Вам также может понравиться

- Review For Exam 1Документ4 страницыReview For Exam 1Mahina NozirovaОценок пока нет

- First National Bank Balance Sheet Assets Liabilities $ Million $ MillionДокумент2 страницыFirst National Bank Balance Sheet Assets Liabilities $ Million $ MillionShameel IrshadОценок пока нет

- Commercial BankingДокумент10 страницCommercial BankingUsama HakeemОценок пока нет

- Liquidity RatiosДокумент1 страницаLiquidity RatiosRahul Girish KumarОценок пока нет

- Financial AnalysisДокумент31 страницаFinancial Analysiskashif aliОценок пока нет

- Academic Honor Code of HKUST: Homework Quiz #1 (10 Points)Документ6 страницAcademic Honor Code of HKUST: Homework Quiz #1 (10 Points)Oscar LamОценок пока нет

- Presentation On CGTMSE and Upcoming OpportunitiesДокумент16 страницPresentation On CGTMSE and Upcoming OpportunitiesAkshay JainОценок пока нет

- HDFC Ar 22Документ455 страницHDFC Ar 22Mohit SainiОценок пока нет

- Major AssignementДокумент9 страницMajor AssignementInzamam ul haqОценок пока нет

- Excel - B2 - Standard LP Problems - Revised September 28Документ21 страницаExcel - B2 - Standard LP Problems - Revised September 28francois mouawadОценок пока нет

- Amendment To Service Provider Agreement 1Документ3 страницыAmendment To Service Provider Agreement 1myloan partnerОценок пока нет

- QuestionsДокумент5 страницQuestionsdhitalkhushiОценок пока нет

- Interest Rate Risk ManagementДокумент15 страницInterest Rate Risk ManagementLiontiniОценок пока нет

- Current RatioДокумент13 страницCurrent RatioAnugya GuptaОценок пока нет

- Past Exam QuestionsДокумент8 страницPast Exam QuestionsKelvin ChenОценок пока нет

- Bodhi Tree Multimedia LimitedДокумент6 страницBodhi Tree Multimedia LimitedraftaarОценок пока нет

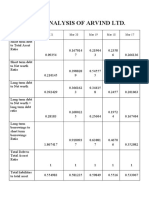

- Ratio Analysis of Arvind LTD.: Ratios Mar 21 Mar 20 Mar 19 Mar 18 Mar 17Документ10 страницRatio Analysis of Arvind LTD.: Ratios Mar 21 Mar 20 Mar 19 Mar 18 Mar 17simranОценок пока нет

- 7 Comparing Investments WorksheetsДокумент4 страницы7 Comparing Investments WorksheetsMuhammad Fajar Agna FernandyОценок пока нет

- Balance Sheet: StandaloneДокумент9 страницBalance Sheet: StandaloneKabita BuragohainОценок пока нет

- FM11 CH 10 Mini-Case Old13 Basics of Cap BudgДокумент20 страницFM11 CH 10 Mini-Case Old13 Basics of Cap BudgMZK videos100% (1)

- ADB Rate PDFДокумент1 страницаADB Rate PDFAlaul KarimОценок пока нет

- Finance Case 1Документ2 страницыFinance Case 1jessevanderendeОценок пока нет

- Credit Risk Management: Prof. Ashok ThampyДокумент55 страницCredit Risk Management: Prof. Ashok ThampyRohan JainОценок пока нет

- FRA練習Документ3 страницыFRA練習华邦盛Оценок пока нет

- Particulars Year 1 Year 2 Year 3Документ6 страницParticulars Year 1 Year 2 Year 3Kuljeet SinghОценок пока нет

- Angaben 28 PfandBG OEPF EN Q1 2022Документ3 страницыAngaben 28 PfandBG OEPF EN Q1 2022Franklin GutiérrezОценок пока нет

- F Sent To PRM 38 Q - A PRM 38 End Term Paper 7.9.17Документ9 страницF Sent To PRM 38 Q - A PRM 38 End Term Paper 7.9.17Parth PatilОценок пока нет

- Company Info - Print FinancialsДокумент2 страницыCompany Info - Print Financialsragaveyndhar maniОценок пока нет

- Credit and CommoditiesДокумент3 страницыCredit and CommoditiesSubG 08Оценок пока нет

- Case StudiesДокумент19 страницCase StudiesEthan DanielОценок пока нет

- Book 1Документ5 страницBook 1Sakulkeat PuechkuakulОценок пока нет

- Problem Set 3 (Duration II) With AnswersДокумент5 страницProblem Set 3 (Duration II) With Answerskenny013Оценок пока нет

- Solvency Position: 1. Debt-Equity RatioДокумент5 страницSolvency Position: 1. Debt-Equity RatioShilpiОценок пока нет

- Sovereign Loan PricingДокумент3 страницыSovereign Loan PricingWilliam LauОценок пока нет

- EX 1718 SolДокумент10 страницEX 1718 SolJoana SilvaОценок пока нет

- Praveen Sagar Project ReportДокумент12 страницPraveen Sagar Project Reportbhuvana uppalaОценок пока нет

- Ch15 Long Term Liabilities - PPSXДокумент40 страницCh15 Long Term Liabilities - PPSXRana PerryОценок пока нет

- 09 ch09 Mishkin Append1 PDFДокумент9 страниц09 ch09 Mishkin Append1 PDFfixa khalidОценок пока нет

- Can Central Banks Talk Too Much?Документ6 страницCan Central Banks Talk Too Much?TBP_Think_TankОценок пока нет

- Chapter 7 Math SolutionДокумент5 страницChapter 7 Math SolutionRakib AhmedОценок пока нет

- Balance Sheet ParleДокумент2 страницыBalance Sheet ParleDhruvi PatelОценок пока нет

- Questions, Anwers Chapter 22Документ3 страницыQuestions, Anwers Chapter 22basit111Оценок пока нет

- GIM - Revised Mid Term Paper - Solution and Marking PatternДокумент4 страницыGIM - Revised Mid Term Paper - Solution and Marking PatternNamitha ShajanОценок пока нет

- The Jammu & Kashmir Bank LTD: AccountДокумент5 страницThe Jammu & Kashmir Bank LTD: AccountĒxçlūsìvē SympãthētìçОценок пока нет

- Corporate Financial Management Assignment - Ratio Analysis of Hays PLCДокумент11 страницCorporate Financial Management Assignment - Ratio Analysis of Hays PLCAmany Hamza100% (1)

- Japan, India, Malaysia, Singapore, Thailand: Asian Bonds, Currency PreviewДокумент6 страницJapan, India, Malaysia, Singapore, Thailand: Asian Bonds, Currency PreviewMuzammil AzeemОценок пока нет

- Corporate RestructuringДокумент11 страницCorporate RestructuringFazul RehmanОценок пока нет

- FIN3009 Financial Management: Topic 5: Bonds and Bond ValuationДокумент72 страницыFIN3009 Financial Management: Topic 5: Bonds and Bond Valuationkc103038Оценок пока нет

- Pg1 3 MergedДокумент10 страницPg1 3 MergedAryan DhamechaОценок пока нет

- Schedule of Charges Revised 01052022Документ19 страницSchedule of Charges Revised 01052022Chandra MohanОценок пока нет

- Tute Solution - CHP 06Документ5 страницTute Solution - CHP 06Aryan KalyanОценок пока нет

- Bos 55636 Finalp 2 AДокумент13 страницBos 55636 Finalp 2 AVipul JainОценок пока нет

- 1.duration Question 2Документ9 страниц1.duration Question 2ShobhitОценок пока нет

- KMC Balance Sheet Stand Alone NewДокумент2 страницыKMC Balance Sheet Stand Alone NewOmkar GadeОценок пока нет

- Fixed Income MarketsДокумент2 страницыFixed Income Marketssaeed14820Оценок пока нет

- Mini Case 8 and 9 FixДокумент6 страницMini Case 8 and 9 FixAnisah Nur Imani100% (1)

- Housing Industry: Topic 1: Mortgage Industry in IndiaДокумент24 страницыHousing Industry: Topic 1: Mortgage Industry in Indiapankaj t pareekОценок пока нет

- Seminar Questions Set II-1Документ4 страницыSeminar Questions Set II-1fanuel kijojiОценок пока нет

- C-206 - FM - Prof R K Mishra - MT - 21-23 For ExamДокумент1 страницаC-206 - FM - Prof R K Mishra - MT - 21-23 For Examajit pandaОценок пока нет

- Finance AccountДокумент430 страницFinance AccountRaman YadavОценок пока нет

- PNOC Vs KeppelДокумент14 страницPNOC Vs KeppelGladys Bantilan0% (1)

- UCPB Home Loan Application Form PrintableДокумент2 страницыUCPB Home Loan Application Form PrintableKaren MalabananОценок пока нет

- RB Millionaire Roadmap Ebook v7-1Документ24 страницыRB Millionaire Roadmap Ebook v7-1Jam AmirОценок пока нет

- CAT CBT 19 With Detailed SolutionsДокумент30 страницCAT CBT 19 With Detailed SolutionsAnjali SharmaОценок пока нет

- 56 Metropol Vs SambokДокумент3 страницы56 Metropol Vs SambokCharm Divina LascotaОценок пока нет

- Financial Management Assignment: Cash Flow Analysis OF Kwality Dairy LTDДокумент4 страницыFinancial Management Assignment: Cash Flow Analysis OF Kwality Dairy LTDishant7890Оценок пока нет

- Indian Banking System Syllabus PDFДокумент2 страницыIndian Banking System Syllabus PDFMahek BaigОценок пока нет

- City Development PlanДокумент139 страницCity Development Planstolidness100% (1)

- Century Savings Bank Vs Sps SamonteДокумент8 страницCentury Savings Bank Vs Sps SamonteCE SherОценок пока нет

- Sajid ResumeДокумент5 страницSajid ResumeAzizleo2002Оценок пока нет

- 56c3fsylabus-Credit Appraisal and Project Financiang 2Документ2 страницы56c3fsylabus-Credit Appraisal and Project Financiang 2Ankit SinghalОценок пока нет

- S. Zug - Monga - Journal of Social StudiesДокумент14 страницS. Zug - Monga - Journal of Social StudiesrubenhechtОценок пока нет

- How To Make Money From Your Hobbies and IdeasДокумент85 страницHow To Make Money From Your Hobbies and Ideasapi-19739188100% (1)

- Attendee List For Aarmr 28th Annual RegulatoryДокумент26 страницAttendee List For Aarmr 28th Annual Regulatoryranjith123Оценок пока нет

- How To Stop ForeclosureДокумент391 страницаHow To Stop Foreclosuresirach2006883586% (7)

- Nikitas Spiros Koutsoukis Spyridon Roukanas Auth. Anastasios Karasavvoglou Persefoni Polychronidou Eds. Economic Crisis in Europe and The Balkans Problems and ProsДокумент245 страницNikitas Spiros Koutsoukis Spyridon Roukanas Auth. Anastasios Karasavvoglou Persefoni Polychronidou Eds. Economic Crisis in Europe and The Balkans Problems and ProsSydneyОценок пока нет

- Business Plan For Fisheries Processing and ExportingДокумент58 страницBusiness Plan For Fisheries Processing and ExportingCarina-Ioana Paraschiv83% (6)

- Lecture No5 - Equal-Payment - Series-ModifiedДокумент13 страницLecture No5 - Equal-Payment - Series-Modifiedpoqwuradfo apdsoaafОценок пока нет

- Internship Report On Faysal Bank LimitedДокумент48 страницInternship Report On Faysal Bank Limitedbbaahmad89100% (2)

- Management Accounting ScriptДокумент5 страницManagement Accounting ScriptGlenn G.Оценок пока нет

- Auditing Standards and Practices Council: Philippine Auditing Practice Statement 1000 Inter-Bank Confirmation ProceduresДокумент12 страницAuditing Standards and Practices Council: Philippine Auditing Practice Statement 1000 Inter-Bank Confirmation ProceduresnikОценок пока нет

- A Benchmark of Machine Learning Approaches For Credit Score PredictionДокумент8 страницA Benchmark of Machine Learning Approaches For Credit Score PredictionCorporacion H21Оценок пока нет

- Newpin Information MemorandumДокумент52 страницыNewpin Information MemorandumJp GdОценок пока нет

- HSa 1 GK AqlДокумент25 страницHSa 1 GK AqlTanmay KaperОценок пока нет

- ACCFA v. Alpha IncДокумент5 страницACCFA v. Alpha IncAnonymous nYvtSgoQОценок пока нет

- 9 Secrecy of Bank Deposits LawДокумент3 страницы9 Secrecy of Bank Deposits LawKelvin CulajaráОценок пока нет

- Evaluation of Mobile Banking Operation of Dutch Bangla Bank LimitedДокумент72 страницыEvaluation of Mobile Banking Operation of Dutch Bangla Bank LimitedSaydur Rahman Sayeed100% (7)

- Banking Law NotesДокумент9 страницBanking Law NotesAfiqah Ismail100% (2)

- Malolos Clark Railway Project - Framework Financing Agreement 1 PDFДокумент22 страницыMalolos Clark Railway Project - Framework Financing Agreement 1 PDFDeniell Joyce MarquezОценок пока нет