Вам также может понравиться

- Crimpro - Transcript (J. Cornejo)Документ2 страницыCrimpro - Transcript (J. Cornejo)Pau JoyosaОценок пока нет

- Sps Dacudao vs. Secretary of Justice GonzalesДокумент11 страницSps Dacudao vs. Secretary of Justice GonzalesaudreyracelaОценок пока нет

- Legal OpinionДокумент3 страницыLegal Opinionknicky FranciscoОценок пока нет

- CRIMINAL LAW TIPSДокумент54 страницыCRIMINAL LAW TIPSPaula GasparОценок пока нет

- AUSL Bar Operations 2017 LMT Property EditedДокумент6 страницAUSL Bar Operations 2017 LMT Property EditedEron Roi Centina-gacutanОценок пока нет

- Part III BOOK II Special Laws Criminal Law 2019 Bar Last Minute SNM IIДокумент37 страницPart III BOOK II Special Laws Criminal Law 2019 Bar Last Minute SNM IIFatimah MandanganОценок пока нет

- Illegal DismissalДокумент6 страницIllegal DismissalPatricia David-MolinaОценок пока нет

- Amendments to the Tax Code under TRAIN LawДокумент23 страницыAmendments to the Tax Code under TRAIN LawCha GalangОценок пока нет

- SababanMagicNotes TaxationLaw1Документ46 страницSababanMagicNotes TaxationLaw1Marife Tubilag Maneja100% (1)

- Continuation (Corp and Corporate Rehabilitation) Combination of The Two (2) TestsДокумент5 страницContinuation (Corp and Corporate Rehabilitation) Combination of The Two (2) TestsAdam SmithОценок пока нет

- Tax Updates by Atty. LumberaДокумент68 страницTax Updates by Atty. Lumberaavery03Оценок пока нет

- Tariff Notes - Atty CabanДокумент14 страницTariff Notes - Atty CabancH3RrY1007Оценок пока нет

- San Beda LMT Soc LegДокумент6 страницSan Beda LMT Soc LegromarcambriОценок пока нет

- Civil Law Review CasesДокумент16 страницCivil Law Review CasesMary Ann Celeste LeuterioОценок пока нет

- Bar Reviewers2Документ3 страницыBar Reviewers2Mar Sayos Dales100% (1)

- CivproДокумент188 страницCivproCpreiiОценок пока нет

- Taxation FaqДокумент40 страницTaxation FaqPeter AllanОценок пока нет

- Did You Know That???Документ2 страницыDid You Know That???sylvia patriciaОценок пока нет

- PTB VillaceteДокумент4 страницыPTB VillaceteAngie DouglasОценок пока нет

- LABOR LAW PRINCIPLES AND RIGHTSДокумент84 страницыLABOR LAW PRINCIPLES AND RIGHTSIzo BellosilloОценок пока нет

- UP Criminal-LawДокумент22 страницыUP Criminal-LawFritz SaponОценок пока нет

- VERIFIED LEGAL DOCUMENTSДокумент4 страницыVERIFIED LEGAL DOCUMENTSeieipОценок пока нет

- CLE Syllabus For EvidenceДокумент3 страницыCLE Syllabus For EvidencewadzievjОценок пока нет

- Torts Tiwa Lat at Ample XДокумент13 страницTorts Tiwa Lat at Ample XMark De JesusОценок пока нет

- Commercial Law Memoryaid: Code of CommerceДокумент46 страницCommercial Law Memoryaid: Code of CommerceCliffordОценок пока нет

- Gardenia Bakeries (Philippines), Inc. vs. Marby Food Ventures CorporationДокумент1 страницаGardenia Bakeries (Philippines), Inc. vs. Marby Food Ventures CorporationanonОценок пока нет

- SPS. CARLOS S. ROMUALDEZ AND ERLINDA R. ROMUALDEZ, Petitioners, v. COMMISSION ON ELECTIONS AND DENNIS GARAY, Respondents.Документ16 страницSPS. CARLOS S. ROMUALDEZ AND ERLINDA R. ROMUALDEZ, Petitioners, v. COMMISSION ON ELECTIONS AND DENNIS GARAY, Respondents.ZACH MATTHEW GALENDEZОценок пока нет

- CW Mini Capslet Qtr. 4 WK 2 2021Документ8 страницCW Mini Capslet Qtr. 4 WK 2 2021Amil, Shierly Mae S. -10 QUISUMBINGОценок пока нет

- UST - Mercantile Law Preweek 2018159572700 PDFДокумент46 страницUST - Mercantile Law Preweek 2018159572700 PDFMarie Chu100% (1)

- Materials To Use For The 2012 Bar ExamsДокумент1 страницаMaterials To Use For The 2012 Bar Examsnike2017100% (2)

- Civil Law Bar Questions (No Answers) 2007-2014Документ105 страницCivil Law Bar Questions (No Answers) 2007-2014Pebs DrlieОценок пока нет

- Insurance Code Updates Based On RA 10607Документ47 страницInsurance Code Updates Based On RA 10607Kristine Dinar C. SisonОценок пока нет

- Cases LeonenДокумент28 страницCases LeonenJenniferPizarrasCadiz-CarullaОценок пока нет

- Civil Law Reviewer - Bar 2018Документ12 страницCivil Law Reviewer - Bar 2018Kevin Ampuan100% (2)

- Criminal Cases Penned by Justice Perlas Bernabe, by Judge CampanillaДокумент16 страницCriminal Cases Penned by Justice Perlas Bernabe, by Judge Campanilladhine77100% (2)

- Understanding Criminal Law Elements and ParticipationДокумент23 страницыUnderstanding Criminal Law Elements and ParticipationSB100% (1)

- Bar 2019 Checklist: Subject Reviewer NOTES (July) Cases Remarks Political LawДокумент2 страницыBar 2019 Checklist: Subject Reviewer NOTES (July) Cases Remarks Political Lawi syОценок пока нет

- Bar Exam Answers Useful Introductory LinesДокумент32 страницыBar Exam Answers Useful Introductory LinesPaolo VillanuevaОценок пока нет

- Pomoly Bar Reviewer Day 2 PM EthicsДокумент35 страницPomoly Bar Reviewer Day 2 PM EthicsRomeo RemotinОценок пока нет

- Philippine Citizenship Laws ExplainedДокумент5 страницPhilippine Citizenship Laws Explainedaerosmith_julio6627Оценок пока нет

- 16 Cut Taxation Local & RealДокумент24 страницы16 Cut Taxation Local & RealMirandaKarrivinОценок пока нет

- 2 DLSU LCBO Labor Law and SocialДокумент46 страниц2 DLSU LCBO Labor Law and SocialNewCovenantChurch100% (1)

- 2019 AUSL LMT Legal Ethics Draft PDFДокумент14 страниц2019 AUSL LMT Legal Ethics Draft PDFJo GutierrezОценок пока нет

- Phbar ReviewДокумент52 страницыPhbar ReviewSuiОценок пока нет

- Prof. Elmer T. Rabuya’s Pre-Week Notes in Civil LawДокумент48 страницProf. Elmer T. Rabuya’s Pre-Week Notes in Civil LawMaverick Jann Esteban100% (2)

- Amendments to Philippine Tax Code ProvisionsДокумент17 страницAmendments to Philippine Tax Code ProvisionsThor D. CruzОценок пока нет

- MaltExports PDFДокумент26 страницMaltExports PDFboldyОценок пока нет

- Reference materials for law subjectsДокумент2 страницыReference materials for law subjectsOna DlanorОценок пока нет

- Specpro - GuardianshipДокумент22 страницыSpecpro - GuardianshipAbbyAlvarezОценок пока нет

- UPH Final Exam-Labor Standards 2014Документ7 страницUPH Final Exam-Labor Standards 2014Jenely Joy Areola-TelanОценок пока нет

- Practice Court 1Документ9 страницPractice Court 1NikkiMaxineValdezОценок пока нет

- Legal Forms - Week 4Документ4 страницыLegal Forms - Week 4TtlrpqОценок пока нет

- Phil. Am. Life Vs Angelita GramajeДокумент21 страницаPhil. Am. Life Vs Angelita GramajeJesa FormaranОценок пока нет

- ATTY. CECILIO DUKA - Juvenile Justice and Welfare ActДокумент4 страницыATTY. CECILIO DUKA - Juvenile Justice and Welfare ActAga FatrickОценок пока нет

- Income Tax Lumbera Part 5Документ18 страницIncome Tax Lumbera Part 5Timothy Mark MaderazoОценок пока нет

- Transfer Taxes Explained: Estate Tax, Donor's Tax, and MoreДокумент101 страницаTransfer Taxes Explained: Estate Tax, Donor's Tax, and MoreAngelo IvanОценок пока нет

- Taxation IIДокумент72 страницыTaxation IIArnold OniaОценок пока нет

- Estate, donor, VAT, excise tax reviewerДокумент3 страницыEstate, donor, VAT, excise tax reviewercardeguzmanОценок пока нет

- Taxation TwoДокумент66 страницTaxation TwomashedpotatoaddictОценок пока нет

- Memorandum Maderazo 2015120709 MSWДокумент6 страницMemorandum Maderazo 2015120709 MSWTimothy Mark MaderazoОценок пока нет

- First Impression RulingДокумент2 страницыFirst Impression RulingTimothy Mark MaderazoОценок пока нет

- 01 Computer HistoryДокумент16 страниц01 Computer HistoryRazonable Morales RommelОценок пока нет

- Human RightsДокумент73 страницыHuman RightsTimothy Mark MaderazoОценок пока нет

- Sky. 30 Jul 2017. 9pmДокумент1 страницаSky. 30 Jul 2017. 9pmTimothy Mark MaderazoОценок пока нет

- Taxation OrtegaДокумент4 страницыTaxation OrtegaTimothy Mark MaderazoОценок пока нет

- Taxation ReviewerДокумент25 страницTaxation ReviewerLes EvangeListaОценок пока нет

- Labor Relations - Assignment Cases1Документ49 страницLabor Relations - Assignment Cases1Timothy Mark MaderazoОценок пока нет

- Judicial Affidavit RequisitesДокумент18 страницJudicial Affidavit RequisitesTimothy Mark MaderazoОценок пока нет

- 4 People Vs AnchetaДокумент17 страниц4 People Vs AnchetaMichael Kevin MangaoОценок пока нет

- Agency 1 and 3cДокумент23 страницыAgency 1 and 3cTimothy Mark MaderazoОценок пока нет

- Establishing The PM CДокумент16 страницEstablishing The PM CMaryroseОценок пока нет

- Fundamental Principle of Local Government Taxation - DomondonДокумент4 страницыFundamental Principle of Local Government Taxation - DomondonTimothy Mark MaderazoОценок пока нет

- Tax Ortega 1 Inno 2Документ24 страницыTax Ortega 1 Inno 2Timothy Mark MaderazoОценок пока нет

- Human Rights 461fgkmgfaДокумент73 страницыHuman Rights 461fgkmgfaTimothy Mark MaderazoОценок пока нет

- Torts - LotisДокумент234 страницыTorts - LotisTimothy Mark MaderazoОценок пока нет

- Docshare - Tips Pre Trial Brief Criminal SampleДокумент6 страницDocshare - Tips Pre Trial Brief Criminal SampleRegi Mabilangan ArceoОценок пока нет

- Absolute Community of Property VsДокумент5 страницAbsolute Community of Property VsTimothy Mark MaderazoОценок пока нет

- Labor 2 SyllabusДокумент12 страницLabor 2 SyllabusTimothy Mark MaderazoОценок пока нет

- Docshare - Tips Pre Trial Brief Criminal SampleДокумент6 страницDocshare - Tips Pre Trial Brief Criminal SampleRegi Mabilangan ArceoОценок пока нет

- Pre Trial BriefДокумент4 страницыPre Trial BriefTimothy Mark MaderazoОценок пока нет

- LLLДокумент2 страницыLLLTimothy Mark MaderazoОценок пока нет

- Andamo Vs IAC 191 SCRA 195Документ5 страницAndamo Vs IAC 191 SCRA 195JessicaОценок пока нет

- Maceda LawДокумент1 страницаMaceda LawAlverastine AnОценок пока нет

- Labor Relations - Assignment Cases1Документ49 страницLabor Relations - Assignment Cases1Timothy Mark MaderazoОценок пока нет

- LLLДокумент2 страницыLLLTimothy Mark MaderazoОценок пока нет

- Judicial Affidavit RuleДокумент4 страницыJudicial Affidavit RuleCaroline DulayОценок пока нет

- Abella. Vat 1Документ9 страницAbella. Vat 1Timothy Mark MaderazoОценок пока нет

- Effects of The Different Property Regimes in The Computation of The Estate TaxДокумент1 страницаEffects of The Different Property Regimes in The Computation of The Estate TaxTimothy Mark MaderazoОценок пока нет

- Wayne Brandt v. Board of Cooperative Educational Services, Third Supervisory District, Suffolk County, New York, Edward J. Murphy and Dominick Morreale, 820 F.2d 41, 2d Cir. (1987)Документ6 страницWayne Brandt v. Board of Cooperative Educational Services, Third Supervisory District, Suffolk County, New York, Edward J. Murphy and Dominick Morreale, 820 F.2d 41, 2d Cir. (1987)Scribd Government DocsОценок пока нет

- Loan AgreementДокумент2 страницыLoan AgreementElizabeth Fernandez-BenologaОценок пока нет

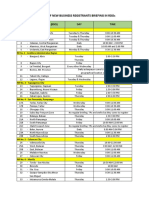

- Schedule of New Business Registrants Briefings by Revenue District OfficeДокумент4 страницыSchedule of New Business Registrants Briefings by Revenue District OfficeNarkSunderОценок пока нет

- LOGIC PROPOSITIONSДокумент6 страницLOGIC PROPOSITIONSSam BundalianОценок пока нет

- Legal Forms ReviewerДокумент3 страницыLegal Forms ReviewerAgripa, Kenneth Mar R.Оценок пока нет

- Rodriguez-Luna vs. Intermediate Appellate CourtДокумент7 страницRodriguez-Luna vs. Intermediate Appellate Courtvince005Оценок пока нет

- Castaneda v. AlemanyДокумент3 страницыCastaneda v. AlemanyDaley CatugdaОценок пока нет

- Yojana January 2024Документ64 страницыYojana January 2024ashish agrahariОценок пока нет

- 25 - Vda de Aviles V CAДокумент7 страниц25 - Vda de Aviles V CAgerlieОценок пока нет

- Standard Form of Agreement For Design ServicesДокумент80 страницStandard Form of Agreement For Design ServicesAIGA, the professional association for design100% (18)

- Saint Mary Crusade To Alleviate Poverty of Brethren Foundation, Inc. vs. RielДокумент12 страницSaint Mary Crusade To Alleviate Poverty of Brethren Foundation, Inc. vs. RielRaine VerdanОценок пока нет

- Cacho V CAДокумент11 страницCacho V CAGladys BantilanОценок пока нет

- Special Power of AttorneyДокумент1 страницаSpecial Power of AttorneyGerlin SentillasОценок пока нет

- Dela Victoria vs. Burgos (245 SCRA 374, 27 June 1995) G.R. No. 111190Документ9 страницDela Victoria vs. Burgos (245 SCRA 374, 27 June 1995) G.R. No. 111190Gendale Am-isОценок пока нет

- Heirs of Demetria Lacsa vs Court of AppealsДокумент2 страницыHeirs of Demetria Lacsa vs Court of AppealsJennilyn TugelidaОценок пока нет

- G.R. No. L-48594 March 16, 1988 GENEROSO ALANO, Petitioner, Employees' Compensation Commission, RespondentДокумент22 страницыG.R. No. L-48594 March 16, 1988 GENEROSO ALANO, Petitioner, Employees' Compensation Commission, RespondentHarry PeterОценок пока нет

- Lewis B. Sckolnick v. David R. Harlow, 820 F.2d 13, 1st Cir. (1987)Документ4 страницыLewis B. Sckolnick v. David R. Harlow, 820 F.2d 13, 1st Cir. (1987)Scribd Government DocsОценок пока нет

- CVNG 1012 Unit 1 Introduction To LawДокумент4 страницыCVNG 1012 Unit 1 Introduction To LawMarly MarlОценок пока нет

- Astm e 11 - 1995Документ7 страницAstm e 11 - 1995jaeyoungyoonОценок пока нет

- The Right To Privacy in The Philippines: Stakeholder Report Universal Periodic Review 27 Session - PhilippinesДокумент11 страницThe Right To Privacy in The Philippines: Stakeholder Report Universal Periodic Review 27 Session - PhilippinesJan. ReyОценок пока нет

- City's Anti-Crime Rewards ProgramДокумент5 страницCity's Anti-Crime Rewards ProgramTaraVamoose100% (1)

- KenyaRoadsAct No2of2007Документ408 страницKenyaRoadsAct No2of2007Boris MilochevОценок пока нет

- Law of Torts MCQ PaperДокумент16 страницLaw of Torts MCQ PaperBgmi PlayОценок пока нет

- DILG - Preparing and Updating The CDPДокумент108 страницDILG - Preparing and Updating The CDPErnest Belmes100% (2)

- TK8A50D Field Effect Transistor SpecificationsДокумент6 страницTK8A50D Field Effect Transistor Specifications劉毛毛Оценок пока нет

- CA Affirms RTC Ruling on Implied Admission Due to Failure to Respond to Request for AdmissionДокумент8 страницCA Affirms RTC Ruling on Implied Admission Due to Failure to Respond to Request for AdmissionIvan Montealegre ConchasОценок пока нет

- 12.09.2019 Proposal - Legal Memo and Tax StudyДокумент3 страницы12.09.2019 Proposal - Legal Memo and Tax StudyfortunecОценок пока нет

- Broker and Salesperson Agreement - Sample OnlyДокумент3 страницыBroker and Salesperson Agreement - Sample Onlychris ajero100% (4)

- Know Your Rights Brochure 0110Документ21 страницаKnow Your Rights Brochure 0110api-28723550Оценок пока нет

- Final Project of CompanyДокумент30 страницFinal Project of CompanySanni KumarОценок пока нет