Вам также может понравиться

- 2 - Steps For Kiosk Banking SolutionДокумент1 страница2 - Steps For Kiosk Banking SolutionGreatway ServicesОценок пока нет

- Phone:-Director Office FAX WWW - Kerala.gov - in 0471-2305230 0471-2305193 0471-2301740Документ2 страницыPhone:-Director Office FAX WWW - Kerala.gov - in 0471-2305230 0471-2305193 0471-2301740Greatway ServicesОценок пока нет

- 12 Chapter 4Документ45 страниц12 Chapter 4Greatway ServicesОценок пока нет

- The Role of National Bank For Agriculture and Rural Development (Nabard) in Agriculture and Rural DevelopmentДокумент1 страницаThe Role of National Bank For Agriculture and Rural Development (Nabard) in Agriculture and Rural DevelopmentGreatway ServicesОценок пока нет

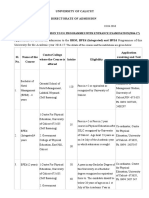

- Recgnized Courses On23Nov2015Документ7 страницRecgnized Courses On23Nov2015Greatway ServicesОценок пока нет

- Understanding Marginal Costing and Its SignificanceДокумент29 страницUnderstanding Marginal Costing and Its SignificanceGreatway ServicesОценок пока нет

- A Study On Fishermen Co-Operative Society in KeralaДокумент24 страницыA Study On Fishermen Co-Operative Society in KeralaGreatway Services0% (1)

- P!Vhil®Ifim111Nitm S@D ©if N&Ib&Irb) : Chapter-VДокумент26 страницP!Vhil®Ifim111Nitm S@D ©if N&Ib&Irb) : Chapter-VGreatway ServicesОценок пока нет

- Understanding Marginal Costing and Its SignificanceДокумент29 страницUnderstanding Marginal Costing and Its SignificanceGreatway ServicesОценок пока нет

- ProfileДокумент1 страницаProfileGreatway ServicesОценок пока нет

- Evening Brach in Co Operative BankДокумент28 страницEvening Brach in Co Operative BankGreatway ServicesОценок пока нет

- NCUBДокумент30 страницNCUBGreatway ServicesОценок пока нет

- Chapter-2 Review of Literature: Bhatia (1978), in His Study Titled, "Banking Structure and Performance A CaseДокумент28 страницChapter-2 Review of Literature: Bhatia (1978), in His Study Titled, "Banking Structure and Performance A CaseApoorvaОценок пока нет

- Compensation ManagementДокумент11 страницCompensation ManagementGreatway ServicesОценок пока нет

- Financial Statement Analysis of Salibury Tea FactoryДокумент27 страницFinancial Statement Analysis of Salibury Tea FactoryGreatway Services50% (2)

- Ug Ent NotifДокумент3 страницыUg Ent NotifGreatway ServicesОценок пока нет

- Etreasury ManualДокумент14 страницEtreasury ManualGreatway ServicesОценок пока нет

- Co - Operative Banks in Kerala - An OverviewДокумент27 страницCo - Operative Banks in Kerala - An Overviewmalayali100100% (1)

- HAJ APPLICATION FORMДокумент4 страницыHAJ APPLICATION FORMGreatway ServicesОценок пока нет

- El Guadual Children Center - ColumbiaДокумент14 страницEl Guadual Children Center - ColumbiaGreatway ServicesОценок пока нет

- Norka PDFДокумент1 страницаNorka PDFGreatway ServicesОценок пока нет

- Kasturirangan Report 2013Документ175 страницKasturirangan Report 2013prijucpОценок пока нет

- WES ApplicationДокумент5 страницWES ApplicationGreatway ServicesОценок пока нет

- Multi State Co-Operatives Bill PDFДокумент29 страницMulti State Co-Operatives Bill PDFGreatway ServicesОценок пока нет

- NORKA SPECIAL SCHEME FOR RETURNING EMIGRANTSДокумент1 страницаNORKA SPECIAL SCHEME FOR RETURNING EMIGRANTSGreatway ServicesОценок пока нет

- 02 Components of The Computer System - HssliveДокумент10 страниц02 Components of The Computer System - HssliveGreatway ServicesОценок пока нет

- 03 Principles of Programming and Problem Solving - HssliveДокумент5 страниц03 Principles of Programming and Problem Solving - HssliveGreatway ServicesОценок пока нет

- ONLINE User Manual SocietyДокумент21 страницаONLINE User Manual Societylotus@79Оценок пока нет

- Tiruchirappalli District Co-Operative Milk Producers Union LimitedДокумент27 страницTiruchirappalli District Co-Operative Milk Producers Union LimitedGreatway ServicesОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Budokon - Mma.program 2012 13Документ10 страницBudokon - Mma.program 2012 13Emilio DiazОценок пока нет

- Expansion Analysis of Offshore PipelineДокумент25 страницExpansion Analysis of Offshore PipelineSAUGAT DUTTAОценок пока нет

- Ardipithecus Ramidus Is A Hominin Species Dating To Between 4.5 and 4.2 Million Years AgoДокумент5 страницArdipithecus Ramidus Is A Hominin Species Dating To Between 4.5 and 4.2 Million Years AgoBianca IrimieОценок пока нет

- Detailed Lesson Plan in Science 10Документ7 страницDetailed Lesson Plan in Science 10Glen MillarОценок пока нет

- Aviation Case StudyДокумент6 страницAviation Case Studynabil sayedОценок пока нет

- AP Biology 1st Semester Final Exam Review-2011.2012Документ13 страницAP Biology 1st Semester Final Exam Review-2011.2012Jessica ShinОценок пока нет

- Rak Single DentureДокумент48 страницRak Single Denturerakes0Оценок пока нет

- Fs Casas FinalДокумент55 страницFs Casas FinalGwen Araña BalgomaОценок пока нет

- Analyzing Evidence of College Readiness: A Tri-Level Empirical & Conceptual FrameworkДокумент66 страницAnalyzing Evidence of College Readiness: A Tri-Level Empirical & Conceptual FrameworkJinky RegonayОценок пока нет

- Midterms and Finals Topics for Statistics at University of the CordillerasДокумент2 страницыMidterms and Finals Topics for Statistics at University of the Cordillerasjohny BraveОценок пока нет

- ECON 121 Principles of MacroeconomicsДокумент3 страницыECON 121 Principles of MacroeconomicssaadianaveedОценок пока нет

- Earth-Song WorksheetДокумент2 страницыEarth-Song WorksheetMuhammad FarizОценок пока нет

- DU - BSC (H) CS BookletДокумент121 страницаDU - BSC (H) CS BookletNagendra DuhanОценок пока нет

- 14 - Habeas Corpus PetitionДокумент4 страницы14 - Habeas Corpus PetitionJalaj AgarwalОценок пока нет

- Shore Activities and Detachments Under The Command of Secretary of Navy and Chief of Naval OperationsДокумент53 страницыShore Activities and Detachments Under The Command of Secretary of Navy and Chief of Naval OperationskarakogluОценок пока нет

- Letter of Reccommendation For LuisaДокумент3 страницыLetter of Reccommendation For Luisaapi-243184335Оценок пока нет

- SampleДокумент4 страницыSampleParrallathanОценок пока нет

- De Broglie's Hypothesis: Wave-Particle DualityДокумент4 страницыDe Broglie's Hypothesis: Wave-Particle DualityAvinash Singh PatelОценок пока нет

- Dmat ReportДокумент130 страницDmat ReportparasarawgiОценок пока нет

- Court Testimony-WpsДокумент3 страницыCourt Testimony-WpsCrisanto HernandezОценок пока нет

- Class 11 English Snapshots Chapter 1Документ2 страницыClass 11 English Snapshots Chapter 1Harsh彡Eagle彡Оценок пока нет

- CV Jan 2015 SДокумент4 страницыCV Jan 2015 Sapi-276142935Оценок пока нет

- Photojournale - Connections Across A Human PlanetДокумент75 страницPhotojournale - Connections Across A Human PlanetjohnhorniblowОценок пока нет

- Assignment OUMH1203 English For Written Communication September 2023 SemesterДокумент15 страницAssignment OUMH1203 English For Written Communication September 2023 SemesterFaiz MufarОценок пока нет

- Multiple Choice Test - 66253Документ2 страницыMultiple Choice Test - 66253mvjОценок пока нет

- Module 1 Ba Core 11 LessonsДокумент37 страницModule 1 Ba Core 11 LessonsLolita AlbaОценок пока нет

- Sakolsky Ron Seizing AirwavesДокумент219 страницSakolsky Ron Seizing AirwavesPalin WonОценок пока нет

- Awareness Training On Filipino Sign Language (FSL) PDFДокумент3 страницыAwareness Training On Filipino Sign Language (FSL) PDFEmerito PerezОценок пока нет

- Senator Frank R Lautenberg 003Документ356 страницSenator Frank R Lautenberg 003Joey WilliamsОценок пока нет

- All Projects Should Be Typed On A4 SheetsДокумент3 страницыAll Projects Should Be Typed On A4 SheetsNikita AgrawalОценок пока нет