Вам также может понравиться

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Florida Motor Fuel Tax Relief Act of 2022Документ9 страницFlorida Motor Fuel Tax Relief Act of 2022ABC Action NewsОценок пока нет

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- ZH210LC 5BДокумент24 страницыZH210LC 5BPHÁT NGUYỄN THẾ0% (1)

- Solution To Campbell Lo Mackinlay PDFДокумент71 страницаSolution To Campbell Lo Mackinlay PDFstaimouk0% (1)

- The Role of Needs Analysis in Adult ESL Programme Design: Geoffrey BrindleyДокумент16 страницThe Role of Needs Analysis in Adult ESL Programme Design: Geoffrey Brindleydeise krieser100% (2)

- Tourism PlanningДокумент36 страницTourism PlanningAvegael Tonido Rotugal100% (1)

- CLT For Triangular Arrays: Alain-Philippe Fortin September 2020Документ1 страницаCLT For Triangular Arrays: Alain-Philippe Fortin September 2020Alain-Philippe FortinОценок пока нет

- ConvergenceДокумент5 страницConvergenceAlain-Philippe FortinОценок пока нет

- DATASP500Документ75 страницDATASP500Alain-Philippe FortinОценок пока нет

- 2 ReportДокумент2 страницы2 ReportAlain-Philippe FortinОценок пока нет

- Visualizing L Hopitals RuleДокумент7 страницVisualizing L Hopitals RuleAlain-Philippe FortinОценок пока нет

- Excel Is The Primary Choice in The Financial IndustryДокумент1 страницаExcel Is The Primary Choice in The Financial IndustryAlain-Philippe FortinОценок пока нет

- PCA Bias Squared Residuals: Alain-Philippe Fortin September 2020Документ3 страницыPCA Bias Squared Residuals: Alain-Philippe Fortin September 2020Alain-Philippe FortinОценок пока нет

- BankДокумент2 страницыBankAlain-Philippe FortinОценок пока нет

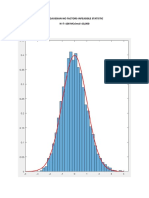

- Iid Gaussian-No Factors-Infeasible StatisticДокумент4 страницыIid Gaussian-No Factors-Infeasible StatisticAlain-Philippe FortinОценок пока нет

- QVДокумент7 страницQVAlain-Philippe FortinОценок пока нет

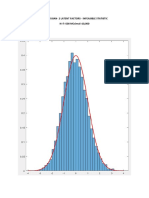

- Iid Gaussian - 2 Latent FactorsДокумент4 страницыIid Gaussian - 2 Latent FactorsAlain-Philippe FortinОценок пока нет

- 7 AptДокумент19 страниц7 AptBikram MaharjanОценок пока нет

- DATASP500Документ75 страницDATASP500Alain-Philippe FortinОценок пока нет

- Valuations: Interdependent Values and Is Particularly Suited For Situations in Which The Object Being Sold Is AnДокумент10 страницValuations: Interdependent Values and Is Particularly Suited For Situations in Which The Object Being Sold Is AnAlain-Philippe FortinОценок пока нет

- For MulesДокумент20 страницFor MulesAlain-Philippe FortinОценок пока нет

- FEДокумент38 страницFEAlain-Philippe FortinОценок пока нет

- BCV 2016 PDFДокумент200 страницBCV 2016 PDFAlain-Philippe FortinОценок пока нет

- Sharpe RatioДокумент1 страницаSharpe RatioAlain-Philippe FortinОценок пока нет

- BetaДокумент1 страницаBetaAlain-Philippe FortinОценок пока нет

- CLC Clear : The Plot Shows That It Can Take Many Periods Before Going BustДокумент2 страницыCLC Clear : The Plot Shows That It Can Take Many Periods Before Going BustAlain-Philippe FortinОценок пока нет

- ExercisesДокумент1 страницаExercisesAlain-Philippe FortinОценок пока нет

- BiasesДокумент6 страницBiasesAlain-Philippe FortinОценок пока нет

- Lecture 2 - IVДокумент45 страницLecture 2 - IVbanderasОценок пока нет

- Quiz 1Документ1 страницаQuiz 1Alain-Philippe FortinОценок пока нет

- MNДокумент1 страницаMNAlain-Philippe FortinОценок пока нет

- SequencesДокумент2 страницыSequencesAlain-Philippe FortinОценок пока нет

- Additive FunctionsДокумент2 страницыAdditive FunctionsAlain-Philippe FortinОценок пока нет

- Integer PartДокумент2 страницыInteger PartAlain-Philippe FortinОценок пока нет

- 1 Caveats: JT T JT JTДокумент1 страница1 Caveats: JT T JT JTAlain-Philippe FortinОценок пока нет

- Chapter 07Документ16 страницChapter 07Elmarie RecorbaОценок пока нет

- Effect of Heater Geometry On The High Temperature Distribution On A MEMS Micro-HotplateДокумент6 страницEffect of Heater Geometry On The High Temperature Distribution On A MEMS Micro-HotplateJorge GuerreroОценок пока нет

- Analysis of Green Entrepreneurship Practices in IndiaДокумент5 страницAnalysis of Green Entrepreneurship Practices in IndiaK SrivarunОценок пока нет

- Describe an English lesson you enjoyed.: 多叔逻辑口语,中国雅思口语第一品牌 公共微信: ddielts 新浪微博@雅思钱多多Документ7 страницDescribe an English lesson you enjoyed.: 多叔逻辑口语,中国雅思口语第一品牌 公共微信: ddielts 新浪微博@雅思钱多多Siyeon YeungОценок пока нет

- TIB Bwpluginrestjson 2.1.0 ReadmeДокумент2 страницыTIB Bwpluginrestjson 2.1.0 ReadmemarcmariehenriОценок пока нет

- Activity 2Документ5 страницActivity 2DIOSAY, CHELZEYA A.Оценок пока нет

- Gr. 10 Persuasive EssayДокумент22 страницыGr. 10 Persuasive EssayZephania JandayanОценок пока нет

- Backward Forward PropogationДокумент19 страницBackward Forward PropogationConrad WaluddeОценок пока нет

- Quemador BrahmaДокумент4 страницыQuemador BrahmaClaudio VerdeОценок пока нет

- Relay G30 ManualДокумент42 страницыRelay G30 ManualLeon KhiuОценок пока нет

- Burn Tests On FibresДокумент2 страницыBurn Tests On Fibresapi-32133818100% (1)

- AB-005-2020 Dated 10.09.2020 (SKF-Prestine)Документ3 страницыAB-005-2020 Dated 10.09.2020 (SKF-Prestine)AliasgarОценок пока нет

- EE360 - Magnetic CircuitsДокумент48 страницEE360 - Magnetic Circuitsبدون اسمОценок пока нет

- Test Report: Tested By-Checked byДокумент12 страницTest Report: Tested By-Checked byjamilОценок пока нет

- Pressure-Dependent Leak Detection Model and Its Application To A District Water SystemДокумент13 страницPressure-Dependent Leak Detection Model and Its Application To A District Water SystemManjul KothariОценок пока нет

- Warning: Shaded Answers Without Corresponding Solution Will Incur Deductive PointsДокумент1 страницаWarning: Shaded Answers Without Corresponding Solution Will Incur Deductive PointsKhiara Claudine EspinosaОценок пока нет

- VPZ M BrochureДокумент2 страницыVPZ M BrochuresundyaОценок пока нет

- Cultural Practices of India Which Is Adopted by ScienceДокумент2 страницыCultural Practices of India Which Is Adopted by ScienceLevina Mary binuОценок пока нет

- Dimmable Bulbs SamplesДокумент11 страницDimmable Bulbs SamplesBOSS BalaОценок пока нет

- Sai Deepa Rock Drills: Unless Otherwise Specified ToleranceДокумент1 страницаSai Deepa Rock Drills: Unless Otherwise Specified ToleranceRavi BabaladiОценок пока нет

- Form No. 1 Gangtok Municipal Corporation Deorali, SikkimДокумент2 страницыForm No. 1 Gangtok Municipal Corporation Deorali, SikkimMUSKAANОценок пока нет

- Soil Liquefaction Analysis of Banasree Residential Area, Dhaka Using NovoliqДокумент7 страницSoil Liquefaction Analysis of Banasree Residential Area, Dhaka Using NovoliqPicasso DebnathОценок пока нет

- 3.15.E.V25 Pneumatic Control Valves DN125-150-EnДокумент3 страницы3.15.E.V25 Pneumatic Control Valves DN125-150-EnlesonspkОценок пока нет

- ECON 401/601, Microeconomic Theory 3/micro 1: Jean Guillaume Forand Fall 2019, WaterlooДокумент3 страницыECON 401/601, Microeconomic Theory 3/micro 1: Jean Guillaume Forand Fall 2019, WaterlooTarun SharmaОценок пока нет

- 1974 - Roncaglia - The Reduction of Complex LabourДокумент12 страниц1974 - Roncaglia - The Reduction of Complex LabourRichardОценок пока нет

- Reading Proficiency Level of Students: Basis For Reading Intervention ProgramДокумент13 страницReading Proficiency Level of Students: Basis For Reading Intervention ProgramSONY JOY QUINTOОценок пока нет