Вам также может понравиться

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5783)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Key economic concepts and terms explainedДокумент2 страницыKey economic concepts and terms explainedAdam EssamОценок пока нет

- Chapter Three Financial Markets in The Financial System: 3.1 Organization and Structure of MarketsДокумент7 страницChapter Three Financial Markets in The Financial System: 3.1 Organization and Structure of MarketsSeid KassawОценок пока нет

- SBI Credit Card StudyДокумент68 страницSBI Credit Card StudyGirish KumarОценок пока нет

- Wealthcon India Issue 7 Highlights Financial TopicsДокумент112 страницWealthcon India Issue 7 Highlights Financial TopicsAmol WaghmareОценок пока нет

- CW 13 LTF Key 1Документ6 страницCW 13 LTF Key 1Jedidiah ManglicmotОценок пока нет

- GIRO CIT Appln FormДокумент2 страницыGIRO CIT Appln FormHarith IskandarОценок пока нет

- REY DANIEL S. ACEDILLO Midterm Exam Credit TransactionsДокумент4 страницыREY DANIEL S. ACEDILLO Midterm Exam Credit TransactionsÝel ÄcedilloОценок пока нет

- Bangladesh Bank: Financial Stability DepartmentДокумент165 страницBangladesh Bank: Financial Stability DepartmentAsif NawazОценок пока нет

- MONEY, BANKING, AND MONETARY POLICY: UNDERSTANDING THE US FINANCIAL SYSTEMДокумент9 страницMONEY, BANKING, AND MONETARY POLICY: UNDERSTANDING THE US FINANCIAL SYSTEMKamalpreetОценок пока нет

- FFM 9 Im 13Документ15 страницFFM 9 Im 13Ernest NyangiОценок пока нет

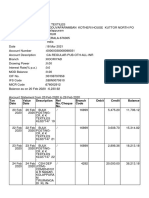

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceДокумент4 страницыTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceJaseem MonuОценок пока нет

- Pocket Catechism On The ConstitutionДокумент114 страницPocket Catechism On The ConstitutionTerry MilesОценок пока нет

- Negotiable Instruments - Case DigestДокумент73 страницыNegotiable Instruments - Case Digestjuan dela cruzОценок пока нет

- As-22 Accounting For Taxes On Income - Brief NoteДокумент5 страницAs-22 Accounting For Taxes On Income - Brief NoteKaran KhatriОценок пока нет

- The Evolution of Credit and Money SystemsДокумент4 страницыThe Evolution of Credit and Money SystemsChantelle IshiОценок пока нет

- Ias 16Документ31 страницаIas 16Reever RiverОценок пока нет

- Grade 10 Provincial Case Study MG 2023Документ3 страницыGrade 10 Provincial Case Study MG 2023kwazy dlaminiОценок пока нет

- Kotak - TSK GarmentsДокумент4 страницыKotak - TSK GarmentsVishnukumar KumarОценок пока нет

- Detailed Solutions To Problem 5Документ3 страницыDetailed Solutions To Problem 5Maria AngelicaОценок пока нет

- Cigi Membership Form 2022Документ1 страницаCigi Membership Form 2022Uday MongaОценок пока нет

- Background of The StudyДокумент2 страницыBackground of The StudyAdonis GaoiranОценок пока нет

- Exercise4 Adjusting 1Документ4 страницыExercise4 Adjusting 1ABIGAIL DAYOTОценок пока нет

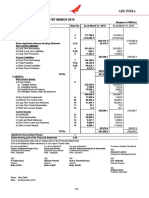

- Balance Sheet As at 31st March 2015Документ1 страницаBalance Sheet As at 31st March 2015Mrigul UppalОценок пока нет

- Financial Statement 2014Документ9 страницFinancial Statement 2014shahid2opuОценок пока нет

- 1Q13 Restructuring Advisory ReviewДокумент5 страниц1Q13 Restructuring Advisory ReviewAshish KrishnaОценок пока нет

- Capital Budgeting Chapter ReviewДокумент27 страницCapital Budgeting Chapter Reviewcindysia000Оценок пока нет

- BOI TPA Legal VettedДокумент6 страницBOI TPA Legal VettedAbhishek BarwalОценок пока нет

- Contracts Project 3rd TremДокумент17 страницContracts Project 3rd TremYashwant ManothiyaОценок пока нет

- Financial Inclusion Through India Post: Dr. Joji Chandran PHDДокумент4 страницыFinancial Inclusion Through India Post: Dr. Joji Chandran PHDJoji ChandranОценок пока нет

- Anderton SICAV Launches New High Income Investment Fund. Gamma Capital Markets Acts As Investment Manager.Документ5 страницAnderton SICAV Launches New High Income Investment Fund. Gamma Capital Markets Acts As Investment Manager.PR.comОценок пока нет