, Options, and SwapsNishant Verma100% (1)

- Bond ValuationДокумент10 страницBond ValuationVivek SuranaОценок пока нет

- Money Mrkts 2ndДокумент3 страницыMoney Mrkts 2ndygolcuОценок пока нет

- 5.fin17 Derivatives9 - 10 Done AskДокумент33 страницы5.fin17 Derivatives9 - 10 Done AskPratik GuptaОценок пока нет

- Topic 6Документ82 страницыTopic 6Narcisse ChanОценок пока нет

- Bonds - Chapt. 8 in RWJJДокумент10 страницBonds - Chapt. 8 in RWJJHaris FadzanОценок пока нет

- Asset Prices and Interest Rates: Notes To The InstructorДокумент26 страницAsset Prices and Interest Rates: Notes To The InstructorRahul ChaturvediОценок пока нет

- Valuation of Bonds and SharesДокумент30 страницValuation of Bonds and SharesJohn TomОценок пока нет

- Bond Cash Flows and YieldsДокумент14 страницBond Cash Flows and YieldsPham Minh DucОценок пока нет

- Power Notes: Bonds Payable and Investments in BondsДокумент38 страницPower Notes: Bonds Payable and Investments in BondsiVOОценок пока нет

- Cash Flow InvestmentsДокумент17 страницCash Flow Investmentskuky6549369Оценок пока нет

- BU SM323 Midterm+ReviewДокумент23 страницыBU SM323 Midterm+ReviewrockstarliveОценок пока нет

- Midterm Exam 1 Practice - SolutionДокумент6 страницMidterm Exam 1 Practice - SolutionbobtanlaОценок пока нет

- Assignment 1stДокумент3 страницыAssignment 1stAmmar ButtОценок пока нет

- PS7 Primera ParteДокумент5 страницPS7 Primera PartethomasОценок пока нет

- Chapter 6Документ57 страницChapter 6Can BayirОценок пока нет

- Case Study BondsДокумент5 страницCase Study BondsAbhijeit BhosaleОценок пока нет

- Iapm Iim Jammu #3Документ67 страницIapm Iim Jammu #3Daksh KhullarОценок пока нет

- Bond Market Fundamentals Dec2012Документ36 страницBond Market Fundamentals Dec2012caxap100% (3)

- Valuing Stocks Using the Dividend Discount Model (DDMДокумент14 страницValuing Stocks Using the Dividend Discount Model (DDMNick HaldenОценок пока нет

- Mock Exam - Section AДокумент4 страницыMock Exam - Section AHAHAHAОценок пока нет

- End of Chapter Exercises - AnswersДокумент3 страницыEnd of Chapter Exercises - AnswersYvonneОценок пока нет

- PEP - MTM ExplainedДокумент4 страницыPEP - MTM Explainedabhishekray20Оценок пока нет

- Kelly criterion for stock market investingДокумент42 страницыKelly criterion for stock market investingBogdan L Morosan100% (1)

- CA FINAL SFM AMENDMENT SHEET Nov 2021 BY CA GAURAV JAINДокумент13 страницCA FINAL SFM AMENDMENT SHEET Nov 2021 BY CA GAURAV JAINType BlankОценок пока нет

- Interest Rates, Bond Valuation, and Stock ValuationДокумент57 страницInterest Rates, Bond Valuation, and Stock Valuationnandita3693Оценок пока нет

- Refinancing Risk: Solutions For End-of-Chapter Questions and Problems: Chapter SevenДокумент6 страницRefinancing Risk: Solutions For End-of-Chapter Questions and Problems: Chapter SevenJeffОценок пока нет

- Definition of Money MarketsДокумент21 страницаDefinition of Money Marketsnelle de leonОценок пока нет

- Cost of CapitalДокумент3 страницыCost of CapitalSuman MandalОценок пока нет

- DRIVATIVES Options Call & Put KKДокумент134 страницыDRIVATIVES Options Call & Put KKAjay Raj ShuklaОценок пока нет

- Financial AccountingДокумент46 страницFinancial AccountingNeil GriggОценок пока нет

- Unit 3 TVM Live SessionДокумент43 страницыUnit 3 TVM Live Sessionkimj22614Оценок пока нет

- CFДокумент11 страницCFPreetesh ChoudhariОценок пока нет

- Calculating Bond Yield-to-MaturityДокумент2 страницыCalculating Bond Yield-to-MaturityManuj RathoreОценок пока нет

- FInance CaseДокумент7 страницFInance CaseAnkit PoudelОценок пока нет

- Stock Market Basics and Stock Pricing: Mishkin CH 7 - Part A Page 151-159 Plus Supplementary Lecture NotesДокумент20 страницStock Market Basics and Stock Pricing: Mishkin CH 7 - Part A Page 151-159 Plus Supplementary Lecture NotesraviОценок пока нет

- FINA 3780 Chapter 6Документ33 страницыFINA 3780 Chapter 6roBinОценок пока нет

- Topic 7-ValuationДокумент36 страницTopic 7-ValuationK60 Nguyễn Ngọc Quế AnhОценок пока нет

- Overview of Bond Sectors and InstrumentsДокумент32 страницыOverview of Bond Sectors and InstrumentsShrirang LichadeОценок пока нет

- Chapter 03Документ62 страницыChapter 03Quỳnh NhưОценок пока нет

- Financial Markets QuestionsДокумент54 страницыFinancial Markets QuestionsMathias VindalОценок пока нет

- Govt SecuritiesДокумент81 страницаGovt SecuritiesJeenal KaraniОценок пока нет

- Lecture 0 Bond ValuationДокумент59 страницLecture 0 Bond ValuationKrati SinghalОценок пока нет

- Chapter 5 Global Bond InvestmentДокумент51 страницаChapter 5 Global Bond InvestmentThư Trần Thị AnhОценок пока нет

- Interest Bond CalculatorДокумент6 страницInterest Bond CalculatorfdfsfsdfjhgjghОценок пока нет

- Understanding Treasury FuturesДокумент22 страницыUnderstanding Treasury FuturesYossi LonkeОценок пока нет

- Midterm Exam 2 - SolutionДокумент6 страницMidterm Exam 2 - SolutionbobtanlaОценок пока нет

- Dividend Investing During Turbulent Times: Financial Freedom, #130От EverandDividend Investing During Turbulent Times: Financial Freedom, #130Оценок пока нет

- Nice AND Easy German GrammarДокумент90 страницNice AND Easy German Grammaralemici93% (46)

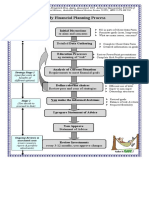

- Plan Process PDFДокумент1 страницаPlan Process PDFLuís Gustavo GrigolettoОценок пока нет

- Varieties of Capitalism in Estonia and Slovenia PDFДокумент22 страницыVarieties of Capitalism in Estonia and Slovenia PDFLuís Gustavo GrigolettoОценок пока нет

- Czech Economic EliteДокумент20 страницCzech Economic EliteLuís Gustavo GrigolettoОценок пока нет

- Risk Management Options and DerivativesДокумент13 страницRisk Management Options and DerivativesAbdu0% (1)

- TIPS Vs TreasuriesДокумент8 страницTIPS Vs TreasurieszdfgbsfdzcgbvdfcОценок пока нет

- Wac12 2019 May A2 MS PDFДокумент34 страницыWac12 2019 May A2 MS PDFAbu Daiyan Bin Saleh ZidaneОценок пока нет

- Quantitative Problems Chapter 3Документ5 страницQuantitative Problems Chapter 3Deng JuniorОценок пока нет

- Choose The Correct Answer From The Given Four Alternatives:: Not Attempt!!!! Rs. 452 LacsДокумент10 страницChoose The Correct Answer From The Given Four Alternatives:: Not Attempt!!!! Rs. 452 LacsHari BabuОценок пока нет

- Financial ManagementДокумент6 страницFinancial ManagementRon BoostОценок пока нет

- Marketing Strategy For ICICI Prudential AMC To Become Topmost Preferred AMC in DebtДокумент42 страницыMarketing Strategy For ICICI Prudential AMC To Become Topmost Preferred AMC in DebtAmit SharmaОценок пока нет

- Financial markets, treasury functions, and risk management in banksДокумент12 страницFinancial markets, treasury functions, and risk management in banksDiwakar PasrichaОценок пока нет

- TRADE FIXED INCOME SECURITIESДокумент15 страницTRADE FIXED INCOME SECURITIESChetal BholeОценок пока нет

- Callable Bonds ExplainedДокумент33 страницыCallable Bonds ExplainedtwinklenoorОценок пока нет

- SFM Formula BookДокумент29 страницSFM Formula BookAstikОценок пока нет

- Draft OF Assessing MUNICIPAL Bond Default ProbabilitIes of California Cities 2013Документ154 страницыDraft OF Assessing MUNICIPAL Bond Default ProbabilitIes of California Cities 201383jjmackОценок пока нет

- Financial Management: Key ConceptsДокумент173 страницыFinancial Management: Key ConceptsAndreea Cristina DiaconuОценок пока нет

- American Home ProductsДокумент6 страницAmerican Home Productssunitha_ratnakaram100% (1)

- 4-Time Value of Money Business Finance 1Документ39 страниц4-Time Value of Money Business Finance 1faizy24Оценок пока нет

- Investment Analysis and Portfolio Management (Mba 3RD Sem) (Akanksha)Документ30 страницInvestment Analysis and Portfolio Management (Mba 3RD Sem) (Akanksha)priyank chourasiyaОценок пока нет

- Capital markets facilitate long-term funds over 1 yearДокумент3 страницыCapital markets facilitate long-term funds over 1 yearThuỳ Linh100% (8)

- Chapter 7Документ25 страницChapter 7Baby KhorОценок пока нет

- Wiley CMA Test Bank Part 2 ReviewДокумент66 страницWiley CMA Test Bank Part 2 ReviewKy DulzОценок пока нет

- Employee Benefits P201Документ17 страницEmployee Benefits P201krisha milloОценок пока нет

- Sar 194857Документ144 страницыSar 194857William HarrisОценок пока нет

- QF2104 Tutorial - Assignment 4Документ3 страницыQF2104 Tutorial - Assignment 4igndunnoОценок пока нет

- CSI GlossaryДокумент44 страницыCSI Glossarygrz7gtqq9bОценок пока нет

- 104 - Indicatorii BursieriДокумент11 страниц104 - Indicatorii BursieriDragos MacoveiОценок пока нет

- Singapore Property & REITs Focus: Developers' Valuations Too Cheap to IgnoreДокумент310 страницSingapore Property & REITs Focus: Developers' Valuations Too Cheap to Ignoremonami.sankarsanОценок пока нет

- 20200920180007HCTAN008S T2 Financial SystemДокумент48 страниц20200920180007HCTAN008S T2 Financial SystemDương DươngОценок пока нет

- Sample Ch2Документ34 страницыSample Ch2DamTokyoОценок пока нет

- Tiob Launched Digital Membership Identification Cards: News FeaturesДокумент5 страницTiob Launched Digital Membership Identification Cards: News FeaturesArden Muhumuza KitomariОценок пока нет

- Comprehensive Review - 2011Документ78 страницComprehensive Review - 2011LBL_LowkeeОценок пока нет

- Financial Management Chapter - Bond and Stock ValuationДокумент6 страницFinancial Management Chapter - Bond and Stock ValuationNahidul Islam IUОценок пока нет