Вам также может понравиться

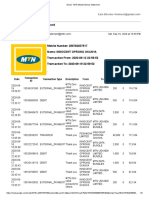

- Gmail - MTN Mobile Money Statement PDFДокумент3 страницыGmail - MTN Mobile Money Statement PDFokanyaОценок пока нет

- Hexaware Letter of Offer PDFДокумент68 страницHexaware Letter of Offer PDFJohnsonОценок пока нет

- Foreign Provisional Permenant RegistrationДокумент11 страницForeign Provisional Permenant RegistrationTina ThomsonОценок пока нет

- Employee Provident Fund: Presentation OnДокумент19 страницEmployee Provident Fund: Presentation OnTracey MorinОценок пока нет

- GM KPSC QCДокумент40 страницGM KPSC QCMahendra M100% (1)

- International Payments AssignmentДокумент13 страницInternational Payments AssignmentMuhammad Dilshad Ahmed AnsariОценок пока нет

- Travel Management Configuration StepsДокумент40 страницTravel Management Configuration Stepsusasidhar100% (1)

- T24 Account Group Parameters R16 PDFДокумент117 страницT24 Account Group Parameters R16 PDFadyani_0997100% (1)

- New Balance: Minimum Payment Due: Payment Due Date:: Account Activity Account Member Make Checks Payable ToДокумент5 страницNew Balance: Minimum Payment Due: Payment Due Date:: Account Activity Account Member Make Checks Payable ToScott HeatwoleОценок пока нет

- Profit & Loss - PC ViewДокумент18 страницProfit & Loss - PC ViewKabir BhaiОценок пока нет

- CExcise Objective QuestionsДокумент34 страницыCExcise Objective QuestionsParvathi Devi Varanasi0% (1)

- Central ExciseДокумент22 страницыCentral ExcisesadathnooriОценок пока нет

- Central Excise Short NotesДокумент27 страницCentral Excise Short Notestoprascal0% (1)

- GST Summary by Cma Tharun RajДокумент122 страницыGST Summary by Cma Tharun Rajrock rollОценок пока нет

- Indian Polity IДокумент10 страницIndian Polity IVIVEK KUMARОценок пока нет

- Goods & Services Act FinalДокумент78 страницGoods & Services Act FinalParvesh AghiОценок пока нет

- EPFOДокумент29 страницEPFOPratham sharmaОценок пока нет

- Pik Pera PDF File 2020 2021 1Документ1 страницаPik Pera PDF File 2020 2021 1Dadarao GavandeОценок пока нет

- Electrobeam MachiningДокумент8 страницElectrobeam Machiningpatel ketan67% (3)

- CCS - LTC Rules - 1988Документ37 страницCCS - LTC Rules - 1988Kranthi Kumar KunaОценок пока нет

- BCom Income Tax Procedure and PracticeДокумент61 страницаBCom Income Tax Procedure and PracticeUjjwal KandhaweОценок пока нет

- No - CE/T&S/NSK/GAD/Depttl - Exam./2236 Date: 22.12.2009 Sub: Syllabus of All Departmental Examinations .Документ19 страницNo - CE/T&S/NSK/GAD/Depttl - Exam./2236 Date: 22.12.2009 Sub: Syllabus of All Departmental Examinations .kbl11794100% (1)

- Ssc-Je: General Intelligence & ReasoningДокумент20 страницSsc-Je: General Intelligence & ReasoningAkhilОценок пока нет

- A Big Collection of GK With 2500 MCQДокумент120 страницA Big Collection of GK With 2500 MCQJuriani Avinash100% (2)

- Geography Through Ncert Questions UnlockedДокумент43 страницыGeography Through Ncert Questions UnlockedVivek JhaОценок пока нет

- The Building Other Construction Workers Act 1996Документ51 страницаThe Building Other Construction Workers Act 1996Anindyadeb BasuОценок пока нет

- EPFO - Latest InitiativesДокумент40 страницEPFO - Latest Initiativestusharujadhav5655Оценок пока нет

- 9 Month Planing For Capf ExamДокумент9 страниц9 Month Planing For Capf Examdeepesh0% (1)

- CE Act, 1944 MCQsДокумент35 страницCE Act, 1944 MCQs'Aakash Yadav'Оценок пока нет

- ANNUAL REPORT 2010 - 2011 Kirloskar Oil Engines LimitedДокумент76 страницANNUAL REPORT 2010 - 2011 Kirloskar Oil Engines LimitedParshu KalalОценок пока нет

- Panchayat RajДокумент318 страницPanchayat RajMohan Raj50% (2)

- Option Under para 11 (3) (Deleted) of The Eps, 1995Документ1 страницаOption Under para 11 (3) (Deleted) of The Eps, 1995Shiv Kumar100% (1)

- New Pik Pera Praman Patra Sowing CertificateДокумент1 страницаNew Pik Pera Praman Patra Sowing CertificateNikhil Kaware100% (1)

- Chargeble GSTДокумент87 страницChargeble GSTgopaljha84Оценок пока нет

- 40 Tax Audit in Tally Erp 9Документ15 страниц40 Tax Audit in Tally Erp 9Giri SukumarОценок пока нет

- General Awareness SyllabusДокумент5 страницGeneral Awareness SyllabusPrakhar tiwariОценок пока нет

- The Employees' Provident Funds and Miscellaneous Provisions Act, 1952Документ21 страницаThe Employees' Provident Funds and Miscellaneous Provisions Act, 1952Nabendu Karmakar100% (2)

- Building and Other Construction Workers Act 1996Документ151 страницаBuilding and Other Construction Workers Act 1996Rajesh KodavatiОценок пока нет

- Principles of Public Administration 2023Документ44 страницыPrinciples of Public Administration 2023Eve AthanasekouОценок пока нет

- 1565586071185130044Документ201 страница1565586071185130044Singer Saksham SharmaОценок пока нет

- Building and Other Construction Workers (Regulation of Employment and Conditions of Service) Act, 1996Документ7 страницBuilding and Other Construction Workers (Regulation of Employment and Conditions of Service) Act, 1996Latest Laws TeamОценок пока нет

- The Building and Other Construction Workers Regulation of Employment and Conditions of Service Act 1996 PDFДокумент29 страницThe Building and Other Construction Workers Regulation of Employment and Conditions of Service Act 1996 PDFApoorv Nagpal100% (1)

- SSC JE Youth 24 Reasoning PyqsДокумент624 страницыSSC JE Youth 24 Reasoning PyqsAnkitОценок пока нет

- BENEFITS - Pension SchemeДокумент9 страницBENEFITS - Pension SchemeajaygaekwadОценок пока нет

- Chapter 11 MCQs On Set Off and Carry Forward of LossessДокумент10 страницChapter 11 MCQs On Set Off and Carry Forward of LossessKaushar AlamОценок пока нет

- Eps 1995Документ3 страницыEps 1995PkaggarwalОценок пока нет

- (Batch:PCB1) Mrunal's Economy Pillar#2D: Budget Disinvestment & Deficits Page 280Документ27 страниц(Batch:PCB1) Mrunal's Economy Pillar#2D: Budget Disinvestment & Deficits Page 280Akshaykumar KeriОценок пока нет

- Epf - Faq What Is EPF?Документ13 страницEpf - Faq What Is EPF?siddhuemailsОценок пока нет

- Social Security For EPFO Exam: Powered byДокумент18 страницSocial Security For EPFO Exam: Powered byNirula SinghОценок пока нет

- Handbook On Exempted Supplies Under GSTДокумент205 страницHandbook On Exempted Supplies Under GSTkaaryafacilitiesОценок пока нет

- Handbook Labour TNДокумент120 страницHandbook Labour TNspshettyОценок пока нет

- Ur Obc SC ST Total: Minimum Level of Suitability of Marks For Written TestДокумент6 страницUr Obc SC ST Total: Minimum Level of Suitability of Marks For Written TestAbhishek GuptaОценок пока нет

- Ebook Pyp SSC PolityДокумент13 страницEbook Pyp SSC PolitymarxianbybirthОценок пока нет

- Kerala PWA CodeДокумент444 страницыKerala PWA CodeHIVETECHОценок пока нет

- Constitution and PolityДокумент356 страницConstitution and PolityAnurag KumarОценок пока нет

- Food Corporation of India Institute of Food Security Gurgaon Phase-A Objective Test: Personnel Management Batch /2010Документ6 страницFood Corporation of India Institute of Food Security Gurgaon Phase-A Objective Test: Personnel Management Batch /2010Swarup MukherjeeОценок пока нет

- Census of India (E) .pdf-60 PDFДокумент7 страницCensus of India (E) .pdf-60 PDFAbhishek GauravОценок пока нет

- Sequential Steps Covering A Departmental InquiryДокумент4 страницыSequential Steps Covering A Departmental Inquiryrishi_sam30Оценок пока нет

- Science Awareness For UpscДокумент196 страницScience Awareness For Upscrishi29Оценок пока нет

- GST - SurajДокумент167 страницGST - SurajSanjitha ParanthamanОценок пока нет

- Audit Manual For SASДокумент304 страницыAudit Manual For SASVivekDinkerОценок пока нет

- Co-Operative Movement in Karnataka UpdatedДокумент18 страницCo-Operative Movement in Karnataka UpdatedSagargn SagarОценок пока нет

- DIRECT TAX Finalold p7Документ5 страницDIRECT TAX Finalold p7VIHARI DОценок пока нет

- Central Excise Rules 2002Документ14 страницCentral Excise Rules 2002Amitabha Sankar BhaduriОценок пока нет

- The Central Excise Rules, 2002Документ30 страницThe Central Excise Rules, 2002mnarasimhacharyОценок пока нет

- CX Rules 2002Документ12 страницCX Rules 2002jessyshahОценок пока нет

- Bank Reconciliation Exercises and Answers: Step-By-Step Tutorial ExerciseДокумент20 страницBank Reconciliation Exercises and Answers: Step-By-Step Tutorial ExerciseTạ Tuấn DũngОценок пока нет

- Mark) : Signature Over Printed Name Date - Signature Over Printed Name DateДокумент3 страницыMark) : Signature Over Printed Name Date - Signature Over Printed Name DateAldwin UnisanОценок пока нет

- Internship Report OnДокумент58 страницInternship Report OnMehedi HasanОценок пока нет

- Information - An Effective WayДокумент7 страницInformation - An Effective WayHoàng Thuỳ Trang NguyễnОценок пока нет

- Soal Latihan MYOBДокумент7 страницSoal Latihan MYOBWinaya LarasatiОценок пока нет

- TEST-8: Lesson 3 Monetary SystemДокумент26 страницTEST-8: Lesson 3 Monetary SystemDeepak ShahОценок пока нет

- Presentation On PCS1x Application: by Kishore Golla Assistant Director (EDPДокумент15 страницPresentation On PCS1x Application: by Kishore Golla Assistant Director (EDPkishoregolla95677Оценок пока нет

- Hedging 1Документ28 страницHedging 1Sadaquat HusainОценок пока нет

- Find A Covering Letter To An Invoice (Enclosed A Sample of The Invoice)Документ9 страницFind A Covering Letter To An Invoice (Enclosed A Sample of The Invoice)danil psrОценок пока нет

- Commercial Banking in KenyaДокумент16 страницCommercial Banking in KenyaJared Opondo100% (6)

- Business Sample LettersДокумент3 страницыBusiness Sample Lettersshaikat1009549Оценок пока нет

- Business ModelsДокумент10 страницBusiness ModelschandusapreddyОценок пока нет

- Cheque Banks: Automated Clearing House (ACH)Документ2 страницыCheque Banks: Automated Clearing House (ACH)papson rukundoОценок пока нет

- Etc Lease BG - SBLC 22Документ32 страницыEtc Lease BG - SBLC 22Tonio EdevОценок пока нет

- Dynamics 365 Business Central Capability Guide - En-En - Final - v2Документ30 страницDynamics 365 Business Central Capability Guide - En-En - Final - v2Jesus CastroОценок пока нет

- Draft NCNDДокумент10 страницDraft NCNDDjarod Samuell0% (1)

- Related Party DisclosureДокумент2 страницыRelated Party DisclosureChristine Jane AbangОценок пока нет

- Customer Name Card Account No MR Ajay Kumar Das 4375 XXXX XXXX 9011Документ2 страницыCustomer Name Card Account No MR Ajay Kumar Das 4375 XXXX XXXX 9011Ajaykumar DasОценок пока нет

- CTI 2011 Application FormДокумент1 страницаCTI 2011 Application FormRnel L. YeeОценок пока нет

- ENBDДокумент1 страницаENBDpvr2k1Оценок пока нет

- FINANCIAL SHENANIGANS Kel 3Документ17 страницFINANCIAL SHENANIGANS Kel 3Qorry NittyОценок пока нет

- Appendix 11 Fee ScheduleДокумент10 страницAppendix 11 Fee ScheduleHamzaОценок пока нет

- Job Description - CashierДокумент2 страницыJob Description - CashierAlbert ManansalaОценок пока нет

- User Guide and TNC Canara Bank Debit CardДокумент16 страницUser Guide and TNC Canara Bank Debit Cardnitesh kumarОценок пока нет