Вам также может понравиться

- Partnership (Chapters 1-3)Документ22 страницыPartnership (Chapters 1-3)nicadagle1996Оценок пока нет

- Partnership LiquidationДокумент1 страницаPartnership LiquidationJo Vee VillanuevaОценок пока нет

- 3 ACCT 2A&B P. DissolutionДокумент10 страниц3 ACCT 2A&B P. DissolutionBrian Christian VillaluzОценок пока нет

- 1 - PDFsam - 01 Partnership - RetirementxxДокумент9 страниц1 - PDFsam - 01 Partnership - RetirementxxnashОценок пока нет

- Partnership DissolutionДокумент4 страницыPartnership DissolutionBianca IyiyiОценок пока нет

- Long Quiz - Ast - MarcellanaДокумент11 страницLong Quiz - Ast - MarcellanaMarcellana ArianeОценок пока нет

- Cpar AfarДокумент21 страницаCpar AfarFrancheska NadurataОценок пока нет

- Partnership HandoutsДокумент4 страницыPartnership Handoutsrose anne0% (1)

- Partnership Formation, Operation, Dissolution, and Liquidation by Lump Sum OnlyДокумент11 страницPartnership Formation, Operation, Dissolution, and Liquidation by Lump Sum OnlyJoyce Ann Cortez100% (2)

- 8901 - Partnership FormationДокумент3 страницы8901 - Partnership FormationRica Jane Santos Marcelo100% (1)

- Afar TestbankДокумент13 страницAfar TestbankRanie MonteclaroОценок пока нет

- PartnershipДокумент24 страницыPartnershipambi100% (4)

- Quiz-Chapter1 Partnership Formation and OperationsДокумент2 страницыQuiz-Chapter1 Partnership Formation and Operationsalellie100% (1)

- Afar-02: Partnership Dissolution & Liquidation: - T R S AДокумент12 страницAfar-02: Partnership Dissolution & Liquidation: - T R S AJenver Buenaventura100% (1)

- Notre Dame Educational Association: Purok San Jose, Brgy. New Isabela, Tacurong CityДокумент15 страницNotre Dame Educational Association: Purok San Jose, Brgy. New Isabela, Tacurong Cityirishjade100% (1)

- Partnership Problems Partnership Problems: Accountancy (La Consolacion College) Accountancy (La Consolacion College)Документ35 страницPartnership Problems Partnership Problems: Accountancy (La Consolacion College) Accountancy (La Consolacion College)Jay Ann DomeОценок пока нет

- Practical Accounting 2 First Pre-Board ExaminationДокумент15 страницPractical Accounting 2 First Pre-Board ExaminationKaren Eloisse89% (9)

- Multiple Choice Questions Variable vs. Absorption CostingДокумент106 страницMultiple Choice Questions Variable vs. Absorption CostingNicole CapundanОценок пока нет

- Partnership ExercisesДокумент35 страницPartnership ExercisesshiieeОценок пока нет

- Chapter 14 Partnerships Formation and OperationДокумент24 страницыChapter 14 Partnerships Formation and OperationJudith100% (5)

- Diagnostic Exam Partnership and CorporationДокумент10 страницDiagnostic Exam Partnership and CorporationMary Joyce GarciaОценок пока нет

- HQ01 Partnership Formation and OperationДокумент9 страницHQ01 Partnership Formation and OperationJean Ysrael Marquez50% (4)

- 4 InventoriesДокумент5 страниц4 InventoriesandreamrieОценок пока нет

- Business Combi TsetДокумент28 страницBusiness Combi Tsetsamuel debebeОценок пока нет

- HO2 Partnership Dissolution and Liquidation RevisedДокумент5 страницHO2 Partnership Dissolution and Liquidation RevisedChristianAquinoОценок пока нет

- Afar I. Partnership FormationДокумент4 страницыAfar I. Partnership FormationIrish SantiagoОценок пока нет

- Partnership Midterm Set BДокумент10 страницPartnership Midterm Set BLene100% (1)

- Quizzer PartnershipДокумент6 страницQuizzer PartnershipAdrianneHarve100% (2)

- Partnership Mock ExamДокумент15 страницPartnership Mock ExamPerbielyn BasinilloОценок пока нет

- Prequalifying ExaminationДокумент6 страницPrequalifying ExaminationVincent Villalino LabrintoОценок пока нет

- Cpa Review School of The Philippines ManilaДокумент4 страницыCpa Review School of The Philippines Manilaxara mizpahОценок пока нет

- 1 - PDFsam - 01 Partnership Formation & Admission of A Partnerxx PDFДокумент43 страницы1 - PDFsam - 01 Partnership Formation & Admission of A Partnerxx PDFnash67% (3)

- Problems - Partnership LiquidationДокумент8 страницProblems - Partnership LiquidationBrunxAlabastro56% (9)

- Partnership FormationДокумент2 страницыPartnership Formationlouise carinoОценок пока нет

- Partnership OperationДокумент3 страницыPartnership OperationBianca Iyiyi0% (1)

- Nature, Scope and Objectives PartnershipДокумент19 страницNature, Scope and Objectives PartnershipSol Luna100% (1)

- Partial Goodwill Full GoodwilДокумент38 страницPartial Goodwill Full GoodwilRose CastilloОценок пока нет

- Partnership Operations Lecture Notes2Документ7 страницPartnership Operations Lecture Notes2bum_24100% (8)

- FEU HO1 Audit of Inventories 2017 PDFДокумент4 страницыFEU HO1 Audit of Inventories 2017 PDFJoshuaОценок пока нет

- Quiz 1 AFAR ReviewДокумент7 страницQuiz 1 AFAR ReviewPrankyJellyОценок пока нет

- AFAR Assessment October 2020Документ8 страницAFAR Assessment October 2020FelixОценок пока нет

- Practical Accounting 2Документ12 страницPractical Accounting 2jaysonОценок пока нет

- AfarДокумент3 страницыAfarDanielle Nicole MarquezОценок пока нет

- FORMATIONДокумент2 страницыFORMATIONBianca IyiyiОценок пока нет

- Toaz - Info Afar PRДокумент95 страницToaz - Info Afar PRMiraflor Sanchez BiñasОценок пока нет

- (At) 01 - Preface, Framework, EtcДокумент8 страниц(At) 01 - Preface, Framework, EtcCykee Hanna Quizo LumongsodОценок пока нет

- Partnership Liquidation InstallmentДокумент1 страницаPartnership Liquidation InstallmentAkira Marantal ValdezОценок пока нет

- Partnership Liquidation QuizДокумент5 страницPartnership Liquidation QuizAlexis TRADIO100% (1)

- Ra 9298 Accountancy Act of 2004Документ10 страницRa 9298 Accountancy Act of 2004Jerome Reyes100% (1)

- ACCTG 7 - Final Exam V2Документ10 страницACCTG 7 - Final Exam V2Sarah Balisacan0% (2)

- Partnership TheoriesДокумент5 страницPartnership TheoriesThomas MarianoОценок пока нет

- Afar PartnershipДокумент6 страницAfar PartnershipSheena Baylosis0% (1)

- Business CombinationДокумент7 страницBusiness CombinationJae DenОценок пока нет

- CORPORATIONEXERCISES28PROBLEMS29ONORGANIZATION21FEB21Документ5 страницCORPORATIONEXERCISES28PROBLEMS29ONORGANIZATION21FEB21Jasmine Acta0% (1)

- 1st PREBOARD EXAMINATION - AFAR STUDENTS PDFДокумент16 страниц1st PREBOARD EXAMINATION - AFAR STUDENTS PDFAAОценок пока нет

- Partnerships: Formation, Operation, and Ownership Changes: Multiple ChoiceДокумент20 страницPartnerships: Formation, Operation, and Ownership Changes: Multiple ChoiceLester AlpanoОценок пока нет

- Partnership Liquidation: Multiple ChoiceДокумент23 страницыPartnership Liquidation: Multiple ChoiceIvhy Cruz EstrellaОценок пока нет

- Chapter 15Документ16 страницChapter 15kylicia bestОценок пока нет

- Jeter and Channey Advacc PDFДокумент21 страницаJeter and Channey Advacc PDFElaine YapОценок пока нет

- ch09 1Документ20 страницch09 1Celestaire LeeОценок пока нет

- PartnershipДокумент43 страницыPartnershipIvhy Cruz EstrellaОценок пока нет

- Relevant CostДокумент12 страницRelevant CostIvhy Cruz EstrellaОценок пока нет

- Ch15 Beams10e TBДокумент22 страницыCh15 Beams10e TBIm In Trouble50% (4)

- AFARrДокумент989 страницAFARrIvhy Cruz Estrella100% (1)

- S C-Test Bank-Income TaxationДокумент135 страницS C-Test Bank-Income TaxationRoselie Barbin47% (19)

- Partnership Liquidation: Multiple ChoiceДокумент23 страницыPartnership Liquidation: Multiple ChoiceIvhy Cruz EstrellaОценок пока нет

- 100 MCQ NegoДокумент12 страниц100 MCQ NegoDaphneОценок пока нет

- Chap 9 PartnershipДокумент77 страницChap 9 PartnershipIvhy Cruz EstrellaОценок пока нет

- NegoДокумент6 страницNegoIvhy Cruz EstrellaОценок пока нет

- Chapter 9 Ed 16Документ73 страницыChapter 9 Ed 16Ivhy Cruz Estrella100% (1)

- Chapter 17 Test BankДокумент29 страницChapter 17 Test BankIvhy Cruz Estrella100% (1)

- Test Bank - Chapter14 Capital BudgetingДокумент35 страницTest Bank - Chapter14 Capital BudgetingAiko E. Lara100% (8)

- CPAR MAS Preweek - May 2005 EditionДокумент47 страницCPAR MAS Preweek - May 2005 EditionIvhy Cruz Estrella100% (5)

- CH 07Документ72 страницыCH 07Ivhy Cruz Estrella100% (1)

- Chap 10 PartnershipДокумент24 страницыChap 10 PartnershipIvhy Cruz Estrella100% (2)

- CH 07Документ63 страницыCH 07Ivhy Cruz Estrella100% (5)

- Advanced Accounting Baker Test Bank - Chap016Документ55 страницAdvanced Accounting Baker Test Bank - Chap016donkazotey93% (14)

- Afar 19Документ20 страницAfar 19Ivhy Cruz EstrellaОценок пока нет

- Afar 17Документ19 страницAfar 17Ivhy Cruz EstrellaОценок пока нет

- Audit Program-Long Term DebtДокумент11 страницAudit Program-Long Term DebtRoemi Rivera Robedizo100% (3)

- The Effects of Changes in Foreign Rates: ExchangeДокумент50 страницThe Effects of Changes in Foreign Rates: ExchangeBethelhem50% (2)

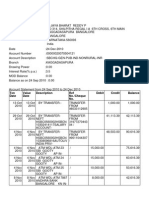

- TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceДокумент4 страницыTXN Date Value Date Description Ref No./Cheque No. Debit Credit Balanceswetha_muthumulaОценок пока нет

- Acctng Mod 2Документ6 страницAcctng Mod 2viaishere4uОценок пока нет

- New Syllabus For Foundation ProgrammeДокумент6 страницNew Syllabus For Foundation ProgrammeAnonymous Sc4K4rQ3UОценок пока нет

- List of Accounts Submitted To Audit (P.W.A. Code Paragraphs 523 and 527)Документ2 страницыList of Accounts Submitted To Audit (P.W.A. Code Paragraphs 523 and 527)Muhammad Ishaq ZahidОценок пока нет

- Financial Accounting 2 Reviewer Part 1Документ20 страницFinancial Accounting 2 Reviewer Part 1monne100% (5)

- Multiple Choices - Theoretical: Chapter 3: Storing and Issuing MaterialsДокумент23 страницыMultiple Choices - Theoretical: Chapter 3: Storing and Issuing MaterialsRenz Alconera100% (2)

- Reviewer Cost PrelimsДокумент10 страницReviewer Cost PrelimsClarence John G. BelzaОценок пока нет

- 2 Statement of Financial PositionДокумент7 страниц2 Statement of Financial Positionreagan blaireОценок пока нет

- QUESTION BANK Class 11Документ87 страницQUESTION BANK Class 11puja bhardwajОценок пока нет

- Sikkim University ERP RFPДокумент38 страницSikkim University ERP RFPSreenivasa AkshinthalaОценок пока нет

- 3456782345Документ17 страниц3456782345Jade MarkОценок пока нет

- Oracle AR Credit Card Issue SetupsДокумент21 страницаOracle AR Credit Card Issue SetupsMag Marina50% (2)

- Tle CBRCДокумент19 страницTle CBRCHazel Grace S. Ortigoza100% (2)

- File Layouts V1.0Документ186 страницFile Layouts V1.0ravikiran30Оценок пока нет

- P S4FIN 1610 Model QuestionДокумент85 страницP S4FIN 1610 Model QuestionNannbaa MynameОценок пока нет

- ASE20091 Mark Scheme September 2019Документ16 страницASE20091 Mark Scheme September 2019Bunny DomeОценок пока нет

- Credit Terms and Conditions of Sale AssignmentДокумент4 страницыCredit Terms and Conditions of Sale AssignmentRoger RogerОценок пока нет

- ExplanationsДокумент2 страницыExplanationsLovely Rose LacuataОценок пока нет

- Question Bank-On MBA SubjectsДокумент100 страницQuestion Bank-On MBA SubjectsPriyanka SinghОценок пока нет

- Advanced Financial Accounting 1Документ12 страницAdvanced Financial Accounting 1Gemine Ailna Panganiban NuevoОценок пока нет

- Cash and ReceivablesДокумент6 страницCash and ReceivablesNylan AnyerОценок пока нет

- Sos - October 2018Документ26 страницSos - October 2018Lilia Villarin DoradoОценок пока нет

- Closing EntriesДокумент10 страницClosing EntriesFranco DexterОценок пока нет

- Cambridge International General Certificate of Secondary EducationДокумент10 страницCambridge International General Certificate of Secondary EducationCikgu kannaОценок пока нет

- Unit 1 Challenge 1: D.) Unethical Behavior by Major Companies Prompted The Government To Create The Sarbanes-Oxley ActДокумент16 страницUnit 1 Challenge 1: D.) Unethical Behavior by Major Companies Prompted The Government To Create The Sarbanes-Oxley ActMeredith Eckard100% (1)

- Working Capital ManagementДокумент75 страницWorking Capital ManagementShadab Khan100% (1)

- Accounting Principles: The Recording ProcessДокумент51 страницаAccounting Principles: The Recording ProcessS. M. Fahmidunnabi 2035150660Оценок пока нет

- 10 - THESIS OUTLINE - SALES and INCOME SUMARYДокумент5 страниц10 - THESIS OUTLINE - SALES and INCOME SUMARYPhuc Hoang DuongОценок пока нет