Вам также может понравиться

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- SMART V Dava0, CIR vs. CA, CIR v. UCBPДокумент6 страницSMART V Dava0, CIR vs. CA, CIR v. UCBPKath LeenОценок пока нет

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Sison JR VS AnchetaДокумент2 страницыSison JR VS AnchetaKath Leen100% (1)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- TAN Vs DEL ROSARIOДокумент3 страницыTAN Vs DEL ROSARIOKath LeenОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Rem 2 DigestДокумент69 страницRem 2 DigestKath LeenОценок пока нет

- TAX EXEMPTION OF NON-STOCK, NON-PROFIT EDUCATIONAL INSTITUTION - ANGELES UNIVERSITY vs. CITY OF ANGELESДокумент4 страницыTAX EXEMPTION OF NON-STOCK, NON-PROFIT EDUCATIONAL INSTITUTION - ANGELES UNIVERSITY vs. CITY OF ANGELESKath LeenОценок пока нет

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Shell Vs VanoДокумент2 страницыShell Vs VanoKath LeenОценок пока нет

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Silkair vs. CirДокумент2 страницыSilkair vs. CirKath Leen100% (1)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Judy Anne Santos v. People, G.R. No. 173176, August 26, 2008 FactsДокумент2 страницыJudy Anne Santos v. People, G.R. No. 173176, August 26, 2008 FactsKath LeenОценок пока нет

- PROSPECTIVITY OF LAWS - Commissioner of Internal Revenue vs. AcostaДокумент2 страницыPROSPECTIVITY OF LAWS - Commissioner of Internal Revenue vs. AcostaKath LeenОценок пока нет

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Philreca VS DilgДокумент3 страницыPhilreca VS DilgKath LeenОценок пока нет

- Philex VS CirДокумент2 страницыPhilex VS CirKath LeenОценок пока нет

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- JOHN HAY PEOPLES ALTERNATIVE COALITION Vs LIMДокумент4 страницыJOHN HAY PEOPLES ALTERNATIVE COALITION Vs LIMKath Leen100% (1)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- NO ESTOPPEL AGAINST THE GOVERNMENT Commissioner of Internal Revenue vs. PetronДокумент2 страницыNO ESTOPPEL AGAINST THE GOVERNMENT Commissioner of Internal Revenue vs. PetronKath LeenОценок пока нет

- MIAA Vs - CIty of ParanaqueДокумент3 страницыMIAA Vs - CIty of ParanaqueKath Leen100% (2)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- Brye Dongz-Manila Electric Co, Inc. vs. Province of LagunaДокумент3 страницыBrye Dongz-Manila Electric Co, Inc. vs. Province of LagunaKath Leen100% (1)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Rcpi VS Provincial AssessorДокумент3 страницыRcpi VS Provincial AssessorKath LeenОценок пока нет

- MCIAA vs. MarcosДокумент2 страницыMCIAA vs. MarcosKath LeenОценок пока нет

- Forms of Escape From TaxationДокумент6 страницForms of Escape From TaxationKath LeenОценок пока нет

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Lladoc VS CirДокумент2 страницыLladoc VS CirKath LeenОценок пока нет

- Topic: Tax Treaties Deutsche Bank Ag Manila Branch Vs Cir FactsДокумент1 страницаTopic: Tax Treaties Deutsche Bank Ag Manila Branch Vs Cir FactsKath LeenОценок пока нет

- Commissioner of Internal RevenueДокумент3 страницыCommissioner of Internal RevenueKath LeenОценок пока нет

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- LRTA vs. CBAAДокумент2 страницыLRTA vs. CBAAKath LeenОценок пока нет

- CIR vs. ST Lukes DigestДокумент2 страницыCIR vs. ST Lukes DigestKath Leen100% (4)

- Contex Corp vs. CirДокумент3 страницыContex Corp vs. CirKath Leen100% (1)

- City of Baguio vs. de Leon DigestДокумент2 страницыCity of Baguio vs. de Leon DigestKath Leen100% (1)

- CIR vs. Central Luzon Drug Corp GR. 159647 and CIR Vs Central Luzon Drug Corp. GR No. 148512Документ4 страницыCIR vs. Central Luzon Drug Corp GR. 159647 and CIR Vs Central Luzon Drug Corp. GR No. 148512Kath Leen100% (1)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- CIR V American RubberДокумент2 страницыCIR V American RubberKath Leen0% (1)

- FAR3Документ6 страницFAR3Hermie TimarioОценок пока нет

- Bachelor of Administration (Hons) in Islamic Finance: Waqf EBB30503Документ15 страницBachelor of Administration (Hons) in Islamic Finance: Waqf EBB30503irfan sururiОценок пока нет

- XYZ Water Inc. FAN ProtestДокумент16 страницXYZ Water Inc. FAN ProtestRalf Arthur SilverioОценок пока нет

- Chapter 18 22 Taxation 2Документ67 страницChapter 18 22 Taxation 2Zvioule Ma FuentesОценок пока нет

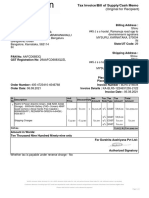

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Документ1 страницаTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Shiva Kumar0% (1)

- Inland Revenue Board of Malaysia: Residence Status of IndividualsДокумент26 страницInland Revenue Board of Malaysia: Residence Status of Individualsabhishekmath123Оценок пока нет

- Paywithtaxslip 102324 PDFДокумент1 страницаPaywithtaxslip 102324 PDFamitshrivastava154218Оценок пока нет

- Financial Planning and Wealth ManagementДокумент58 страницFinancial Planning and Wealth ManagementsohanlОценок пока нет

- (TAX 1) Scope and Limitations - 05 JRRBДокумент3 страницы(TAX 1) Scope and Limitations - 05 JRRBJay-ar Rivera BadulisОценок пока нет

- Commisioner of Costum Vs Oilink International CorporationДокумент1 страницаCommisioner of Costum Vs Oilink International Corporationhigoremso giensdksОценок пока нет

- Tax Prep Advisers Inc Has Forecasted The Following Staffing RequirementsДокумент1 страницаTax Prep Advisers Inc Has Forecasted The Following Staffing RequirementsAmit PandeyОценок пока нет

- 6th Class Physics Text BookДокумент1 страница6th Class Physics Text BookSrinu SehwagОценок пока нет

- CA Final IBS A MTP 1 May 2024 Castudynotes ComДокумент36 страницCA Final IBS A MTP 1 May 2024 Castudynotes Comamanjain254Оценок пока нет

- 0015 1947 Article A005 en PDFДокумент4 страницы0015 1947 Article A005 en PDFProject BluebellОценок пока нет

- Blakemore Freeman Fellowship InformationДокумент6 страницBlakemore Freeman Fellowship InformationTaiwanSummerProgramsОценок пока нет

- Guide Doing Business in Tanzania Digital 1Документ36 страницGuide Doing Business in Tanzania Digital 1Yaula SiminyuОценок пока нет

- 425 1594 1 PBДокумент23 страницы425 1594 1 PBWOYOPWA SHEMОценок пока нет

- Emirates Fare ConditionsДокумент6 страницEmirates Fare ConditionsMPC RaoОценок пока нет

- G.O. Rt. No. 192, Dated 09-05-2020Документ2 страницыG.O. Rt. No. 192, Dated 09-05-2020sampathОценок пока нет

- Hierarchical ModesДокумент19 страницHierarchical ModesAlexandra MihutОценок пока нет

- Dividends TaxationДокумент3 страницыDividends TaxationGuruОценок пока нет

- How To Calculate Custom DutyДокумент15 страницHow To Calculate Custom DutyDr-Koteswara Rao0% (1)

- Nyse Sap 2018Документ190 страницNyse Sap 2018Naveen KumarОценок пока нет

- Collector ManualДокумент1 206 страницCollector ManualJayanti DaburiaОценок пока нет

- Dick Stewart's Letter To SCPA's Peter Lehman Dated Feb. 13, 2014Документ10 страницDick Stewart's Letter To SCPA's Peter Lehman Dated Feb. 13, 2014Island Packet and Beaufort GazetteОценок пока нет

- F 09420010120134019 PP T 06Документ21 страницаF 09420010120134019 PP T 06Morita MichieОценок пока нет

- Adam Smith SummaryДокумент9 страницAdam Smith SummarySargun MehramОценок пока нет

- Introduction To Agriculture Lecture Notes NewДокумент35 страницIntroduction To Agriculture Lecture Notes NewAnonymous S8YHHo51M86% (7)

- MFGPro MenuListДокумент266 страницMFGPro MenuListJay TracewellОценок пока нет

- CT 1 - QP - Icse - X - GSTДокумент2 страницыCT 1 - QP - Icse - X - GSTAnanya IyerОценок пока нет

- Building Construction Technology: A Useful Guide - Part 1От EverandBuilding Construction Technology: A Useful Guide - Part 1Рейтинг: 4 из 5 звезд4/5 (3)

- A Place of My Own: The Architecture of DaydreamsОт EverandA Place of My Own: The Architecture of DaydreamsРейтинг: 4 из 5 звезд4/5 (242)

- Building Physics -- Heat, Air and Moisture: Fundamentals and Engineering Methods with Examples and ExercisesОт EverandBuilding Physics -- Heat, Air and Moisture: Fundamentals and Engineering Methods with Examples and ExercisesОценок пока нет

- How to Estimate with RSMeans Data: Basic Skills for Building ConstructionОт EverandHow to Estimate with RSMeans Data: Basic Skills for Building ConstructionРейтинг: 4.5 из 5 звезд4.5/5 (2)

- Principles of Welding: Processes, Physics, Chemistry, and MetallurgyОт EverandPrinciples of Welding: Processes, Physics, Chemistry, and MetallurgyРейтинг: 4 из 5 звезд4/5 (1)

- Pressure Vessels: Design, Formulas, Codes, and Interview Questions & Answers ExplainedОт EverandPressure Vessels: Design, Formulas, Codes, and Interview Questions & Answers ExplainedРейтинг: 5 из 5 звезд5/5 (1)