Вам также может понравиться

- Fundamentals of Corporate Finance: Discounted Cash Flow ValuationДокумент41 страницаFundamentals of Corporate Finance: Discounted Cash Flow ValuationThành NguyễnОценок пока нет

- Time Value of Money: Present and Future Values Present and Future Value Factors Compounding Growing Income StreamsДокумент64 страницыTime Value of Money: Present and Future Values Present and Future Value Factors Compounding Growing Income StreamsPranulfc RagaОценок пока нет

- 2.1 - Swaps, Bridge To SwapsДокумент56 страниц2.1 - Swaps, Bridge To SwapscutehibouxОценок пока нет

- FM11 CH 12 Mini CaseДокумент14 страницFM11 CH 12 Mini CaseRahul Rathi100% (1)

- Project Evaluation TechniquesДокумент30 страницProject Evaluation TechniquesMujeeb KhanОценок пока нет

- Capital Budgeting: Part I Investment CriteriaДокумент49 страницCapital Budgeting: Part I Investment Criteriarani namdevОценок пока нет

- Async CFin-I Annuities and Perpetuities Friday 5august2022Документ35 страницAsync CFin-I Annuities and Perpetuities Friday 5august2022SSОценок пока нет

- Capital Budgeting - Part I PDFДокумент83 страницыCapital Budgeting - Part I PDFJannat JavedОценок пока нет

- Capital Budgeting V2 - Click Read Only To View DocumentДокумент40 страницCapital Budgeting V2 - Click Read Only To View Documentzia hussain100% (1)

- Lecture 7Документ7 страницLecture 7bbasmiuОценок пока нет

- HW 3Документ24 страницыHW 3Matthew RyanОценок пока нет

- Present ValueДокумент6 страницPresent ValuecelsoОценок пока нет

- Capital Budgeting V2 - Click Read Only To View DocumentДокумент40 страницCapital Budgeting V2 - Click Read Only To View DocumentSamantha Meril PandithaОценок пока нет

- Capital BudgetingДокумент70 страницCapital BudgetingAvirup ChakrabortyОценок пока нет

- TVM Lecture 3Документ42 страницыTVM Lecture 380tekОценок пока нет

- Chapter 1 - Overview - 2022 - SДокумент100 страницChapter 1 - Overview - 2022 - SĐức Nam TrầnОценок пока нет

- Fundamentals of Corporate Finance 11th Edition Ross Solutions ManualДокумент11 страницFundamentals of Corporate Finance 11th Edition Ross Solutions ManualElizabethFuentesrfaj100% (38)

- CF Lecture 2 Time Value of Money v1Документ50 страницCF Lecture 2 Time Value of Money v1Tâm NhưОценок пока нет

- Investment Appraisal Using DCF MethodsДокумент47 страницInvestment Appraisal Using DCF MethodsMohit GolechaОценок пока нет

- Capital Budgeting-Investment Decision CriteriaДокумент57 страницCapital Budgeting-Investment Decision CriteriaSheila ArjonaОценок пока нет

- Concepts of Value and ReturnДокумент38 страницConcepts of Value and Returnravi anandОценок пока нет

- Investment Appraisal Techniques: Prepared By: Ms ShazДокумент37 страницInvestment Appraisal Techniques: Prepared By: Ms Shazshazlina_liОценок пока нет

- SS6 Chapter 06 v0Документ30 страницSS6 Chapter 06 v0Thúy An NguyễnОценок пока нет

- Intermediate Accounting 2 Week 2 Lecture NotesДокумент5 страницIntermediate Accounting 2 Week 2 Lecture NotesdeeznutsОценок пока нет

- Intermediate Accounting 2 Week 2 Lecture AY 2020-2021 Chapter 2:notes PayableДокумент5 страницIntermediate Accounting 2 Week 2 Lecture AY 2020-2021 Chapter 2:notes PayabledeeznutsОценок пока нет

- Cash Flow Rate of Return (DCFROR), Payback PeriodДокумент2 страницыCash Flow Rate of Return (DCFROR), Payback PeriodPeter TolibasОценок пока нет

- BFD - Weighted Average Cost of Capital by Ahmed Raza Mir & Taha PopatiaДокумент6 страницBFD - Weighted Average Cost of Capital by Ahmed Raza Mir & Taha PopatiaAiman TuhaОценок пока нет

- The Two Key Concepts in FinanceДокумент63 страницыThe Two Key Concepts in FinanceJai SharmaОценок пока нет

- FE1 Chapter 4Документ41 страницаFE1 Chapter 4Hùng PhanОценок пока нет

- THE TIME VALUE OF MONEY EXPLAINEDДокумент10 страницTHE TIME VALUE OF MONEY EXPLAINEDNirmal ShresthaОценок пока нет

- Lec 04 Time Value of MoneyДокумент24 страницыLec 04 Time Value of MoneyOptimistic EyeОценок пока нет

- Capital Budgeting: Dr. Akshita Arora IBS-GurgaonДокумент24 страницыCapital Budgeting: Dr. Akshita Arora IBS-GurgaonhitanshuОценок пока нет

- Expenditure Decisions: DCF MethodologiesДокумент46 страницExpenditure Decisions: DCF MethodologiesRam Surya Prakash DommetiОценок пока нет

- Solution For Financial FunctionsДокумент4 страницыSolution For Financial FunctionsJorge JraigeОценок пока нет

- Capital BudgetingДокумент27 страницCapital BudgetingRishi CharanОценок пока нет

- Allocating Resources Over TimeДокумент27 страницAllocating Resources Over TimeDuy TânОценок пока нет

- NPV vs Payback - Which Capital Budgeting Method Is BestДокумент72 страницыNPV vs Payback - Which Capital Budgeting Method Is BestAbdullah MujahidОценок пока нет

- Kewirausahaan Konsep-Konsep Keuangan: Dteti 2021Документ27 страницKewirausahaan Konsep-Konsep Keuangan: Dteti 2021PANDHU ARDI PRASETYOОценок пока нет

- Pitt - Edu Schlinge Fall99 L7docДокумент40 страницPitt - Edu Schlinge Fall99 L7docCheryl GanitОценок пока нет

- Formulas and Calculation: NPV CalculationsДокумент3 страницыFormulas and Calculation: NPV Calculationssadianasir960Оценок пока нет

- 5.2 Discounted Cash Flows, Internal Rate of Return, ROI. Feb 8-12. 2Документ13 страниц5.2 Discounted Cash Flows, Internal Rate of Return, ROI. Feb 8-12. 2John GarciaОценок пока нет

- Time Value of Money ExplainedДокумент53 страницыTime Value of Money ExplainedgokulkОценок пока нет

- Net Present Value and Other Investment Rules: Mcgraw-Hill/IrwinДокумент34 страницыNet Present Value and Other Investment Rules: Mcgraw-Hill/IrwinQUYÊN PHAN ĐÌNH PHƯƠNGОценок пока нет

- NPV and IRR investment rulesДокумент37 страницNPV and IRR investment rulesBouchraya MilitoОценок пока нет

- Unit 5 - Single Project EvaluationДокумент38 страницUnit 5 - Single Project EvaluationAadeem NyaichyaiОценок пока нет

- CAIIB Paper 1 Moudle B Business Mathmatics PDF 2021Документ32 страницыCAIIB Paper 1 Moudle B Business Mathmatics PDF 2021DurgaОценок пока нет

- CH 02 RevisedДокумент38 страницCH 02 RevisedZia AhmadОценок пока нет

- Valuation of Financial AssetsДокумент47 страницValuation of Financial AssetsprashantkumbhaniОценок пока нет

- Bond Mathematics ExplainedДокумент35 страницBond Mathematics Explainedrohan.explorerОценок пока нет

- Time Value of MoneyДокумент43 страницыTime Value of MoneyEdwin OctorizaОценок пока нет

- Time Value of MoneyДокумент14 страницTime Value of MoneyYasir AyazОценок пока нет

- TVM: Calculating Future, Present Values and Loan PaymentsДокумент26 страницTVM: Calculating Future, Present Values and Loan PaymentsSushil KharelОценок пока нет

- Ch04Full Time ValueДокумент65 страницCh04Full Time Valuek61.2214535043Оценок пока нет

- The Time Value of Money ConceptsДокумент28 страницThe Time Value of Money ConceptsJanzel SantillanОценок пока нет

- Ufanpv Irr1.2Документ45 страницUfanpv Irr1.2mayankОценок пока нет

- Topic 2. Discounting: Future ValueДокумент13 страницTopic 2. Discounting: Future ValueАндрей ДымовОценок пока нет

- Net Present Value (NPV)Документ28 страницNet Present Value (NPV)KAORU AmaneОценок пока нет

- Chapter 3 - Investment Analysis & .....Документ58 страницChapter 3 - Investment Analysis & .....Behailu TesfayeОценок пока нет

- Decoding DCF: A Beginner's Guide to Discounted Cash Flow AnalysisОт EverandDecoding DCF: A Beginner's Guide to Discounted Cash Flow AnalysisОценок пока нет

- Tuca-Calibration of LMM - Comparison Between Separated and Approximated ApproachДокумент52 страницыTuca-Calibration of LMM - Comparison Between Separated and Approximated Approachswinki3Оценок пока нет

- Calculating Convexity Adjustment for Interest Rates Using Martingale TheoryДокумент18 страницCalculating Convexity Adjustment for Interest Rates Using Martingale Theoryswinki3Оценок пока нет

- Tu-Is Regime Switching in Stock Returns Important in Portfolio DecisionsДокумент46 страницTu-Is Regime Switching in Stock Returns Important in Portfolio Decisionsswinki3Оценок пока нет

- How To Create An Operating SystemДокумент36 страницHow To Create An Operating Systemecartman2100% (1)

- Bare Metal CPPДокумент199 страницBare Metal CPPswinki3Оценок пока нет

- Shinada-Actual Factors To Determine Cross-Currency Basis Swaps An Empirical Study On US Dollar-Japanese Yen Basis Swap Rates From The Late 1990sДокумент14 страницShinada-Actual Factors To Determine Cross-Currency Basis Swaps An Empirical Study On US Dollar-Japanese Yen Basis Swap Rates From The Late 1990sswinki3Оценок пока нет

- Convexity BiasДокумент26 страницConvexity Biasswinki3Оценок пока нет

- Bonds Analysis ValuationДокумент52 страницыBonds Analysis Valuationswinki3Оценок пока нет

- Major Challenges in Collateral ManagementДокумент22 страницыMajor Challenges in Collateral Managementswinki3Оценок пока нет

- The Atlas of Economic Indicators PDFДокумент123 страницыThe Atlas of Economic Indicators PDFswinki383% (6)

- CPP Best PracticesДокумент45 страницCPP Best Practicesswinki3Оценок пока нет

- ISDA Section 10 Overview of Derivatives TechnologyДокумент35 страницISDA Section 10 Overview of Derivatives Technologyswinki3Оценок пока нет

- Lehman Brothers: Guide To Exotic Credit DerivativesДокумент60 страницLehman Brothers: Guide To Exotic Credit DerivativesCrodoleОценок пока нет

- Accounting for Derivatives and Hedging ActivitiesДокумент22 страницыAccounting for Derivatives and Hedging Activitiesswinki3Оценок пока нет

- JPMorgan DerivativesДокумент55 страницJPMorgan Derivativesswinki3Оценок пока нет

- ISDA Section 02 AgendaДокумент11 страницISDA Section 02 Agendaswinki3Оценок пока нет

- ISDA Section 11 Hand NotesДокумент7 страницISDA Section 11 Hand Notesswinki3Оценок пока нет

- ISDA Section 08 Rate Sets and SettlementsДокумент21 страницаISDA Section 08 Rate Sets and Settlementsswinki3Оценок пока нет

- 2005 ISDA Conference Prime Brokerage As TheДокумент4 страницы2005 ISDA Conference Prime Brokerage As Theswinki3Оценок пока нет

- ISDA Section 07 Trade CaptureДокумент14 страницISDA Section 07 Trade Captureswinki3Оценок пока нет

- ISDA Section 05 Swaps Global OperationsДокумент7 страницISDA Section 05 Swaps Global Operationsswinki3Оценок пока нет

- 2005 ISDA Conference NovationsДокумент3 страницы2005 ISDA Conference Novationsswinki3Оценок пока нет

- ISDA Conference On Structured Products CDSДокумент15 страницISDA Conference On Structured Products CDSswinki3Оценок пока нет

- ISDA Section 03 Interest Rate and Currency DerivativesДокумент82 страницыISDA Section 03 Interest Rate and Currency Derivativesswinki3Оценок пока нет

- ISDA 2000 Board of DirectorsДокумент37 страницISDA 2000 Board of Directorsswinki3Оценок пока нет

- ISDA Section 00 Table of ContentsДокумент3 страницыISDA Section 00 Table of Contentsswinki3Оценок пока нет

- Equity Derivatives OverviewДокумент15 страницEquity Derivatives Overviewswinki3Оценок пока нет

- 2005 ISDA Conference Netting and CollateralДокумент13 страниц2005 ISDA Conference Netting and Collateralswinki3Оценок пока нет

- 2005 ISDA Conference Overview of Pay-As-YouДокумент5 страниц2005 ISDA Conference Overview of Pay-As-Youswinki3Оценок пока нет

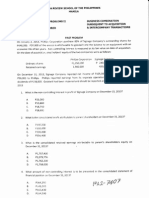

- CPA REVIEW SCHOOL PHILIPPINES BUSINESS COMBINATIONSДокумент5 страницCPA REVIEW SCHOOL PHILIPPINES BUSINESS COMBINATIONSAngelo Villadores100% (3)

- B Liquid Yield Option NoteДокумент2 страницыB Liquid Yield Option NoteDanica BalinasОценок пока нет

- Tybfm Sem 6 Venture Capital Unit II & IIIДокумент19 страницTybfm Sem 6 Venture Capital Unit II & IIIElamathiОценок пока нет

- Choose The Correct Answer From The Given Four Alternatives:: Not Attempt!!!! Public Provident FundДокумент11 страницChoose The Correct Answer From The Given Four Alternatives:: Not Attempt!!!! Public Provident FundHari BabuОценок пока нет

- Debt PolicyДокумент2 страницыDebt PolicyKathy Beth TerryОценок пока нет

- Advance Swing Analysis PDFДокумент58 страницAdvance Swing Analysis PDFnts100% (2)

- Homework For Debt & EquityДокумент6 страницHomework For Debt & EquityPetra100% (1)

- Quiz 6 Market Value Approach True or False Multiple Choice Theory ProblemsДокумент4 страницыQuiz 6 Market Value Approach True or False Multiple Choice Theory ProblemsRissa AgapeОценок пока нет

- Strictly Private and Confidential Road to IPOДокумент24 страницыStrictly Private and Confidential Road to IPOedyОценок пока нет

- 07 Task Performance 1 - FinmarДокумент2 страницы07 Task Performance 1 - FinmarJen DeloyОценок пока нет

- Soneri Bank Limited Balance SheetДокумент3 страницыSoneri Bank Limited Balance SheetSaad Ur RehmanОценок пока нет

- PRIYANKA RAWAT - BLACK BOOK Sem 4Документ70 страницPRIYANKA RAWAT - BLACK BOOK Sem 4m.com22shiudkarsudarshanОценок пока нет

- Financial Derivatives: A Derivative A Financial InstrumentДокумент17 страницFinancial Derivatives: A Derivative A Financial Instrumentmohammad bilalОценок пока нет

- 7 Step Trade Entry Checklist1 PDFДокумент9 страниц7 Step Trade Entry Checklist1 PDFashlogicОценок пока нет

- DerivaGem 2Документ10 страницDerivaGem 2Vicky RajoraОценок пока нет

- Summary of 'Buffett's Alpha'Документ2 страницыSummary of 'Buffett's Alpha'Shyngys SuiindikОценок пока нет

- Bus - Valuation - StudentДокумент5 страницBus - Valuation - StudentMilan TilvaОценок пока нет

- SCDL - Capital MarketДокумент75 страницSCDL - Capital MarketManish Garg100% (4)

- Chapter 5 - Financial MarketsДокумент9 страницChapter 5 - Financial MarketsThuyển ThuyểnОценок пока нет

- IdxxxДокумент197 страницIdxxxBulan Rahma NinditaОценок пока нет

- Midterm Examination Questions Derivatives BUPДокумент4 страницыMidterm Examination Questions Derivatives BUPAqid Ahmed AnsariОценок пока нет

- Mutual Funds and Other Investment CompaniesДокумент27 страницMutual Funds and Other Investment CompaniesJyra MendezОценок пока нет

- Options Wheel StrategyДокумент13 страницOptions Wheel StrategyShao MaОценок пока нет

- Atta Hur LTD Prospectus FinalДокумент135 страницAtta Hur LTD Prospectus FinalSarosh NagraОценок пока нет

- Intermediate Guide To E-Mini Futures Contracts - Rollover Dates and Expiration - InvestopediaДокумент5 страницIntermediate Guide To E-Mini Futures Contracts - Rollover Dates and Expiration - Investopediarsumant1Оценок пока нет

- Share-Based Compensation: Learning ObjectivesДокумент48 страницShare-Based Compensation: Learning ObjectivesMark S MadsenОценок пока нет

- Introduction To Derivatives and Risk Management 10th Edition Chance Test BankДокумент8 страницIntroduction To Derivatives and Risk Management 10th Edition Chance Test BankMavos OdinОценок пока нет

- Wednesday, January 21, 2015: Bonus Debentures: Features and ImplicationsДокумент7 страницWednesday, January 21, 2015: Bonus Debentures: Features and ImplicationsnisseemkОценок пока нет

- Debt Fund FeaturesДокумент18 страницDebt Fund FeaturesAmit ShahОценок пока нет

- Cfin 6th Edition Besley Test BankДокумент15 страницCfin 6th Edition Besley Test Bankdrkevinlee03071984jki100% (26)