Вам также может понравиться

- Eclectica Absolute Macro Fund: Manager CommentДокумент3 страницыEclectica Absolute Macro Fund: Manager Commentfreemind3682Оценок пока нет

- Inflation Rates: The Cost of LivingДокумент6 страницInflation Rates: The Cost of LivingAnonymous QKHeLscy2kОценок пока нет

- Indian Stock Market AnalysisДокумент36 страницIndian Stock Market AnalysisTushar GangolyОценок пока нет

- Outlook For The SMSF SectorДокумент13 страницOutlook For The SMSF SectorRomeoОценок пока нет

- Jan-12 Sep-13 Jun-13 Mar-13 Jan-13 Sep-14 Jun-14 Mar-14 Dec-14 Sep-15 Jun-15 Mar-15 Dec-13 Oct-16 Jun-16 Mar-17 Jan-18 Jun-18 Dec-18 YearДокумент4 страницыJan-12 Sep-13 Jun-13 Mar-13 Jan-13 Sep-14 Jun-14 Mar-14 Dec-14 Sep-15 Jun-15 Mar-15 Dec-13 Oct-16 Jun-16 Mar-17 Jan-18 Jun-18 Dec-18 YearsyedОценок пока нет

- MEF Analysis UI Claims - March 2020Документ2 страницыMEF Analysis UI Claims - March 2020Dave AllenОценок пока нет

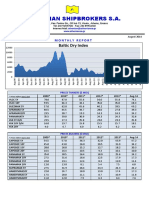

- Athenian Shipbrokers S.A.: Baltic Dry IndexДокумент17 страницAthenian Shipbrokers S.A.: Baltic Dry IndexgeorgevarsasОценок пока нет

- Athenian Shipbrokers - Monthy Report - 14.08.15Документ17 страницAthenian Shipbrokers - Monthy Report - 14.08.15georgevarsasОценок пока нет

- Atalonia The Difficult Path Towards Independence: Sebastian D. Baglioni Carleton University March 11, 2015Документ16 страницAtalonia The Difficult Path Towards Independence: Sebastian D. Baglioni Carleton University March 11, 2015Haeshan NiyarepolaОценок пока нет

- Building Speech Recognition Systems With The Kaldi Toolkit PDFДокумент121 страницаBuilding Speech Recognition Systems With The Kaldi Toolkit PDFLe Gia Anh QuyОценок пока нет

- Al Ahli Bank of Kuwait - Egypt - MMF - November 2017 - English - Monthly ReportДокумент1 страницаAl Ahli Bank of Kuwait - Egypt - MMF - November 2017 - English - Monthly ReportSobolОценок пока нет

- Tracking Financial ConditionsДокумент14 страницTracking Financial ConditionsSathishОценок пока нет

- Athenian-Shipbrokers-April 2013Документ18 страницAthenian-Shipbrokers-April 2013Nguyen Le Thu HaОценок пока нет

- TAKAFUL IKHLAS March - 2020 - EngДокумент6 страницTAKAFUL IKHLAS March - 2020 - EngEncik ArifОценок пока нет

- SageOne Investor Memo May 2018Документ10 страницSageOne Investor Memo May 2018Akhil ParekhОценок пока нет

- Loan E.M.I. Calculator: Data To EnterДокумент10 страницLoan E.M.I. Calculator: Data To EnterNanjunda SwamyОценок пока нет

- 2015 Priorities of Energy Policy of Japan Under AbenomicsДокумент14 страниц2015 Priorities of Energy Policy of Japan Under AbenomicsHằng ĐặngОценок пока нет

- Copyright and The Evolving Learning Materials Market - Campus Stores CanadaДокумент6 страницCopyright and The Evolving Learning Materials Market - Campus Stores CanadaAn Michael Powell100% (2)

- On The Treadmill: Young and Long-Term: Unemployed in AustraliaДокумент3 страницыOn The Treadmill: Young and Long-Term: Unemployed in Australia90x93 -Оценок пока нет

- Presentation FY2014Документ26 страницPresentation FY2014Vlad KremerОценок пока нет

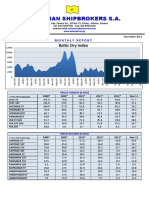

- Athenian Shipbrokers - Monthy Report - 13.11.15 PDFДокумент20 страницAthenian Shipbrokers - Monthy Report - 13.11.15 PDFgeorgevarsas0% (1)

- November 2019 Monthly Housing Market OutlookДокумент47 страницNovember 2019 Monthly Housing Market OutlookC.A.R. Research & EconomicsОценок пока нет

- Turkiye 2023 Elections Three Economic ScenariosДокумент22 страницыTurkiye 2023 Elections Three Economic ScenariosBaran SakallıoğluОценок пока нет

- InflationДокумент42 страницыInflationTwinkle MehtaОценок пока нет

- 2017 08 16 - ID Finance Presentation PDFДокумент12 страниц2017 08 16 - ID Finance Presentation PDFJuan Daniel Garcia VeigaОценок пока нет

- Athenian-Shipbrokers-July 2013Документ18 страницAthenian-Shipbrokers-July 2013Nguyen Le Thu HaОценок пока нет

- 2019-06 Monthly Housing Market OutlookДокумент39 страниц2019-06 Monthly Housing Market OutlookC.A.R. Research & EconomicsОценок пока нет

- 17 Total BD: MMM Total Break DownДокумент2 страницы17 Total BD: MMM Total Break DownVIBHORОценок пока нет

- 2019-10 Monthly Housing Market OutlookДокумент44 страницы2019-10 Monthly Housing Market OutlookC.A.R. Research & EconomicsОценок пока нет

- Athenian-Shipbrokers-May 2016Документ17 страницAthenian-Shipbrokers-May 2016Nguyen Le Thu HaОценок пока нет

- APRAS 60 S/D 72 BLN 12 S/D 59 BN (Balita) : Umur Pelaksanaan DDTK Puskesmas Pasir Belengkong Tahun 2018Документ4 страницыAPRAS 60 S/D 72 BLN 12 S/D 59 BN (Balita) : Umur Pelaksanaan DDTK Puskesmas Pasir Belengkong Tahun 2018MeitiAriantiОценок пока нет

- Protocolo de Bioseguridad (Toma de Temperatura) Empleados DÍA Tempe DÍA Tempe DÍA Tempe DÍA Tempe DÍA Tempe DÍA TempeДокумент1 страницаProtocolo de Bioseguridad (Toma de Temperatura) Empleados DÍA Tempe DÍA Tempe DÍA Tempe DÍA Tempe DÍA Tempe DÍA TempeCOMPRAS MVM LTDAОценок пока нет

- 2019-02 Monthly Housing Market OutlookДокумент28 страниц2019-02 Monthly Housing Market OutlookC.A.R. Research & Economics0% (1)

- Month-To-Month Volatility ShortДокумент4 страницыMonth-To-Month Volatility ShortAgnes PoppyОценок пока нет

- Parte 2Документ34 страницыParte 2Odla Sedlej OcopihcОценок пока нет

- 4.4 The Role of International TradeДокумент5 страниц4.4 The Role of International TradeMingyu LiangОценок пока нет

- Exchange Rate ForecastДокумент5 страницExchange Rate ForecastLaxmana Rao ParimiОценок пока нет

- 2019-09 Monthly Housing Market OutlookДокумент44 страницы2019-09 Monthly Housing Market OutlookC.A.R. Research & EconomicsОценок пока нет

- South Korean Energy Outlook 2015Документ13 страницSouth Korean Energy Outlook 2015Afifa KamilaОценок пока нет

- Potential Inflationary PressuresДокумент5 страницPotential Inflationary PressuresKamran BayramovОценок пока нет

- Control de Aceros 1301Документ16 страницControl de Aceros 1301rullitsОценок пока нет

- How To Create A Simple Run ChartДокумент2 страницыHow To Create A Simple Run ChartWage qualityОценок пока нет

- Monthly Fund Performance Update Aia International Small Cap FundДокумент1 страницаMonthly Fund Performance Update Aia International Small Cap FundLam Kah MengОценок пока нет

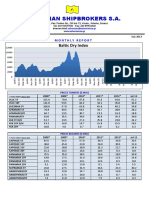

- Athenian Shipbrokers - Monthy Report - 14.07.15 PDFДокумент18 страницAthenian Shipbrokers - Monthy Report - 14.07.15 PDFgeorgevarsasОценок пока нет

- Athenian-Shipbrokers-March 2013Документ19 страницAthenian-Shipbrokers-March 2013Nguyen Le Thu HaОценок пока нет

- 2014 Deepa Puthran Forecasting Global Turbocharger Market A Mixed Method ApproachДокумент5 страниц2014 Deepa Puthran Forecasting Global Turbocharger Market A Mixed Method ApproachShiv PrasadОценок пока нет

- Aagbs Research Briefing 20204 - Mba - Mibf (07112020)Документ7 страницAagbs Research Briefing 20204 - Mba - Mibf (07112020)AKMALОценок пока нет

- Time Sheet - Janaury2018 ShahidДокумент56 страницTime Sheet - Janaury2018 ShahidJunaidОценок пока нет

- Torrent Downloaded From ExtraTorrent - CCДокумент6 страницTorrent Downloaded From ExtraTorrent - CCAhmed Ali HefnawyОценок пока нет

- 95 - Emerging India Portfolio-March2019 - Final Email VersionДокумент22 страницы95 - Emerging India Portfolio-March2019 - Final Email VersionTarunAnandaniОценок пока нет

- 2021-02 Monthly Housing Market OutlookДокумент29 страниц2021-02 Monthly Housing Market OutlookC.A.R. Research & EconomicsОценок пока нет

- Evolucion Del Indice de Solvencia Establecimientos de Credito December 2020Документ10 страницEvolucion Del Indice de Solvencia Establecimientos de Credito December 2020Laura GarcesОценок пока нет

- Research Speak - 16-04-2010Документ12 страницResearch Speak - 16-04-2010A_KinshukОценок пока нет

- Update On IDFC Arbitrage FundДокумент6 страницUpdate On IDFC Arbitrage FundGОценок пока нет

- VolatilityFriendOrFoeДокумент18 страницVolatilityFriendOrFoejacekОценок пока нет

- Picture Last Name First Name, Middle Name 1X1 Student Number Contact NumberДокумент2 страницыPicture Last Name First Name, Middle Name 1X1 Student Number Contact NumberRobert CondeОценок пока нет

- Atk - Accelerating Into Uncertainty PREEZДокумент25 страницAtk - Accelerating Into Uncertainty PREEZAndrey PritulyukОценок пока нет

- % Fisico Planejado: % Fisico Planejado Acum % Fisico Real % Fisico Real AcumДокумент4 страницы% Fisico Planejado: % Fisico Planejado Acum % Fisico Real % Fisico Real AcumMiquéias AlcântaraОценок пока нет

- Global Cement Magazine Nov 2017 PDFДокумент70 страницGlobal Cement Magazine Nov 2017 PDFPavala Ayyanar100% (1)

- ISD CodesДокумент4 страницыISD CodesMusaddique Ahmed100% (7)

- Inspection Procedures For Evaluation of ESPДокумент153 страницыInspection Procedures For Evaluation of ESPPavala AyyanarОценок пока нет

- ISO 4628engДокумент4 страницыISO 4628engLuisArmandoFranyuttiArciaОценок пока нет

- Icesp 09 A21 PDFДокумент12 страницIcesp 09 A21 PDFPavala AyyanarОценок пока нет

- Icesp 09 A21 PDFДокумент12 страницIcesp 09 A21 PDFPavala AyyanarОценок пока нет

- TPSeiffert 100Документ8 страницTPSeiffert 100Pavala AyyanarОценок пока нет

- Injection System Brochure PDFДокумент9 страницInjection System Brochure PDFPavala AyyanarОценок пока нет

- ISO 4628engДокумент4 страницыISO 4628engLuisArmandoFranyuttiArciaОценок пока нет

- ChemSet Crack Injection BrochureДокумент12 страницChemSet Crack Injection BrochurePavala AyyanarОценок пока нет

- ESP BrochureДокумент10 страницESP BrochureyukselenturkОценок пока нет

- BV34442446 PDFДокумент5 страницBV34442446 PDFPavala AyyanarОценок пока нет

- Accelerometers by Texas InstrumentsДокумент20 страницAccelerometers by Texas InstrumentsSergio GonzalezОценок пока нет

- 10 DesignДокумент7 страниц10 DesignPavala AyyanarОценок пока нет

- QUOTATION HO-20-17309 - Eulogio Amang Rodriguez Institute of Science and TechnologyДокумент1 страницаQUOTATION HO-20-17309 - Eulogio Amang Rodriguez Institute of Science and TechnologyVir Gel DiamanteОценок пока нет

- Comprehensive Illustrative ProblemДокумент2 страницыComprehensive Illustrative ProblemLyssa Marie Avenido GuelosОценок пока нет

- Cheminformatic Institute of Science Studies Lucknow: Tele:-0522 - 430 64 64 Mob: 09554064000, 09559196700Документ1 страницаCheminformatic Institute of Science Studies Lucknow: Tele:-0522 - 430 64 64 Mob: 09554064000, 09559196700dmannewarОценок пока нет

- Banking Laws Zarah PDFДокумент17 страницBanking Laws Zarah PDFMarcelino CasilОценок пока нет

- Feb 2017 Lists For PublicationsДокумент40 страницFeb 2017 Lists For Publicationspsiziba670287% (15)

- Chapter 4Документ5 страницChapter 4Angelica PagaduanОценок пока нет

- Loan Approval Letter (1) - 1Документ5 страницLoan Approval Letter (1) - 1selamoОценок пока нет

- Hi Cement Vs InsularДокумент1 страницаHi Cement Vs InsularTenet ManzanoОценок пока нет

- Axis Bank - Final.Документ55 страницAxis Bank - Final.TEJASHVINI PATELОценок пока нет

- PC 2013 06Документ15 страницPC 2013 06BruegelОценок пока нет

- Module 5 BankingДокумент42 страницыModule 5 Bankingg.prasanna saiОценок пока нет

- Federal Bank: Dividend Discount Valuation: The Indian Banking SystemДокумент10 страницFederal Bank: Dividend Discount Valuation: The Indian Banking SystemSyed GhouseОценок пока нет

- BAICC2X-Solution Supplementary - Week 1docxДокумент7 страницBAICC2X-Solution Supplementary - Week 1docxMitchie FaustinoОценок пока нет

- BC Details UK DistrictДокумент3 страницыBC Details UK DistrictNisa ArunОценок пока нет

- Stable ActДокумент18 страницStable ActMichaelPatrickMcSweeney50% (2)

- Negotiable Instruments Act 1881Документ20 страницNegotiable Instruments Act 1881Ankit Tiwari100% (1)

- Account Statement From 1 May 2021 To 16 Aug 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceДокумент10 страницAccount Statement From 1 May 2021 To 16 Aug 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceLoan LoanОценок пока нет

- Jawaban Soal UTBKДокумент5 страницJawaban Soal UTBKSyafira AdzkiaОценок пока нет

- 1 This First Bank: Sample Account Statement and BalancingДокумент2 страницы1 This First Bank: Sample Account Statement and BalancingAida Bracken100% (1)

- Credit AppraisalДокумент14 страницCredit AppraisalRishabh Jain0% (1)

- Invoice NoДокумент2 страницыInvoice Nodhiec100% (1)

- Mid Term Test - 01: Principles of AccountingДокумент2 страницыMid Term Test - 01: Principles of AccountingAn TuanОценок пока нет

- Forward RatesДокумент2 страницыForward RatesTiso Blackstar GroupОценок пока нет

- I - Functions of MoneyДокумент38 страницI - Functions of MoneyVISHVESH JUNEJAОценок пока нет

- Alt - Bank Company Brief PDFДокумент1 страницаAlt - Bank Company Brief PDFBruno MottaОценок пока нет

- International Finance Class Assignment 1Документ2 страницыInternational Finance Class Assignment 1AakashОценок пока нет

- Sbi 8853 Dec 23 RecoДокумент9 страницSbi 8853 Dec 23 RecoShivam pandeyОценок пока нет

- Finance Current Affairs March RevisionДокумент47 страницFinance Current Affairs March RevisionRte FrthОценок пока нет

- Article AssgnmentДокумент27 страницArticle AssgnmentNurul NadiaОценок пока нет

- All About CASHДокумент18 страницAll About CASHAshley Levy San Pedro100% (1)

- Financial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassОт EverandFinancial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassОценок пока нет

- A History of the United States in Five Crashes: Stock Market Meltdowns That Defined a NationОт EverandA History of the United States in Five Crashes: Stock Market Meltdowns That Defined a NationРейтинг: 4 из 5 звезд4/5 (11)

- Look Again: The Power of Noticing What Was Always ThereОт EverandLook Again: The Power of Noticing What Was Always ThereРейтинг: 5 из 5 звезд5/5 (3)

- The War Below: Lithium, Copper, and the Global Battle to Power Our LivesОт EverandThe War Below: Lithium, Copper, and the Global Battle to Power Our LivesРейтинг: 4.5 из 5 звезд4.5/5 (8)

- The Trillion-Dollar Conspiracy: How the New World Order, Man-Made Diseases, and Zombie Banks Are Destroying AmericaОт EverandThe Trillion-Dollar Conspiracy: How the New World Order, Man-Made Diseases, and Zombie Banks Are Destroying AmericaОценок пока нет

- The Infinite Machine: How an Army of Crypto-Hackers Is Building the Next Internet with EthereumОт EverandThe Infinite Machine: How an Army of Crypto-Hackers Is Building the Next Internet with EthereumРейтинг: 3 из 5 звезд3/5 (12)

- Vulture Capitalism: Corporate Crimes, Backdoor Bailouts, and the Death of FreedomОт EverandVulture Capitalism: Corporate Crimes, Backdoor Bailouts, and the Death of FreedomОценок пока нет

- This Changes Everything: Capitalism vs. The ClimateОт EverandThis Changes Everything: Capitalism vs. The ClimateРейтинг: 4 из 5 звезд4/5 (349)

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingОт EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingРейтинг: 4.5 из 5 звезд4.5/5 (97)

- Chip War: The Quest to Dominate the World's Most Critical TechnologyОт EverandChip War: The Quest to Dominate the World's Most Critical TechnologyРейтинг: 4.5 из 5 звезд4.5/5 (227)

- Narrative Economics: How Stories Go Viral and Drive Major Economic EventsОт EverandNarrative Economics: How Stories Go Viral and Drive Major Economic EventsРейтинг: 4.5 из 5 звезд4.5/5 (94)

- Nudge: The Final Edition: Improving Decisions About Money, Health, And The EnvironmentОт EverandNudge: The Final Edition: Improving Decisions About Money, Health, And The EnvironmentРейтинг: 4.5 из 5 звезд4.5/5 (92)

- Principles for Dealing with the Changing World Order: Why Nations Succeed or FailОт EverandPrinciples for Dealing with the Changing World Order: Why Nations Succeed or FailРейтинг: 4.5 из 5 звезд4.5/5 (237)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaОт EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaРейтинг: 4.5 из 5 звезд4.5/5 (14)

- The Technology Trap: Capital, Labor, and Power in the Age of AutomationОт EverandThe Technology Trap: Capital, Labor, and Power in the Age of AutomationРейтинг: 4.5 из 5 звезд4.5/5 (46)

- The Meth Lunches: Food and Longing in an American CityОт EverandThe Meth Lunches: Food and Longing in an American CityРейтинг: 5 из 5 звезд5/5 (5)

- The Myth of the Rational Market: A History of Risk, Reward, and Delusion on Wall StreetОт EverandThe Myth of the Rational Market: A History of Risk, Reward, and Delusion on Wall StreetОценок пока нет

- Economics 101: From Consumer Behavior to Competitive Markets—Everything You Need to Know About EconomicsОт EverandEconomics 101: From Consumer Behavior to Competitive Markets—Everything You Need to Know About EconomicsРейтинг: 5 из 5 звезд5/5 (3)

- Poor Economics: A Radical Rethinking of the Way to Fight Global PovertyОт EverandPoor Economics: A Radical Rethinking of the Way to Fight Global PovertyРейтинг: 4.5 из 5 звезд4.5/5 (263)