Вам также может понравиться

- Estimation of Values & Residual 1 AprilДокумент14 страницEstimation of Values & Residual 1 AprilKathryn CottonОценок пока нет

- Explanation For The Notification On Escalation Factors and Other Parameters, Dated 7.4.2015Документ12 страницExplanation For The Notification On Escalation Factors and Other Parameters, Dated 7.4.2015spgkumar7733Оценок пока нет

- 2012-Motaleb Monowara CompositeДокумент3 страницы2012-Motaleb Monowara CompositeShahadat Hossain ShahinОценок пока нет

- Village Road Bridge bid schedule and construction detailsДокумент24 страницыVillage Road Bridge bid schedule and construction detailsmuhammad iqbalОценок пока нет

- Supply and Delivery of Electrical Spare PartsДокумент1 страницаSupply and Delivery of Electrical Spare PartsJaapar HassanОценок пока нет

- Region VIII - Eastern Visayas Quickstat On: Philippine Statistics AuthorityДокумент3 страницыRegion VIII - Eastern Visayas Quickstat On: Philippine Statistics AuthorityBegie LucenecioОценок пока нет

- 88) Goldline Defence TowerДокумент3 страницы88) Goldline Defence ToweraliОценок пока нет

- Project Name: Provision of Potable Water System Location: Brgy. Arado, Dulag, Leyte Itemi: Tap Stand 1) 20 UnitsДокумент14 страницProject Name: Provision of Potable Water System Location: Brgy. Arado, Dulag, Leyte Itemi: Tap Stand 1) 20 UnitsCarlo Basinang CapiliОценок пока нет

- The Arton East Tower Price List As of July 28, 2023Документ3 страницыThe Arton East Tower Price List As of July 28, 2023Lean MeilyОценок пока нет

- Quickstat - Region 11 June 2018Документ5 страницQuickstat - Region 11 June 2018Kyle EscalaОценок пока нет

- Cost analysis of mining operationsДокумент3 страницыCost analysis of mining operationsRatmokoAdiNugrohoОценок пока нет

- Home SalesДокумент1 страницаHome Salesgayle8961Оценок пока нет

- 2019 SDDOT Bid Item Price Report SummaryДокумент31 страница2019 SDDOT Bid Item Price Report SummaryEddy Mustafa JalilОценок пока нет

- LAKEHOLMZ (1,000 TO 1,600SQFT) : Project Information LocationДокумент26 страницLAKEHOLMZ (1,000 TO 1,600SQFT) : Project Information LocationSGYong14Оценок пока нет

- Gaur City Centre Shop Category and Price ListДокумент2 страницыGaur City Centre Shop Category and Price ListNitin AgnihotriОценок пока нет

- Quickstat - Region 04a March 2018Документ5 страницQuickstat - Region 04a March 2018caratnotcarrotОценок пока нет

- Region X - Northern Mindanao Quickstat On: As of June 2018Документ6 страницRegion X - Northern Mindanao Quickstat On: As of June 2018Joebell VillanuevaОценок пока нет

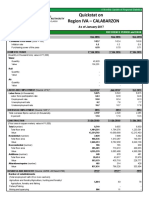

- Regional Statistics Update for CALABARZON RegionДокумент3 страницыRegional Statistics Update for CALABARZON RegionmojokinsОценок пока нет

- 2012-Shah FatehullahДокумент3 страницы2012-Shah FatehullahShahadat Hossain ShahinОценок пока нет

- 1 BR - All Seasons Terrace Apartments - Damac Hills - Golf Terrace - Inr 2.99 CR - ReadyДокумент4 страницы1 BR - All Seasons Terrace Apartments - Damac Hills - Golf Terrace - Inr 2.99 CR - ReadyFahad Farooq FareedОценок пока нет

- CBT - Steel Plate (New)Документ5 страницCBT - Steel Plate (New)ArviansОценок пока нет

- Dahab Tower Apartments Payment PlanДокумент3 страницыDahab Tower Apartments Payment PlanLexico InternationalОценок пока нет

- NEW APP Format RA 11469Документ6 страницNEW APP Format RA 11469marineljunepalerОценок пока нет

- Biaya Investasi Unit Pendaftaran Rekam Medis: No. Nama Alat Tahun Beli Satuan Harga Satuan Jumlah BarangДокумент12 страницBiaya Investasi Unit Pendaftaran Rekam Medis: No. Nama Alat Tahun Beli Satuan Harga Satuan Jumlah BarangSholikhatin Eka PrasetiaОценок пока нет

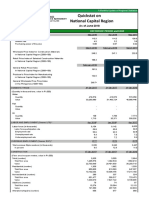

- Regional Statistics Update: NCR June 2018Документ5 страницRegional Statistics Update: NCR June 2018LiaОценок пока нет

- Variation 02Документ7 страницVariation 02Lakmal JayashanthaОценок пока нет

- Invoice Kates 1 - 2Документ2 страницыInvoice Kates 1 - 2Ahmat Safa'atОценок пока нет

- Sensitive Price Indicator (SPI)Документ22 страницыSensitive Price Indicator (SPI)Mian Kaashif ImranОценок пока нет

- Contract Cost Estimate Variation Form FirmДокумент4 страницыContract Cost Estimate Variation Form Firmsaneeltandan1Оценок пока нет

- Presentation On Road ProjectДокумент13 страницPresentation On Road ProjectKhan EngrОценок пока нет

- Certified IPC No. 31Документ28 страницCertified IPC No. 31John AlexОценок пока нет

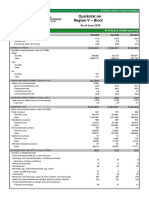

- Region V - Bicol Quickstat On: As of June 2018Документ3 страницыRegion V - Bicol Quickstat On: As of June 2018Jessica VasquezОценок пока нет

- BIAYA INVESTASI UNIT PENYIMPANAN OBATДокумент15 страницBIAYA INVESTASI UNIT PENYIMPANAN OBATSholikhatin Eka PrasetiaОценок пока нет

- Studio - All Seasons Terrace Apartments - Damac Hills - Loreto - Inr 1.51 CR - ReadyДокумент4 страницыStudio - All Seasons Terrace Apartments - Damac Hills - Loreto - Inr 1.51 CR - ReadyFahad Farooq FareedОценок пока нет

- Part IV Price Bid 220kv Rahiyad SuvaДокумент51 страницаPart IV Price Bid 220kv Rahiyad SuvaramОценок пока нет

- SV 2.0 Price List - Payment PlanДокумент5 страницSV 2.0 Price List - Payment PlanRahul MalikОценок пока нет

- Concrete Paving Project in Maasin CityДокумент11 страницConcrete Paving Project in Maasin CityPEOIROW SOLEYTEОценок пока нет

- Standard Costing and Variance Analysis (8304)Документ14 страницStandard Costing and Variance Analysis (8304)Rachel FuentesОценок пока нет

- Bond and Stock Valuation: Lembar Jawaban Lab 4 IpmДокумент4 страницыBond and Stock Valuation: Lembar Jawaban Lab 4 IpmIcal PahleviОценок пока нет

- Blossomvale TransactionДокумент14 страницBlossomvale TransactionSGYong14Оценок пока нет

- Amount (RS) : Nadirabad Flyover Multan Bill No - 1Документ3 страницыAmount (RS) : Nadirabad Flyover Multan Bill No - 1naveed ahmedОценок пока нет

- S10 18Документ7 страницS10 18Kapil DalviОценок пока нет

- Dupa. 1Документ90 страницDupa. 1Jus TineОценок пока нет

- TheReserve JeffCrossing BR OM Feb24Документ36 страницTheReserve JeffCrossing BR OM Feb24samobtiaОценок пока нет

- PT Dharma Henwa Dayworks Sheet Resume for Culverts InstallationДокумент6 страницPT Dharma Henwa Dayworks Sheet Resume for Culverts Installationmufqi fauzi100% (1)

- Kannipayoor Rou CompensationДокумент4 страницыKannipayoor Rou CompensationsebincherianОценок пока нет

- Voyage Costs ProjectДокумент32 страницыVoyage Costs ProjectAndra PurcareaОценок пока нет

- MS Welding ElectrodesДокумент7 страницMS Welding Electrodesmkpasha55mpОценок пока нет

- Budgeting & Plan Produksi 2020 NCIДокумент54 страницыBudgeting & Plan Produksi 2020 NCIArief SusantoОценок пока нет

- Ahs PersiapanДокумент6 страницAhs PersiapanMohamad Khaerun Zuhry RadjilunОценок пока нет

- CCE - PLATE 1 46 - Aguillon Araneta and MatratarДокумент48 страницCCE - PLATE 1 46 - Aguillon Araneta and MatratarIndependence CuradaОценок пока нет

- Invoice KMFДокумент1 страницаInvoice KMFhusen123 alhusadaОценок пока нет

- Prospero-Ville 1597715836 PDFДокумент7 страницProspero-Ville 1597715836 PDFSGYong14Оценок пока нет

- Combined For Mining Machines Rev. 1Документ7 страницCombined For Mining Machines Rev. 1mkpasha55mpОценок пока нет

- Sales SummaryДокумент12 страницSales SummarySATYANARAYANA MOTAMARRIОценок пока нет

- Lecture 2-Economics D-SДокумент34 страницыLecture 2-Economics D-Szahra naheedОценок пока нет

- VO Acad WaterproofingДокумент2 страницыVO Acad WaterproofingEldrianne Louie OponОценок пока нет

- Cópia de 20201216 - Preços ECE95Документ5 страницCópia de 20201216 - Preços ECE95Paulo BarbozaОценок пока нет

- Region XII Quickstat Monthly UpdateДокумент5 страницRegion XII Quickstat Monthly UpdateArra Carlyne Soberano CasadorОценок пока нет

- Understand Supply & Demand with this Guide to Key Real Estate PrinciplesДокумент8 страницUnderstand Supply & Demand with this Guide to Key Real Estate PrinciplesKathryn CottonОценок пока нет

- Paraphrasing and Summarising Sem 2 2014 - 15Документ14 страницParaphrasing and Summarising Sem 2 2014 - 15Kathryn CottonОценок пока нет

- Rred Compiled RemaДокумент12 страницRred Compiled RemaKathryn CottonОценок пока нет

- Online Grammar Exercise 14Документ6 страницOnline Grammar Exercise 14Kathryn CottonОценок пока нет

- TrafficДокумент1 страницаTrafficKathryn CottonОценок пока нет

- Text EditingДокумент1 страницаText EditingKathryn CottonОценок пока нет

- Online Grammar Exercise 8-EditedДокумент15 страницOnline Grammar Exercise 8-EditedKathryn CottonОценок пока нет

- 6 Key Factors With DescriptionДокумент15 страниц6 Key Factors With DescriptionKathryn CottonОценок пока нет

- Construction CostsДокумент8 страницConstruction CostsKathryn CottonОценок пока нет

- The Decided Is Has Argues Have Are: Activity Type I: Error IdentificationДокумент6 страницThe Decided Is Has Argues Have Are: Activity Type I: Error IdentificationKathryn CottonОценок пока нет

- Using Outlines & Graphic Organizers for Summarizing & Pre-WritingДокумент6 страницUsing Outlines & Graphic Organizers for Summarizing & Pre-WritingKathryn CottonОценок пока нет

- Using Outlines & Graphic Organizers for Summarizing & Pre-WritingДокумент6 страницUsing Outlines & Graphic Organizers for Summarizing & Pre-WritingKathryn CottonОценок пока нет

- TrafficДокумент1 страницаTrafficKathryn CottonОценок пока нет

- AuthEssay 2 TEXTДокумент2 страницыAuthEssay 2 TEXTKathryn CottonОценок пока нет

- 1104 t4 q3Документ12 страниц1104 t4 q3Kathryn CottonОценок пока нет

- RE1102 - Negative Impacts V2Документ5 страницRE1102 - Negative Impacts V2Kathryn CottonОценок пока нет

- A&D of Valuation MethodsДокумент1 страницаA&D of Valuation MethodsKathryn CottonОценок пока нет

- IntroductionДокумент1 страницаIntroductionKathryn CottonОценок пока нет

- A&D of Valuation MethodsДокумент1 страницаA&D of Valuation MethodsKathryn CottonОценок пока нет

- Koh de Ping ResumeДокумент2 страницыKoh de Ping ResumeKathryn CottonОценок пока нет

- AuthEssay 2 TEXTДокумент2 страницыAuthEssay 2 TEXTKathryn CottonОценок пока нет

- Wendy ResumeДокумент2 страницыWendy ResumeKathryn CottonОценок пока нет

- Yokogawa PID Tuning Guide - CsTunerДокумент28 страницYokogawa PID Tuning Guide - CsTunerZohaib Alam100% (2)

- M XXSRY2 Q Yk 8Документ1 страницаM XXSRY2 Q Yk 8Kathryn CottonОценок пока нет

- 3 Yd cEKoCkДокумент2 страницы3 Yd cEKoCkKathryn CottonОценок пока нет

- 3 Yd cEKoCkДокумент2 страницы3 Yd cEKoCkKathryn CottonОценок пока нет

- 3 Yd cEKoCkДокумент2 страницы3 Yd cEKoCkKathryn CottonОценок пока нет

- ZTT T6 PVRFX UДокумент2 страницыZTT T6 PVRFX UKathryn CottonОценок пока нет

- 3.1 Overview of Cell Line DevelopmentДокумент4 страницы3.1 Overview of Cell Line DevelopmentKathryn CottonОценок пока нет

- MGMT611 Managing Littlefield TechДокумент4 страницыMGMT611 Managing Littlefield Techqiyang84Оценок пока нет

- Assignment Next PLCДокумент16 страницAssignment Next PLCJames Jane50% (2)

- Chapter 4 Labor Demand ElasticityДокумент9 страницChapter 4 Labor Demand ElasticityMon CotacoОценок пока нет

- Operations Research Course Requirements and TopicsДокумент18 страницOperations Research Course Requirements and TopicsgotdlookzОценок пока нет

- Chapter 26 Introduction To Liabilities PDFДокумент16 страницChapter 26 Introduction To Liabilities PDFARIS100% (1)

- System LimitedДокумент11 страницSystem LimitedNabeel AhmadОценок пока нет

- Acknowledgement Fy 2020-21Документ1 страницаAcknowledgement Fy 2020-21Prajwal ShettyОценок пока нет

- HAFALAN AKUNTANSI HUMPB (HARTA UTANG MODAL PENDAPATAN BEBAN) (English)Документ3 страницыHAFALAN AKUNTANSI HUMPB (HARTA UTANG MODAL PENDAPATAN BEBAN) (English)Ilham SukronОценок пока нет

- Business FinanceДокумент30 страницBusiness FinanceCelina LimОценок пока нет

- ITC E-ChoupalДокумент23 страницыITC E-ChoupalRick Ganguly100% (1)

- Affidavit of Coporate Denial: Registered Mail#Документ2 страницыAffidavit of Coporate Denial: Registered Mail#roquemore1100% (2)

- Cost of Goods Sold Problems PDF 1 3Документ3 страницыCost of Goods Sold Problems PDF 1 3Janine padronesОценок пока нет

- 9.hilton 9E Global Edition Solutions Manual Chapter08 (Exercise+problem)Документ22 страницы9.hilton 9E Global Edition Solutions Manual Chapter08 (Exercise+problem)Anisa VrenoziОценок пока нет

- Deductions From Income From Other SourcesДокумент7 страницDeductions From Income From Other SourcesPADMANABHAN POTTIОценок пока нет

- Financial Management: 2002, Prentice Hall, IncДокумент31 страницаFinancial Management: 2002, Prentice Hall, IncMuhammad Zeeshan KhanОценок пока нет

- A Case Study of Reebok Acquisition by AdidasДокумент4 страницыA Case Study of Reebok Acquisition by AdidasIrtaza Zaidi0% (1)

- Chapter 3 Notes Full CompleteДокумент17 страницChapter 3 Notes Full CompleteTakreem AliОценок пока нет

- ARTO Bank Report: Development, Shareholders, DividendsДокумент3 страницыARTO Bank Report: Development, Shareholders, DividendsAfterneathОценок пока нет

- CPA Review School of the Philippines Final Pre-board ExaminationДокумент67 страницCPA Review School of the Philippines Final Pre-board ExaminationCykee Hanna Quizo Lumongsod100% (1)

- Combine PDF Dari TugasДокумент62 страницыCombine PDF Dari TugasAloysius Derry BenediktusОценок пока нет

- SERVICES of PTCL Pakistan Telecommunication Company Limited Not Only Provides Conventional Telephone Faciliti Services For Consumers These Services Are Basically For The Common UsersДокумент6 страницSERVICES of PTCL Pakistan Telecommunication Company Limited Not Only Provides Conventional Telephone Faciliti Services For Consumers These Services Are Basically For The Common UsersJunaid NoonariОценок пока нет

- Garrison12ce PPT Ch04Документ78 страницGarrison12ce PPT Ch04snsahaОценок пока нет

- 285 AA445 D 01Документ21 страница285 AA445 D 01tkkg854Оценок пока нет

- ACCT102 Standard CostingДокумент52 страницыACCT102 Standard CostingDonovan Leong 도노반0% (1)

- Strategic Audit For Transportation and Engineering Company For Tires (Trenco)Документ16 страницStrategic Audit For Transportation and Engineering Company For Tires (Trenco)Yousab KaldasОценок пока нет

- Abhishek Alloys PVT LTDДокумент18 страницAbhishek Alloys PVT LTDRajeshKolekarОценок пока нет

- RCM Expenses List Under GSTДокумент5 страницRCM Expenses List Under GSTAnonymous O3P3qkОценок пока нет

- SPCC Accounts Term 2 HomeworkДокумент2 страницыSPCC Accounts Term 2 HomeworkHarsh MishraОценок пока нет

- Sales Manager in Minneapolis ST Paul MN Resume Stacey BuzayДокумент2 страницыSales Manager in Minneapolis ST Paul MN Resume Stacey BuzayStaceyBuzayОценок пока нет

- Explaining Zambian Poverty: A History of Economic Policy Since IndependenceДокумент37 страницExplaining Zambian Poverty: A History of Economic Policy Since IndependenceChola Mukanga100% (3)

- Crossings: How Road Ecology Is Shaping the Future of Our PlanetОт EverandCrossings: How Road Ecology Is Shaping the Future of Our PlanetРейтинг: 4.5 из 5 звезд4.5/5 (10)

- A Place of My Own: The Architecture of DaydreamsОт EverandA Place of My Own: The Architecture of DaydreamsРейтинг: 4 из 5 звезд4/5 (241)

- The Things We Make: The Unknown History of Invention from Cathedrals to Soda CansОт EverandThe Things We Make: The Unknown History of Invention from Cathedrals to Soda CansОценок пока нет

- Pressure Vessels: Design, Formulas, Codes, and Interview Questions & Answers ExplainedОт EverandPressure Vessels: Design, Formulas, Codes, and Interview Questions & Answers ExplainedРейтинг: 5 из 5 звезд5/5 (1)

- To Engineer Is Human: The Role of Failure in Successful DesignОт EverandTo Engineer Is Human: The Role of Failure in Successful DesignРейтинг: 4 из 5 звезд4/5 (137)

- Piping and Pipeline Calculations Manual: Construction, Design Fabrication and ExaminationОт EverandPiping and Pipeline Calculations Manual: Construction, Design Fabrication and ExaminationРейтинг: 4 из 5 звезд4/5 (18)

- Building Construction Technology: A Useful Guide - Part 1От EverandBuilding Construction Technology: A Useful Guide - Part 1Рейтинг: 4 из 5 звезд4/5 (3)

- The Complete Guide to Alternative Home Building Materials & Methods: Including Sod, Compressed Earth, Plaster, Straw, Beer Cans, Bottles, Cordwood, and Many Other Low Cost MaterialsОт EverandThe Complete Guide to Alternative Home Building Materials & Methods: Including Sod, Compressed Earth, Plaster, Straw, Beer Cans, Bottles, Cordwood, and Many Other Low Cost MaterialsРейтинг: 4.5 из 5 звезд4.5/5 (6)

- An Architect's Guide to Construction: Tales from the Trenches Book 1От EverandAn Architect's Guide to Construction: Tales from the Trenches Book 1Оценок пока нет

- The Complete Guide to Building Your Own Home and Saving Thousands on Your New HouseОт EverandThe Complete Guide to Building Your Own Home and Saving Thousands on Your New HouseРейтинг: 5 из 5 звезд5/5 (3)

- How to Estimate with RSMeans Data: Basic Skills for Building ConstructionОт EverandHow to Estimate with RSMeans Data: Basic Skills for Building ConstructionРейтинг: 4.5 из 5 звезд4.5/5 (2)

- Engineering Critical Assessment (ECA) for Offshore Pipeline SystemsОт EverandEngineering Critical Assessment (ECA) for Offshore Pipeline SystemsОценок пока нет

- The Complete HVAC BIBLE for Beginners: The Most Practical & Updated Guide to Heating, Ventilation, and Air Conditioning Systems | Installation, Troubleshooting and Repair | Residential & CommercialОт EverandThe Complete HVAC BIBLE for Beginners: The Most Practical & Updated Guide to Heating, Ventilation, and Air Conditioning Systems | Installation, Troubleshooting and Repair | Residential & CommercialОценок пока нет

- Practical Guides to Testing and Commissioning of Mechanical, Electrical and Plumbing (Mep) InstallationsОт EverandPractical Guides to Testing and Commissioning of Mechanical, Electrical and Plumbing (Mep) InstallationsРейтинг: 3.5 из 5 звезд3.5/5 (3)

- The Great Bridge: The Epic Story of the Building of the Brooklyn BridgeОт EverandThe Great Bridge: The Epic Story of the Building of the Brooklyn BridgeРейтинг: 4.5 из 5 звезд4.5/5 (59)

- The Things We Make: The Unknown History of Invention from Cathedrals to Soda CansОт EverandThe Things We Make: The Unknown History of Invention from Cathedrals to Soda CansРейтинг: 4.5 из 5 звезд4.5/5 (21)

- Building Construction Technology: A Useful Guide - Part 2От EverandBuilding Construction Technology: A Useful Guide - Part 2Рейтинг: 5 из 5 звезд5/5 (1)

- Nuclear Energy in the 21st Century: World Nuclear University PressОт EverandNuclear Energy in the 21st Century: World Nuclear University PressРейтинг: 4.5 из 5 звезд4.5/5 (3)

- Methodology for Estimating Carbon Footprint of Road Projects: Case Study: IndiaОт EverandMethodology for Estimating Carbon Footprint of Road Projects: Case Study: IndiaОценок пока нет

- Civil Engineer's Handbook of Professional PracticeОт EverandCivil Engineer's Handbook of Professional PracticeРейтинг: 4.5 из 5 звезд4.5/5 (2)

- Field Guide for Construction Management: Management by Walking AroundОт EverandField Guide for Construction Management: Management by Walking AroundРейтинг: 4.5 из 5 звезд4.5/5 (3)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)