Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Blmscul3542895 PDFДокумент1 страницаBlmscul3542895 PDFEric Jara0% (1)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- University of Vermont Branding and Marketing RFPДокумент14 страницUniversity of Vermont Branding and Marketing RFPSeven Days VermontОценок пока нет

- Deep Learning Book, by Ian Goodfellow, Yoshua Bengio and Aaron CourvilleДокумент38 страницDeep Learning Book, by Ian Goodfellow, Yoshua Bengio and Aaron CourvilleHarshitShuklaОценок пока нет

- Trust AgreementДокумент4 страницыTrust AgreementDeb VeilleОценок пока нет

- ServiceNow Solution OverviewДокумент5 страницServiceNow Solution OverviewDany Ukken75% (4)

- Srimad Bhagvatam PDFДокумент64 страницыSrimad Bhagvatam PDFmonashaОценок пока нет

- Study and Practice of Yoga Volume-IДокумент8 страницStudy and Practice of Yoga Volume-IHarshitShuklaОценок пока нет

- Onboarding - FAQ'sДокумент4 страницыOnboarding - FAQ'sHarshitShuklaОценок пока нет

- Yoga of Knowledge Pandit M.P.Документ292 страницыYoga of Knowledge Pandit M.P.HarshitShuklaОценок пока нет

- Deep Learning LibДокумент3 страницыDeep Learning LibrakikiraОценок пока нет

- Algorithms Illuminated: Part 2: Graph Algorithms and Data Structures Tim RoughgardenДокумент28 страницAlgorithms Illuminated: Part 2: Graph Algorithms and Data Structures Tim RoughgardenHarshitShuklaОценок пока нет

- Glimpses of Vedic LiteratureДокумент255 страницGlimpses of Vedic LiteratureHarshitShuklaОценок пока нет

- Tablet Publisher: - InstructionsДокумент18 страницTablet Publisher: - InstructionsHarshitShuklaОценок пока нет

- Graph Traversals: Slides by Carl KingsfordДокумент52 страницыGraph Traversals: Slides by Carl KingsfordHarshitShuklaОценок пока нет

- InterOP TestReportДокумент28 страницInterOP TestReportHarshitShuklaОценок пока нет

- FGH Global 141104 EnglishДокумент2 страницыFGH Global 141104 EnglishHarshitShuklaОценок пока нет

- Dem128064f FGH PWДокумент16 страницDem128064f FGH PWHarshitShuklaОценок пока нет

- IRCP Policies Pic 4 3 16 PDFДокумент2 страницыIRCP Policies Pic 4 3 16 PDFHarshitShuklaОценок пока нет

- Full PDFДокумент13 страницFull PDFHarshitShuklaОценок пока нет

- Teaching Philosophy Guidelines PDFДокумент14 страницTeaching Philosophy Guidelines PDFHarshitShuklaОценок пока нет

- 13494T 2017IF USA-CAN Wild West Cowboys and Buffalos STD EDTPДокумент2 страницы13494T 2017IF USA-CAN Wild West Cowboys and Buffalos STD EDTPHarshitShuklaОценок пока нет

- 1york Yhe 5005747 Ytg A 0216Документ70 страниц1york Yhe 5005747 Ytg A 0216HarshitShuklaОценок пока нет

- Retiree Tuition Benefit PDFДокумент1 страницаRetiree Tuition Benefit PDFHarshitShuklaОценок пока нет

- Modern Placer MiningДокумент36 страницModern Placer MiningHarshitShuklaОценок пока нет

- Ytg A 0609Документ54 страницыYtg A 0609HarshitShuklaОценок пока нет

- Computer Science Major Worksheet 2016 17 PDFДокумент2 страницыComputer Science Major Worksheet 2016 17 PDFHarshitShuklaОценок пока нет

- YTG J 1009SunlineXPДокумент73 страницыYTG J 1009SunlineXPHarshitShuklaОценок пока нет

- Manual Chiller York Model Ytg 3Документ3 страницыManual Chiller York Model Ytg 3HarshitShuklaОценок пока нет

- Manual Chiller York Model Ytg 5Документ4 страницыManual Chiller York Model Ytg 5HarshitShuklaОценок пока нет

- Ytg PDFДокумент2 страницыYtg PDFHarshitShuklaОценок пока нет

- YG Core Competency FrameworkДокумент15 страницYG Core Competency FrameworkHarshitShukla100% (1)

- Mcbee V Gy YhrbaДокумент17 страницMcbee V Gy YhrbaHarshitShuklaОценок пока нет

- Manual Chiller York Model Ytg 6Документ2 страницыManual Chiller York Model Ytg 6HarshitShukla100% (1)

- DFSДокумент19 страницDFSHarshitShuklaОценок пока нет

- The Origin of Financial Crises by George CooperДокумент6 страницThe Origin of Financial Crises by George CooperSoner Atakan Ertürk0% (1)

- 1567408107395rej1z59pM0TrJ6Ni PDFДокумент2 страницы1567408107395rej1z59pM0TrJ6Ni PDFBrajesh PandayОценок пока нет

- R12 Accounts PayablesДокумент19 страницR12 Accounts Payablesfreeman_agОценок пока нет

- 2 IFRS 17 The Actuarial ViewДокумент33 страницы2 IFRS 17 The Actuarial ViewmarhadiОценок пока нет

- Arrieta Vs Natl Rice and Corn CorpДокумент1 страницаArrieta Vs Natl Rice and Corn Corpkhayis_belsОценок пока нет

- IFRS 17 - Profit Profiles Under IFRS 4 and IFRS 17 - 20190717 PDFДокумент3 страницыIFRS 17 - Profit Profiles Under IFRS 4 and IFRS 17 - 20190717 PDFkhedidja attiaОценок пока нет

- NCLT 23march21Документ124 страницыNCLT 23march21Sharp ToungeОценок пока нет

- Bank GuaranteeДокумент2 страницыBank GuaranteeFaridul Alam100% (1)

- Dem Federal FDIC V Direct Ores RGДокумент85 страницDem Federal FDIC V Direct Ores RGOscar J. SerranoОценок пока нет

- Air WaybillДокумент1 страницаAir WaybillRizal BachtiarОценок пока нет

- Bank Statement Template 3 - TemplateLabДокумент3 страницыBank Statement Template 3 - TemplateLabFrank GallagherОценок пока нет

- Patwar KhanaДокумент12 страницPatwar KhanaFaisal RafiqОценок пока нет

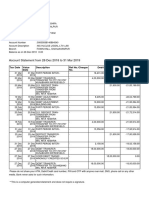

- Statement One YearДокумент7 страницStatement One YearAjay Chowdary Ajay ChowdaryОценок пока нет

- IllustrationДокумент3 страницыIllustrationShivakant ManchandaОценок пока нет

- Bank Reconciliation PDFДокумент2 страницыBank Reconciliation PDFFazal Rehman MandokhailОценок пока нет

- All Enrolment Centres List11 12 2022 7 03 49 PMДокумент6 страницAll Enrolment Centres List11 12 2022 7 03 49 PMpuneetchadhokarОценок пока нет

- Basic Reconciliation StatementsДокумент41 страницаBasic Reconciliation StatementsBeverly EroyОценок пока нет

- Assignment 1 Sunstone 119045Документ3 страницыAssignment 1 Sunstone 119045Rohit YadavОценок пока нет

- SOF DL en Brand V15 - tcm41 180545 PDFДокумент11 страницSOF DL en Brand V15 - tcm41 180545 PDFAnkur GargОценок пока нет

- AccountingequationДокумент6 страницAccountingequationJolly Singhal100% (1)

- Personal Loan Application FormДокумент1 страницаPersonal Loan Application FormMikky Garcia Dela CruzОценок пока нет

- Furikomi - A Step by Step Guide To Bank Transfers in Japan - GaijinPotДокумент12 страницFurikomi - A Step by Step Guide To Bank Transfers in Japan - GaijinPotrlab1000Оценок пока нет

- Payment and Other TermsДокумент11 страницPayment and Other TermsNguyệtt HươnggОценок пока нет

- Regarding PaymentДокумент2 страницыRegarding Paymentbab1235Оценок пока нет

- Intercontinental Bank Debunks Akingbola's Claims - 101010Документ2 страницыIntercontinental Bank Debunks Akingbola's Claims - 101010ProshareОценок пока нет