Вам также может понравиться

- BBVA OpenMind Libro El Proximo Paso Vida Exponencial2Документ59 страницBBVA OpenMind Libro El Proximo Paso Vida Exponencial2giovanniОценок пока нет

- Summary of Bruce C. Greenwald, Judd Kahn & Paul D. Sonkin's Value InvestingОт EverandSummary of Bruce C. Greenwald, Judd Kahn & Paul D. Sonkin's Value InvestingОценок пока нет

- Capital Allocation - UpdatedДокумент73 страницыCapital Allocation - UpdatedGabriel LagesОценок пока нет

- The Executive Guide to Boosting Cash Flow and Shareholder Value: The Profit Pool ApproachОт EverandThe Executive Guide to Boosting Cash Flow and Shareholder Value: The Profit Pool ApproachОценок пока нет

- On Streaks: Perception, Probability, and SkillДокумент5 страницOn Streaks: Perception, Probability, and Skilljohnwang_174817Оценок пока нет

- The Art of Vulture Investing: Adventures in Distressed Securities ManagementОт EverandThe Art of Vulture Investing: Adventures in Distressed Securities ManagementОценок пока нет

- The Incredible Shrinking Universe of StocksДокумент29 страницThe Incredible Shrinking Universe of StocksErsin Seçkin100% (1)

- Financial Fine Print: Uncovering a Company's True ValueОт EverandFinancial Fine Print: Uncovering a Company's True ValueРейтинг: 3 из 5 звезд3/5 (3)

- A Piece of The Action - Employee Stock Options in The New EconomyДокумент45 страницA Piece of The Action - Employee Stock Options in The New Economypjs15Оценок пока нет

- Private Equity Unchained: Strategy Insights for the Institutional InvestorОт EverandPrivate Equity Unchained: Strategy Insights for the Institutional InvestorОценок пока нет

- Merits of CFROIДокумент7 страницMerits of CFROIfreemind3682Оценок пока нет

- Capital Structure and Profitability: S&P 500 Enterprises in the Light of the 2008 Financial CrisisОт EverandCapital Structure and Profitability: S&P 500 Enterprises in the Light of the 2008 Financial CrisisОценок пока нет

- Ubs - DCF PDFДокумент36 страницUbs - DCF PDFPaola VerdiОценок пока нет

- Alpha and The Paradox of Skill (MMauboussin - July '13)Документ12 страницAlpha and The Paradox of Skill (MMauboussin - July '13)Alexander LueОценок пока нет

- Curing Corporate Short-Termism: Future Growth vs. Current EarningsОт EverandCuring Corporate Short-Termism: Future Growth vs. Current EarningsОценок пока нет

- Capital Allocation Outside The U.SДокумент83 страницыCapital Allocation Outside The U.SSwapnil GorantiwarОценок пока нет

- Behind the Curve: An Analysis of the Investment Behavior of Private Equity FundsОт EverandBehind the Curve: An Analysis of the Investment Behavior of Private Equity FundsОценок пока нет

- Michael Mauboussin - Surge in The Urge To Merge, M&a Trends & Analysis 1-12-10Документ15 страницMichael Mauboussin - Surge in The Urge To Merge, M&a Trends & Analysis 1-12-10Phaedrus34Оценок пока нет

- PIPE Investments of Private Equity Funds: The temptation of public equity investments to private equity firmsОт EverandPIPE Investments of Private Equity Funds: The temptation of public equity investments to private equity firmsОценок пока нет

- Absolute Power - The Internet's Hidden OrderДокумент8 страницAbsolute Power - The Internet's Hidden Orderpjs15Оценок пока нет

- In Defense of Shareholder ValueДокумент11 страницIn Defense of Shareholder ValueJaime Andres Laverde ZuletaОценок пока нет

- Death, Taxes and Reversion To The Mean - ROIC StudyДокумент20 страницDeath, Taxes and Reversion To The Mean - ROIC Studypjs15Оценок пока нет

- Yacktman PresentationДокумент34 страницыYacktman PresentationVijay MalikОценок пока нет

- Mauboussin - Does The M&a Boom Mean Anything For The MarketДокумент6 страницMauboussin - Does The M&a Boom Mean Anything For The MarketRob72081Оценок пока нет

- Equities Crossing Barriers 09jun10Документ42 страницыEquities Crossing Barriers 09jun10Javier Holguera100% (1)

- Article - Mercer Capital Guide Option Pricing ModelДокумент18 страницArticle - Mercer Capital Guide Option Pricing ModelKshitij SharmaОценок пока нет

- Bill Ackman On What Makes A Great InvestmentДокумент5 страницBill Ackman On What Makes A Great InvestmentSww WisdomОценок пока нет

- The Fat Tail That Wags The Dog - Demystifying The Stock Market's PerformanceДокумент16 страницThe Fat Tail That Wags The Dog - Demystifying The Stock Market's Performancepjs15100% (1)

- Wolf Bytes 20: Equity Research-AmericasДокумент20 страницWolf Bytes 20: Equity Research-Americasvouzvouz7127Оценок пока нет

- The Real Role of DividendДокумент9 страницThe Real Role of DividendlenovojiОценок пока нет

- Michael Mauboussin - Seeking Portfolio Manager Skill 2-24-12Документ13 страницMichael Mauboussin - Seeking Portfolio Manager Skill 2-24-12Phaedrus34Оценок пока нет

- What Do We Need To FixДокумент10 страницWhat Do We Need To Fixkoyuri7Оценок пока нет

- Competitive Advantage PeriodДокумент6 страницCompetitive Advantage PeriodAndrija BabićОценок пока нет

- Freestyle Chess MauboussinДокумент10 страницFreestyle Chess MauboussinWilliam PetersenОценок пока нет

- 1995.12.13 - The More Things Change, The More They Stay The SameДокумент20 страниц1995.12.13 - The More Things Change, The More They Stay The SameYury PopovОценок пока нет

- Cashflow.comДокумент40 страницCashflow.comad9292Оценок пока нет

- Economic Returns, Reversion To The Mean, and Total Shareholder Returns Anticipating Change Is Hard But ProfitableДокумент15 страницEconomic Returns, Reversion To The Mean, and Total Shareholder Returns Anticipating Change Is Hard But ProfitableAhmed MadhaОценок пока нет

- One Job: Counterpoint Global InsightsДокумент25 страницOne Job: Counterpoint Global Insightscartigayan100% (1)

- Meausing A MoatДокумент73 страницыMeausing A MoatjesprileОценок пока нет

- Class Notes #2 Intro and Duff and Phelps Case StudyДокумент27 страницClass Notes #2 Intro and Duff and Phelps Case StudyJohn Aldridge Chew100% (1)

- Bottom-Up EV Calculation (Finatics)Документ5 страницBottom-Up EV Calculation (Finatics)Jessica KaryonoОценок пока нет

- BaupostДокумент20 страницBaupostapi-26094277Оценок пока нет

- Bin There Done That - Us PDFДокумент19 страницBin There Done That - Us PDFaaquibnasirОценок пока нет

- Let's Make A Deal - A Practical Framework For Assessing M&a ActivityДокумент26 страницLet's Make A Deal - A Practical Framework For Assessing M&a Activitypjs15100% (1)

- LPX 10K 2010 - Balance Sheet Case-StudyДокумент116 страницLPX 10K 2010 - Balance Sheet Case-StudyJohn Aldridge ChewОценок пока нет

- Dangers of DCF MortierДокумент12 страницDangers of DCF MortierKitti WongtuntakornОценок пока нет

- MS - Good Losses, Bad LossesДокумент13 страницMS - Good Losses, Bad LossesResearch ReportsОценок пока нет

- Fill and KillДокумент12 страницFill and Killad9292Оценок пока нет

- Still Powerful - The Internet's Hidden OrderДокумент17 страницStill Powerful - The Internet's Hidden Orderpjs15Оценок пока нет

- Valuing Growth Managing RiskДокумент35 страницValuing Growth Managing RiskJohn Aldridge Chew67% (3)

- Financial InfoДокумент23 страницыFinancial InfojohnsolarpanelsОценок пока нет

- How To Model Reversion To The Mean - Determining How Fast, and To What Mean, Results RevertДокумент26 страницHow To Model Reversion To The Mean - Determining How Fast, and To What Mean, Results Revertpjs15Оценок пока нет

- DB US Airlines PDFДокумент65 страницDB US Airlines PDFGeorge ShevtsovОценок пока нет

- DCF PrimerДокумент30 страницDCF PrimerAnkit_modi2000Оценок пока нет

- Li Lu's 2010 Lecture at Columbia My Previous Transcript View A More Recent LectureДокумент14 страницLi Lu's 2010 Lecture at Columbia My Previous Transcript View A More Recent Lecturepa_langstrom100% (1)

- Free Cash Flow Investing 04-18-11Документ6 страницFree Cash Flow Investing 04-18-11lowbankОценок пока нет

- Common DCF Errors - LeggMasonДокумент12 страницCommon DCF Errors - LeggMasonBob JonesОценок пока нет

- Creating Value Thru Best-In-class Capital AllocationДокумент16 страницCreating Value Thru Best-In-class Capital Allocationiltdf100% (1)

- PV PrimerДокумент15 страницPV Primerveda20Оценок пока нет

- End Game: Number of Firms Beta ROE Cost of Equity (Roe - Coe) BV of Equity Equity EVA ROCДокумент18 страницEnd Game: Number of Firms Beta ROE Cost of Equity (Roe - Coe) BV of Equity Equity EVA ROCCinthiaОценок пока нет

- RiskpracДокумент4 страницыRiskpracveda20Оценок пока нет

- End Game: Number of Firms Beta ROE Cost of Equity (Roe - Coe) BV of Equity Equity EVA ROCДокумент18 страницEnd Game: Number of Firms Beta ROE Cost of Equity (Roe - Coe) BV of Equity Equity EVA ROCCinthiaОценок пока нет

- DivginzuДокумент34 страницыDivginzuveda20Оценок пока нет

- End Game: Number of Firms Beta ROE Cost of Equity (Roe - Coe) BV of Equity Equity EVA ROCДокумент18 страницEnd Game: Number of Firms Beta ROE Cost of Equity (Roe - Coe) BV of Equity Equity EVA ROCCinthiaОценок пока нет

- Calculating Forward Rates: Practice ProblemsДокумент1 страницаCalculating Forward Rates: Practice Problemsveda20Оценок пока нет

- City BrochureДокумент16 страницCity Brochureveda20Оценок пока нет

- Primer StatsДокумент4 страницыPrimer Statsveda20Оценок пока нет

- Pamela Peterson Drake, James Madison UniversityДокумент4 страницыPamela Peterson Drake, James Madison Universityveda20Оценок пока нет

- Advt. Deputation 2018Документ8 страницAdvt. Deputation 2018veda20Оценок пока нет

- Venture Capital MarshallДокумент9 страницVenture Capital Marshallveda20Оценок пока нет

- Packet 3 SPR 17Документ164 страницыPacket 3 SPR 17veda20Оценок пока нет

- Pamela Peterson Drake, James Madison UniversityДокумент4 страницыPamela Peterson Drake, James Madison Universityveda20Оценок пока нет

- Brazilian Stagflation 2015Документ1 страницаBrazilian Stagflation 2015Victor Zhiyu Lee100% (4)

- LCR Calculation Tool - For PublicationДокумент6 страницLCR Calculation Tool - For PublicationAlper BayramОценок пока нет

- Pamela Peterson Drake, James Madison UniversityДокумент4 страницыPamela Peterson Drake, James Madison Universityveda20Оценок пока нет

- Technology: Hardware: Research IN Motion (RIMM: $73.39) 1 /buyДокумент12 страницTechnology: Hardware: Research IN Motion (RIMM: $73.39) 1 /buyveda20Оценок пока нет

- CBSE - NEET TEST 2016 ResultsДокумент2 страницыCBSE - NEET TEST 2016 Resultsveda20Оценок пока нет

- Brochure 2016 17Документ10 страницBrochure 2016 17veda20Оценок пока нет

- Accounting SyllabusДокумент3 страницыAccounting Syllabusveda20Оценок пока нет

- Bank - Model Commerzbank 1Документ10 страницBank - Model Commerzbank 1Khryss Anne Miñon MendezОценок пока нет

- Enterprise ValueДокумент3 страницыEnterprise Valueveda20Оценок пока нет

- How To Fill Application Form EMed UGET 2016Документ19 страницHow To Fill Application Form EMed UGET 2016aayuОценок пока нет

- Syllabus MGMT E-2790 Private Equity Spring 2016 1-1Документ8 страницSyllabus MGMT E-2790 Private Equity Spring 2016 1-1veda20Оценок пока нет

- TelomereTimebombs Chapter3Документ15 страницTelomereTimebombs Chapter3veda20100% (1)

- Syllabus MGMT S-2790 Private Equity Summer 2019 DRAFT 02-15Документ8 страницSyllabus MGMT S-2790 Private Equity Summer 2019 DRAFT 02-15veda20Оценок пока нет

- Immunology Standalone ModuleДокумент4 страницыImmunology Standalone Moduleveda20Оценок пока нет

- M&A at Columbia Business School: Program CurriculumДокумент6 страницM&A at Columbia Business School: Program Curriculumveda20Оценок пока нет

- Key Words: Covid-19, Credit Cycle, High-Yield Bonds, Leveraged Loans, Clos, Default Rates, Recovery Rates, Rating/Inflation, Crowding-Out, ZombiesДокумент26 страницKey Words: Covid-19, Credit Cycle, High-Yield Bonds, Leveraged Loans, Clos, Default Rates, Recovery Rates, Rating/Inflation, Crowding-Out, Zombiesveda20Оценок пока нет

- The Entry and Exit of Political Economy ArrangementsДокумент13 страницThe Entry and Exit of Political Economy ArrangementsMARIANNE JANE ZARAОценок пока нет

- Greenberg-Megaworld Demand LetterДокумент2 страницыGreenberg-Megaworld Demand LetterLilian RoqueОценок пока нет

- TCSДокумент4 страницыTCSjayasree_reddyОценок пока нет

- M&A Module 1Документ56 страницM&A Module 1avinashj8100% (1)

- ICSB Mexico MSMEs Outlook Ricardo D. Alvarez v.2.Документ4 страницыICSB Mexico MSMEs Outlook Ricardo D. Alvarez v.2.Ricardo ALvarezОценок пока нет

- Senior Development Officer Principal Major Gifts in Dallas FT Worth TX Resume Sherri TaylorДокумент2 страницыSenior Development Officer Principal Major Gifts in Dallas FT Worth TX Resume Sherri TaylorSherriTaylor2Оценок пока нет

- Its The Economy, Student! by Gloria Macapagal ArroyoДокумент9 страницIts The Economy, Student! by Gloria Macapagal ArroyodabomeisterОценок пока нет

- Article 10 - Headquarters or Regions Who Leads Growth in EMДокумент4 страницыArticle 10 - Headquarters or Regions Who Leads Growth in EMRОценок пока нет

- International Marketing "Country Notebook" Export of Cardamom To Saudi ArabiaДокумент28 страницInternational Marketing "Country Notebook" Export of Cardamom To Saudi ArabiaPurohit SagarОценок пока нет

- Population GrowthДокумент3 страницыPopulation GrowthJennybabe PetaОценок пока нет

- CPO-5 Block - Llanos Basin - Colombia, South AmericaДокумент4 страницыCPO-5 Block - Llanos Basin - Colombia, South AmericaRajesh BarkurОценок пока нет

- Project ProposalДокумент7 страницProject Proposalrehmaniaaa100% (3)

- Yong Le: Beijing Huaxia Yongleadhesive Tape Co., LTDДокумент9 страницYong Le: Beijing Huaxia Yongleadhesive Tape Co., LTDColors Little ParkОценок пока нет

- Nama Peserta BPPДокумент53 страницыNama Peserta BPPInge Syahla KearyОценок пока нет

- EV Infrastructure Solutions DEA-524Документ8 страницEV Infrastructure Solutions DEA-524tommyctechОценок пока нет

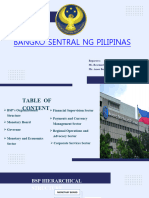

- BSP ReportДокумент20 страницBSP ReportRosemarie CabahugОценок пока нет

- Fin 254 SNT Project Ratio AnalysisДокумент29 страницFin 254 SNT Project Ratio Analysissoul1971Оценок пока нет

- Watcho Masti - Mar 02, 2023 - 1677944911Документ1 страницаWatcho Masti - Mar 02, 2023 - 1677944911Rajesh KumarОценок пока нет

- Ecosystem Services of The Congo Basin ForestsДокумент33 страницыEcosystem Services of The Congo Basin ForestsGlobal Canopy Programme100% (3)

- Steeple AnalysisДокумент2 страницыSteeple AnalysisSamrahОценок пока нет

- Only Tool in Laguna Woods Village's Toolbox Is A HammerДокумент5 страницOnly Tool in Laguna Woods Village's Toolbox Is A Hammer"Buzz" AguirreОценок пока нет

- List of TSD Facilities July 31 2019Документ15 страницList of TSD Facilities July 31 2019Emrick SantiagoОценок пока нет

- Economy of BangladeshДокумент22 страницыEconomy of BangladeshRobert DunnОценок пока нет

- Accesorios Ape TheexzoneДокумент64 страницыAccesorios Ape TheexzoneLucas GomezОценок пока нет

- Game Theory (2) - Mechanism Design With TransfersДокумент60 страницGame Theory (2) - Mechanism Design With Transfersjm15yОценок пока нет

- AMT4SAP - Junio26 - Red - v3 PDFДокумент30 страницAMT4SAP - Junio26 - Red - v3 PDFCarlos Eugenio Lovera VelasquezОценок пока нет

- Bank Guarantee BrochureДокумент46 страницBank Guarantee BrochureVictoria Adhitya0% (1)

- Understanding ManagementДокумент35 страницUnderstanding ManagementXian-liОценок пока нет

- EVALUATION OF BANK OF MAHARASTRA-DevanshuДокумент7 страницEVALUATION OF BANK OF MAHARASTRA-DevanshuDevanshu sharma100% (2)

- Buyer Questionnaire: General QuestionsДокумент3 страницыBuyer Questionnaire: General Questionsshweta meshramОценок пока нет

- The One Thing: The Surprisingly Simple Truth Behind Extraordinary ResultsОт EverandThe One Thing: The Surprisingly Simple Truth Behind Extraordinary ResultsРейтинг: 4.5 из 5 звезд4.5/5 (709)

- Summary: Atomic Habits by James Clear: An Easy & Proven Way to Build Good Habits & Break Bad OnesОт EverandSummary: Atomic Habits by James Clear: An Easy & Proven Way to Build Good Habits & Break Bad OnesРейтинг: 5 из 5 звезд5/5 (1635)

- The Compound Effect by Darren Hardy - Book Summary: Jumpstart Your Income, Your Life, Your SuccessОт EverandThe Compound Effect by Darren Hardy - Book Summary: Jumpstart Your Income, Your Life, Your SuccessРейтинг: 5 из 5 звезд5/5 (456)

- Summary of The Anxious Generation by Jonathan Haidt: How the Great Rewiring of Childhood Is Causing an Epidemic of Mental IllnessОт EverandSummary of The Anxious Generation by Jonathan Haidt: How the Great Rewiring of Childhood Is Causing an Epidemic of Mental IllnessОценок пока нет

- The Body Keeps the Score by Bessel Van der Kolk, M.D. - Book Summary: Brain, Mind, and Body in the Healing of TraumaОт EverandThe Body Keeps the Score by Bessel Van der Kolk, M.D. - Book Summary: Brain, Mind, and Body in the Healing of TraumaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Summary of The Galveston Diet by Mary Claire Haver MD: The Doctor-Developed, Patient-Proven Plan to Burn Fat and Tame Your Hormonal SymptomsОт EverandSummary of The Galveston Diet by Mary Claire Haver MD: The Doctor-Developed, Patient-Proven Plan to Burn Fat and Tame Your Hormonal SymptomsОценок пока нет

- Summary of 12 Rules for Life: An Antidote to ChaosОт EverandSummary of 12 Rules for Life: An Antidote to ChaosРейтинг: 4.5 из 5 звезд4.5/5 (294)

- How To Win Friends and Influence People by Dale Carnegie - Book SummaryОт EverandHow To Win Friends and Influence People by Dale Carnegie - Book SummaryРейтинг: 5 из 5 звезд5/5 (556)

- Mindset by Carol S. Dweck - Book Summary: The New Psychology of SuccessОт EverandMindset by Carol S. Dweck - Book Summary: The New Psychology of SuccessРейтинг: 4.5 из 5 звезд4.5/5 (328)

- SUMMARY: So Good They Can't Ignore You (UNOFFICIAL SUMMARY: Lesson from Cal Newport)От EverandSUMMARY: So Good They Can't Ignore You (UNOFFICIAL SUMMARY: Lesson from Cal Newport)Рейтинг: 4.5 из 5 звезд4.5/5 (14)

- The War of Art by Steven Pressfield - Book Summary: Break Through The Blocks And Win Your Inner Creative BattlesОт EverandThe War of Art by Steven Pressfield - Book Summary: Break Through The Blocks And Win Your Inner Creative BattlesРейтинг: 4.5 из 5 звезд4.5/5 (273)

- Can't Hurt Me by David Goggins - Book Summary: Master Your Mind and Defy the OddsОт EverandCan't Hurt Me by David Goggins - Book Summary: Master Your Mind and Defy the OddsРейтинг: 4.5 из 5 звезд4.5/5 (383)

- Make It Stick by Peter C. Brown, Henry L. Roediger III, Mark A. McDaniel - Book Summary: The Science of Successful LearningОт EverandMake It Stick by Peter C. Brown, Henry L. Roediger III, Mark A. McDaniel - Book Summary: The Science of Successful LearningРейтинг: 4.5 из 5 звезд4.5/5 (55)

- The Whole-Brain Child by Daniel J. Siegel, M.D., and Tina Payne Bryson, PhD. - Book Summary: 12 Revolutionary Strategies to Nurture Your Child’s Developing MindОт EverandThe Whole-Brain Child by Daniel J. Siegel, M.D., and Tina Payne Bryson, PhD. - Book Summary: 12 Revolutionary Strategies to Nurture Your Child’s Developing MindРейтинг: 4.5 из 5 звезд4.5/5 (57)

- Summary of Atomic Habits by James ClearОт EverandSummary of Atomic Habits by James ClearРейтинг: 5 из 5 звезд5/5 (169)

- Summary, Analysis, and Review of Daniel Kahneman's Thinking, Fast and SlowОт EverandSummary, Analysis, and Review of Daniel Kahneman's Thinking, Fast and SlowРейтинг: 3.5 из 5 звезд3.5/5 (2)

- Designing Your Life by Bill Burnett, Dave Evans - Book Summary: How to Build a Well-Lived, Joyful LifeОт EverandDesigning Your Life by Bill Burnett, Dave Evans - Book Summary: How to Build a Well-Lived, Joyful LifeРейтинг: 4.5 из 5 звезд4.5/5 (62)

- How Not to Die by Michael Greger MD, Gene Stone - Book Summary: Discover the Foods Scientifically Proven to Prevent and Reverse DiseaseОт EverandHow Not to Die by Michael Greger MD, Gene Stone - Book Summary: Discover the Foods Scientifically Proven to Prevent and Reverse DiseaseРейтинг: 4.5 из 5 звезд4.5/5 (83)

- Essentialism by Greg McKeown - Book Summary: The Disciplined Pursuit of LessОт EverandEssentialism by Greg McKeown - Book Summary: The Disciplined Pursuit of LessРейтинг: 4.5 из 5 звезд4.5/5 (187)

- The 5 Second Rule by Mel Robbins - Book Summary: Transform Your Life, Work, and Confidence with Everyday CourageОт EverandThe 5 Second Rule by Mel Robbins - Book Summary: Transform Your Life, Work, and Confidence with Everyday CourageРейтинг: 4.5 из 5 звезд4.5/5 (329)

- Psycho-Cybernetics by Maxwell Maltz - Book SummaryОт EverandPsycho-Cybernetics by Maxwell Maltz - Book SummaryРейтинг: 4.5 из 5 звезд4.5/5 (91)

- Steal Like an Artist by Austin Kleon - Book Summary: 10 Things Nobody Told You About Being CreativeОт EverandSteal Like an Artist by Austin Kleon - Book Summary: 10 Things Nobody Told You About Being CreativeРейтинг: 4.5 из 5 звезд4.5/5 (128)

- Summary of The Algebra of Wealth by Scott Galloway: A Simple Formula for Financial SecurityОт EverandSummary of The Algebra of Wealth by Scott Galloway: A Simple Formula for Financial SecurityОценок пока нет

- We Were the Lucky Ones: by Georgia Hunter | Conversation StartersОт EverandWe Were the Lucky Ones: by Georgia Hunter | Conversation StartersОценок пока нет

- Tiny Habits by BJ Fogg - Book Summary: The Small Changes That Change EverythingОт EverandTiny Habits by BJ Fogg - Book Summary: The Small Changes That Change EverythingРейтинг: 4.5 из 5 звезд4.5/5 (111)

- Summary of The Compound Effect by Darren HardyОт EverandSummary of The Compound Effect by Darren HardyРейтинг: 5 из 5 звезд5/5 (70)

- Summary of Slow Productivity by Cal Newport: The Lost Art of Accomplishment Without BurnoutОт EverandSummary of Slow Productivity by Cal Newport: The Lost Art of Accomplishment Without BurnoutРейтинг: 1 из 5 звезд1/5 (1)

- Blink by Malcolm Gladwell - Book Summary: The Power of Thinking Without ThinkingОт EverandBlink by Malcolm Gladwell - Book Summary: The Power of Thinking Without ThinkingРейтинг: 4.5 из 5 звезд4.5/5 (114)