Вам также может понравиться

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Gutierrez Arnaiz - Real Options With Unknown-Date Events - CongressДокумент28 страницGutierrez Arnaiz - Real Options With Unknown-Date Events - CongressAndrew Drummond-MurrayОценок пока нет

- Artigo Real Options Where Are The Imperator ClothesДокумент30 страницArtigo Real Options Where Are The Imperator ClothesAndrew Drummond-MurrayОценок пока нет

- Artigo Option Pricing in A Real WorldДокумент55 страницArtigo Option Pricing in A Real WorldAndrew Drummond-MurrayОценок пока нет

- Artigo An Investment Criterion Incorporating Real OptionsДокумент8 страницArtigo An Investment Criterion Incorporating Real OptionsAndrew Drummond-MurrayОценок пока нет

- Artigo Real Organizations For Real OptionsДокумент45 страницArtigo Real Organizations For Real OptionsAndrew Drummond-MurrayОценок пока нет

- The Holy Grail PDFДокумент632 страницыThe Holy Grail PDFAndrew Drummond-MurrayОценок пока нет

- Artigo Pricing Options and Real Options For ExcelДокумент14 страницArtigo Pricing Options and Real Options For ExcelAndrew Drummond-MurrayОценок пока нет

- Artigo Evaluating Natural Resource Investmens Using Monte Carlo SimulationДокумент33 страницыArtigo Evaluating Natural Resource Investmens Using Monte Carlo SimulationAndrew Drummond-MurrayОценок пока нет

- Controlling Cfar With Real Options. A Univariate Case StudyДокумент41 страницаControlling Cfar With Real Options. A Univariate Case StudyAndrew Drummond-MurrayОценок пока нет

- Container Shipping and Ports: An Overview: Theo E. NotteboomДокумент21 страницаContainer Shipping and Ports: An Overview: Theo E. NotteboomMuhammad Ashari Fitra RachmannullahОценок пока нет

- Artigo Rubinstein Implied Binomial TreesДокумент43 страницыArtigo Rubinstein Implied Binomial TreesAndrew Drummond-MurrayОценок пока нет

- Container Shipping and Ports: An Overview: Theo E. NotteboomДокумент21 страницаContainer Shipping and Ports: An Overview: Theo E. NotteboomMuhammad Ashari Fitra RachmannullahОценок пока нет

- Artigo Markett Shiping Carriers OptionsДокумент18 страницArtigo Markett Shiping Carriers OptionsAndrew Drummond-MurrayОценок пока нет

- Zadeh L.a.-Fuzzy Sets (1965)Документ16 страницZadeh L.a.-Fuzzy Sets (1965)Nita FerdianaОценок пока нет

- Apostila Logica Nebulosa UFRJДокумент75 страницApostila Logica Nebulosa UFRJAndrew Drummond-MurrayОценок пока нет

- Artigo The Valuation of Corporate DebtДокумент26 страницArtigo The Valuation of Corporate DebtAndrew Drummond-MurrayОценок пока нет

- Introduction Hand OutДокумент14 страницIntroduction Hand OutAndrew Drummond-MurrayОценок пока нет

- Sets OperationsДокумент15 страницSets OperationsAndrew Drummond-MurrayОценок пока нет

- PhytonДокумент2 страницыPhytonAndrew Drummond-MurrayОценок пока нет

- Im Plica Coes Hand OutДокумент9 страницIm Plica Coes Hand OutAndrew Drummond-MurrayОценок пока нет

- Rules by Learning From ExamplesДокумент3 страницыRules by Learning From ExamplesAndrew Drummond-MurrayОценок пока нет

- Artigo The Valuation of Corporate DebtДокумент26 страницArtigo The Valuation of Corporate DebtAndrew Drummond-MurrayОценок пока нет

- Very Near: TallДокумент8 страницVery Near: TallAndrew Drummond-MurrayОценок пока нет

- Artigo Strategic Debt RestructuringДокумент46 страницArtigo Strategic Debt RestructuringAndrew Drummond-MurrayОценок пока нет

- BPM Standards ComparisonДокумент31 страницаBPM Standards ComparisonAndrew Drummond-MurrayОценок пока нет

- Levered and Unlevered BetaДокумент18 страницLevered and Unlevered BetaarchitbumbОценок пока нет

- Musings On The Geometric Properties of The Square and CompassesДокумент7 страницMusings On The Geometric Properties of The Square and CompassesAndrew Drummond-MurrayОценок пока нет

- Speculation On The Symbol of The Square and CompassesДокумент4 страницыSpeculation On The Symbol of The Square and CompassesAndrew Drummond-MurrayОценок пока нет

- Apresentacao ValuationДокумент107 страницApresentacao ValuationAndrew Drummond-MurrayОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- LK TPM 31 Mar 2023 PDFДокумент67 страницLK TPM 31 Mar 2023 PDFAnonymous waj9QU06Оценок пока нет

- Tugas 1 TMK Adbi4201 Bahasa Inggris NiagaДокумент3 страницыTugas 1 TMK Adbi4201 Bahasa Inggris NiagaSakazukiОценок пока нет

- Summary of Account: Invoice/Statement of Account Service Tax REG. NO:B16-1808-31031789Документ4 страницыSummary of Account: Invoice/Statement of Account Service Tax REG. NO:B16-1808-31031789NKОценок пока нет

- Presentation On State Financial Corporation: Presented By:-Parul Jain Vanadna Tyagi Jitendra SinghДокумент18 страницPresentation On State Financial Corporation: Presented By:-Parul Jain Vanadna Tyagi Jitendra SinghJitendra SinghОценок пока нет

- Fedai Rule - 2012 (Circular)Документ15 страницFedai Rule - 2012 (Circular)Ramam Remo RemoОценок пока нет

- IDEX 2022 Q4 Interim ReportДокумент26 страницIDEX 2022 Q4 Interim ReportMaria PolyuhanychОценок пока нет

- Internship Report On UBLДокумент62 страницыInternship Report On UBLbbaahmad89Оценок пока нет

- KPMG Flash News Draft Guidelines For Core Investment CompaniesДокумент5 страницKPMG Flash News Draft Guidelines For Core Investment CompaniesmurthyeОценок пока нет

- The Coinage of Two Hundred Rupees and Ten Rupees Coins To Commemorate The Occasion of 200 H BIRTH ANNIVERSARY of TATYA TOPE Rules, 2015.Документ6 страницThe Coinage of Two Hundred Rupees and Ten Rupees Coins To Commemorate The Occasion of 200 H BIRTH ANNIVERSARY of TATYA TOPE Rules, 2015.Latest Laws TeamОценок пока нет

- Bii Global Outlook 2023Документ16 страницBii Global Outlook 2023Zerohedge Janitor89% (9)

- (Acb) SFRДокумент57 страниц(Acb) SFRVu Thi NinhОценок пока нет

- COOPДокумент8 страницCOOPJohn Kenneth BoholОценок пока нет

- We Won The Revolution & We Own The Knowledge of ItДокумент311 страницWe Won The Revolution & We Own The Knowledge of ItSusan100% (1)

- Financial Statements 2, ModuleДокумент4 страницыFinancial Statements 2, ModuleSUHARTO USMANОценок пока нет

- Accounting 101 Chapter 1Документ39 страницAccounting 101 Chapter 1Md. Riyad Mahmud 183-15-11991Оценок пока нет

- MBBsavings - 164017 212412 - 2022 08 31 PDFДокумент4 страницыMBBsavings - 164017 212412 - 2022 08 31 PDFAdeela fazlinОценок пока нет

- Regions Bank StatementДокумент1 страницаRegions Bank Statementdudu adulОценок пока нет

- Private BankingДокумент53 страницыPrivate BankingChristine Gillespie100% (12)

- Exposure To Currency Risk, Definition and MeasurementДокумент12 страницExposure To Currency Risk, Definition and MeasurementGustavo Adolfo Leyva LópezОценок пока нет

- Investment Center and Transfer PricingДокумент10 страницInvestment Center and Transfer Pricingrakib_0011Оценок пока нет

- RRL ForeignДокумент4 страницыRRL Foreignゔ違でStrawberry milkОценок пока нет

- Complete Guide To Value InvestingДокумент59 страницComplete Guide To Value InvestingPaulo TrickОценок пока нет

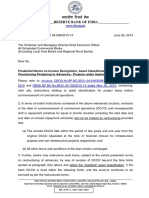

- Prudential Norms On Income Recognition, Asset Classification and Provisioning Pertaining To Advances - Projects Under Implementation PDFДокумент2 страницыPrudential Norms On Income Recognition, Asset Classification and Provisioning Pertaining To Advances - Projects Under Implementation PDFPraveer MoreyОценок пока нет

- Negotiable Instruments Act 1881Документ47 страницNegotiable Instruments Act 1881SupriyamathewОценок пока нет

- Cuestionario 4Документ3 страницыCuestionario 4Carlos Hasler Ballesteros BarraganОценок пока нет

- Bond Yield CalculatorДокумент1 страницаBond Yield CalculatorsarangdharОценок пока нет

- AntichresisДокумент2 страницыAntichresiscrisypilОценок пока нет

- Enterprise Risk ManagementДокумент29 страницEnterprise Risk ManagementSujeewa LakmalОценок пока нет

- My Home Raka Price ListДокумент1 страницаMy Home Raka Price ListManohar Reddy MavillaОценок пока нет

- RiskДокумент3 страницыRiskChaucer19Оценок пока нет