Вам также может понравиться

- Applied Corporate Finance. What is a Company worth?От EverandApplied Corporate Finance. What is a Company worth?Рейтинг: 3 из 5 звезд3/5 (2)

- Recall The Flows of Funds and Decisions Important To The Financial ManagerДокумент27 страницRecall The Flows of Funds and Decisions Important To The Financial ManagerAyaz MahmoodОценок пока нет

- Model Paper Business FinanceДокумент7 страницModel Paper Business FinanceMuhammad Tahir NawazОценок пока нет

- HW 6Документ2 страницыHW 6feenОценок пока нет

- CA IPCC Costing & FM Quick Revision NotesДокумент21 страницаCA IPCC Costing & FM Quick Revision NotesChandreshОценок пока нет

- Activity Based Costing in ABB Drives: Team MembersДокумент18 страницActivity Based Costing in ABB Drives: Team MembersGeorge BabuОценок пока нет

- Advanced Bond ConceptsДокумент8 страницAdvanced Bond ConceptsEllaine OlimberioОценок пока нет

- Principles of Microeconomics Production FunctionДокумент28 страницPrinciples of Microeconomics Production FunctionmqcpiqmsОценок пока нет

- Capital BudetingДокумент12 страницCapital BudetingChristian LimОценок пока нет

- Material ControlДокумент16 страницMaterial ControlbelladoОценок пока нет

- CAPM GuideДокумент15 страницCAPM GuideEnp Gus AgostoОценок пока нет

- Process Costing PresentationДокумент50 страницProcess Costing PresentationKhadija AlkebsiОценок пока нет

- Management Accounting-Nature and ScopeДокумент13 страницManagement Accounting-Nature and ScopePraveen SinghОценок пока нет

- Overhead ControlДокумент6 страницOverhead ControlbelladoОценок пока нет

- Overview of Comparative Financial SystemДокумент16 страницOverview of Comparative Financial Systemarafat alamОценок пока нет

- Job CostingДокумент11 страницJob Costingbellado0% (1)

- Consumer Behaviour: by Kirtish Bhavsar JanviДокумент7 страницConsumer Behaviour: by Kirtish Bhavsar Janvikirtissh bhavsaarОценок пока нет

- Introduction To Economics: Choices, Choices, Choices, - .Документ68 страницIntroduction To Economics: Choices, Choices, Choices, - .shahumang11Оценок пока нет

- Introduction To EconomicsДокумент88 страницIntroduction To EconomicsdoomОценок пока нет

- Chapter 6Документ3 страницыChapter 6Regine Gale UlnaganОценок пока нет

- Formation of A CompanyДокумент17 страницFormation of A CompanySyed Adnan Hussain ZaidiОценок пока нет

- Chapter 6 International Banking and Money Market 4017Документ23 страницыChapter 6 International Banking and Money Market 4017jdahiya_1Оценок пока нет

- Time Value of Money: - Presented byДокумент18 страницTime Value of Money: - Presented byMayuresh GanuОценок пока нет

- By: Anjali KulshresthaДокумент18 страницBy: Anjali KulshresthaAnjali KulshresthaОценок пока нет

- Prisoner DilemmaДокумент2 страницыPrisoner DilemmaRakhee ChatterjeeОценок пока нет

- Types Functions Financial InstitutionsДокумент27 страницTypes Functions Financial InstitutionsTarun MalhotraОценок пока нет

- Marginal CostingДокумент22 страницыMarginal CostingbelladoОценок пока нет

- Role or Importance of State Bank of Pakistan in Economic Development of PakistanДокумент3 страницыRole or Importance of State Bank of Pakistan in Economic Development of PakistanMohammad Hasan100% (1)

- Portfolio Selection Using Sharpe, Treynor & Jensen Performance IndexДокумент15 страницPortfolio Selection Using Sharpe, Treynor & Jensen Performance Indexktkalai selviОценок пока нет

- Game Theory: Abhishek Shukla Mba (It) IiitaДокумент21 страницаGame Theory: Abhishek Shukla Mba (It) IiitaAbhishek ShuklaОценок пока нет

- Cost Behavior AnalysisДокумент5 страницCost Behavior AnalysisMuhammad Umer Qureshi100% (1)

- Chapter Product NotesДокумент11 страницChapter Product NotesGoransh KhandelwalОценок пока нет

- CF B21 TVДокумент33 страницыCF B21 TVSoumya KhatuaОценок пока нет

- Chapter 11 - Cost of Capital - Text and End of Chapter QuestionsДокумент63 страницыChapter 11 - Cost of Capital - Text and End of Chapter QuestionsSaba Rajpoot50% (2)

- 3353 TVM Lecture 3Документ31 страница3353 TVM Lecture 3herueuxОценок пока нет

- Download the original attachment - The complete basics of accountingДокумент32 страницыDownload the original attachment - The complete basics of accountingvijayОценок пока нет

- Answers Exercises Chapter 4 and 5Документ10 страницAnswers Exercises Chapter 4 and 5Filipe FrancoОценок пока нет

- Ratio Analysis: R K MohantyДокумент30 страницRatio Analysis: R K Mohantybgowda_erp1438Оценок пока нет

- Financial MarketДокумент10 страницFinancial MarketLinganagouda PatilОценок пока нет

- Chapter 4 PDFДокумент50 страницChapter 4 PDFSyed Atiq TurabiОценок пока нет

- Ch14 Capital BudgetingДокумент16 страницCh14 Capital BudgetingYentl Rose Bico RomeroОценок пока нет

- Accounting Training OverviewДокумент74 страницыAccounting Training Overviewzee_iitОценок пока нет

- Standard Costs and Variance AnalysisДокумент37 страницStandard Costs and Variance Analysisromelover79152Оценок пока нет

- Chapter 4 Risk and ReturnДокумент19 страницChapter 4 Risk and Returnvaghela_jitendra8Оценок пока нет

- Capital Asset Pricing Model and Modern Portfolio TheoryДокумент12 страницCapital Asset Pricing Model and Modern Portfolio TheorylordaiztrandОценок пока нет

- Lesson - 17 Production FunctionДокумент6 страницLesson - 17 Production FunctionDurga DeviОценок пока нет

- Chapter 4 DerivativesДокумент38 страницChapter 4 DerivativesTamrat KindeОценок пока нет

- JOINT STOCK COMPANY CHARACTERISTICSДокумент40 страницJOINT STOCK COMPANY CHARACTERISTICSarun447Оценок пока нет

- Twelve: Monopolistic Competition: The Competitive Model in A More Realistic SettingДокумент21 страницаTwelve: Monopolistic Competition: The Competitive Model in A More Realistic SettingAmit BhattacherjiОценок пока нет

- FE 445 M1 CheatsheetДокумент5 страницFE 445 M1 Cheatsheetsaya1990Оценок пока нет

- Chap 8 SolutionsДокумент8 страницChap 8 SolutionsMiftahudin MiftahudinОценок пока нет

- Chapter - 5 Capital BudgetingДокумент9 страницChapter - 5 Capital BudgetingShuvro RahmanОценок пока нет

- A Comparison of Capital Budgeting Techniques: With Definitions and ExemplificationsДокумент36 страницA Comparison of Capital Budgeting Techniques: With Definitions and Exemplificationsahmad_ranjhaОценок пока нет

- Chapter 9 Net Present Value and Other Investment Criteria: Use The Following Information To Answer Questions 1 Through 5Документ12 страницChapter 9 Net Present Value and Other Investment Criteria: Use The Following Information To Answer Questions 1 Through 5Tuấn HoàngОценок пока нет

- IM Chapter 6 and 7Документ48 страницIM Chapter 6 and 7Kasahun MekonnenОценок пока нет

- Review For Midterm (Project Mana) 102021Документ37 страницReview For Midterm (Project Mana) 102021Tam MinhОценок пока нет

- UNIT - 4-2 - Gursamey....Документ27 страницUNIT - 4-2 - Gursamey....demeketeme2013Оценок пока нет

- NPV, IRR, and Investment Criteria AnalysisДокумент24 страницыNPV, IRR, and Investment Criteria AnalysisJehan OsamaОценок пока нет

- CH 6Документ29 страницCH 6Kasahun MekonnenОценок пока нет

- Net Present Value and Other Investment Criteria: Solutions To Questions and ProblemsДокумент4 страницыNet Present Value and Other Investment Criteria: Solutions To Questions and Problemsabraha gebruОценок пока нет

- Chapter5 - Elasticities of Demand and SupplyДокумент36 страницChapter5 - Elasticities of Demand and SupplyAnasChihabОценок пока нет

- Practice Questions Week 5 Day 1 and 2 Multiple ChoiceДокумент16 страницPractice Questions Week 5 Day 1 and 2 Multiple ChoiceAnasChihabОценок пока нет

- Ch01final9ed FinalДокумент35 страницCh01final9ed FinalAnasChihabОценок пока нет

- Barringer E5 PPT 09Документ26 страницBarringer E5 PPT 09AnasChihabОценок пока нет

- Capital Budgeting Techniques ComparisonДокумент30 страницCapital Budgeting Techniques ComparisonAnasChihabОценок пока нет

- IPPTChap 008Документ92 страницыIPPTChap 008AnasChihabОценок пока нет

- Standard Costs and VariancesДокумент65 страницStandard Costs and VariancesAnasChihabОценок пока нет

- Feasibility IronyourClothes FeedbackДокумент12 страницFeasibility IronyourClothes FeedbackAnasChihabОценок пока нет

- IPPTCh 005Документ97 страницIPPTCh 005AnasChihabОценок пока нет

- IPPTChap 008Документ92 страницыIPPTChap 008AnasChihabОценок пока нет

- Speee CHДокумент1 страницаSpeee CHAnasChihabОценок пока нет

- Buisness in MoroccoДокумент2 страницыBuisness in MoroccoAnasChihabОценок пока нет

- The Rise of Divorce: Explaining the Main CausesДокумент4 страницыThe Rise of Divorce: Explaining the Main CausesAnasChihabОценок пока нет

- Mock Assignment 4 - C Programming/Functions and Pointers Exercise 1Документ2 страницыMock Assignment 4 - C Programming/Functions and Pointers Exercise 1AnasChihabОценок пока нет

- Anas Chihab Rajae Driouich Ismail ElmahdiДокумент5 страницAnas Chihab Rajae Driouich Ismail ElmahdiAnasChihabОценок пока нет

- Annual Report Project On Muthoot Finance LTDДокумент39 страницAnnual Report Project On Muthoot Finance LTDAnu ArjaОценок пока нет

- Stock Research Report For UNH As of 7/27/11 - Chaikin Power ToolsДокумент4 страницыStock Research Report For UNH As of 7/27/11 - Chaikin Power ToolsChaikin Analytics, LLCОценок пока нет

- Capital Structure UploadДокумент17 страницCapital Structure UploadLakshmi Harshitha mОценок пока нет

- Fundamentals of Corporate Finance 3rd Edition Berk Test BankДокумент39 страницFundamentals of Corporate Finance 3rd Edition Berk Test Bankpalproedpm7t100% (15)

- Cost of Capital Capital Structure Dividend ProblemsДокумент26 страницCost of Capital Capital Structure Dividend Problemssalehin19690% (1)

- Cash and Cash Equivalents: Purchased Three Months Before MaturityДокумент8 страницCash and Cash Equivalents: Purchased Three Months Before MaturityMary Lyn DatuinОценок пока нет

- BetterSystemTrader UltimateGuideToTradingBooksДокумент180 страницBetterSystemTrader UltimateGuideToTradingBooksSebastianCalle90% (10)

- Ibm FinancialsДокумент132 страницыIbm Financialsphgiang1506Оценок пока нет

- Account Statement: Folio Number: 1017949588Документ2 страницыAccount Statement: Folio Number: 1017949588Z Limtsukiu Khiungrü YimchungerОценок пока нет

- CH2SOLUTIONS-AnswersProblemSetsДокумент4 страницыCH2SOLUTIONS-AnswersProblemSetsandreaskarayian8972100% (4)

- Horizontal Groups (2021)Документ5 страницHorizontal Groups (2021)Tawanda Tatenda HerbertОценок пока нет

- Test Bank For Horngrens Financial Managerial Accounting 4e by Nobles 0133359840Документ55 страницTest Bank For Horngrens Financial Managerial Accounting 4e by Nobles 0133359840JonathanHicksnrmo100% (36)

- Repurchase Agreements (Repos) : Concept, Mechanics and UsesДокумент5 страницRepurchase Agreements (Repos) : Concept, Mechanics and UsesManish KumarОценок пока нет

- Chapter 3Документ12 страницChapter 3Briggs Navarro BaguioОценок пока нет

- LT Foods Limited (DAAWAT - NS) - Long: Ritu Singh '22Документ2 страницыLT Foods Limited (DAAWAT - NS) - Long: Ritu Singh '22Sampann PatodiОценок пока нет

- World Co. Supply Chain Management AssignmentДокумент1 страницаWorld Co. Supply Chain Management AssignmentmirrorОценок пока нет

- Deluxe SolutionДокумент6 страницDeluxe SolutionR K Patham100% (1)

- OPM Inventory Balance Reconciliation DocumentДокумент6 страницOPM Inventory Balance Reconciliation DocumentKarthikeya BandaruОценок пока нет

- How To Read and Interpret Financial Statements - A Guide To Understanding What The Numbers Really MeanДокумент179 страницHow To Read and Interpret Financial Statements - A Guide To Understanding What The Numbers Really MeanMushahid Aly Khan100% (5)

- Turtle StrategyДокумент31 страницаTurtle StrategyJeniffer Rayen100% (3)

- Class No 14 & 15Документ31 страницаClass No 14 & 15WILD๛SHOTッ tanvirОценок пока нет

- CH 19Документ26 страницCH 19Samphors SengОценок пока нет

- Lot Traded Profit and Capital Table Shows Trading Strategy Over TimeДокумент14 страницLot Traded Profit and Capital Table Shows Trading Strategy Over TimeAmandeep SinghОценок пока нет

- Types Functions Financial InstitutionsДокумент27 страницTypes Functions Financial InstitutionsTarun MalhotraОценок пока нет

- PMBA PB6020 July2020 Cases Questions 23june2020Документ24 страницыPMBA PB6020 July2020 Cases Questions 23june2020Deepa GОценок пока нет

- Capital Structure Decision: An Overview: Kennedy Prince ModuguДокумент14 страницCapital Structure Decision: An Overview: Kennedy Prince ModuguChaitanya PrasadОценок пока нет

- Alibaba VIE Structure NotesДокумент3 страницыAlibaba VIE Structure NotesYujia JinОценок пока нет

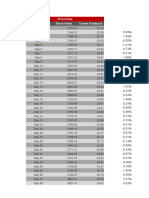

- Price Data Date Stock Index Turner FastbuckДокумент14 страницPrice Data Date Stock Index Turner FastbuckRampraveen ChamarthiОценок пока нет

- Multicap Fund - Four PagerДокумент4 страницыMulticap Fund - Four PagerSajid NavyОценок пока нет

- Best Intraday TipsДокумент4 страницыBest Intraday TipsGururaj VОценок пока нет