Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Lec 24 B Wrap Up ValuationДокумент37 страницLec 24 B Wrap Up ValuationserpepeОценок пока нет

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Bai Tap TcdnACP4EA (J) 13 - LowresДокумент14 страницBai Tap TcdnACP4EA (J) 13 - LowresAn HoàiОценок пока нет

- CApital Structure and LeverageДокумент33 страницыCApital Structure and LeverageMD Rifat ZahirОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Business PlansДокумент51 страницаBusiness PlansSandip GhoshОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Phan Phoi Co Tuc Cuc Hay CH 19 (Online) - Accepted PDFДокумент46 страницPhan Phoi Co Tuc Cuc Hay CH 19 (Online) - Accepted PDFAn HoàiОценок пока нет

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- pp20Документ44 страницыpp20An HoàiОценок пока нет

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- 14Документ69 страниц14Shoniqua Johnson100% (2)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Chapter 17Документ37 страницChapter 17Kad Saad100% (2)

- Marketing Case Studies CataloguesДокумент67 страницMarketing Case Studies Cataloguespanashe1275% (4)

- HRSP Condensed - FinalДокумент16 страницHRSP Condensed - FinalAn HoàiОценок пока нет

- 80 VCD English For YouДокумент4 страницы80 VCD English For YouAn Hoài100% (1)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Investment AnalysisДокумент10 страницInvestment AnalysisAn HoàiОценок пока нет

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- TL Tap Huan BhytДокумент23 страницыTL Tap Huan BhytAn HoàiОценок пока нет

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- ln8 QTRRRCДокумент46 страницln8 QTRRRCAn HoàiОценок пока нет

- The Valuation and Characteristics of Stock: (Ch. 7 in 4 Edition)Документ47 страницThe Valuation and Characteristics of Stock: (Ch. 7 in 4 Edition)An HoàiОценок пока нет

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Accounting Ratios: Inancial Statements Aim at Providing FДокумент47 страницAccounting Ratios: Inancial Statements Aim at Providing Fabc100% (1)

- Brooks PP CH 7 RTPДокумент48 страницBrooks PP CH 7 RTPAn HoàiОценок пока нет

- 205417quan Tri Danh Muc CatologeДокумент81 страница205417quan Tri Danh Muc CatologeAn HoàiОценок пока нет

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- FTSE UK Index Series Guide To CalcДокумент16 страницFTSE UK Index Series Guide To CalcAn HoàiОценок пока нет

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Calculations For Time Value of Money: T F V S SДокумент8 страницCalculations For Time Value of Money: T F V S SAn HoàiОценок пока нет

- 1 OnlinepublicationДокумент1 страница1 OnlinepublicationAn HoàiОценок пока нет

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Motivating The Channel Members: Chapter ObjectivesДокумент6 страницMotivating The Channel Members: Chapter ObjectivesAn HoàiОценок пока нет

- Chapter 12 0Документ9 страницChapter 12 0An HoàiОценок пока нет

- Solutions To End-of-Chapter Three ProblemsДокумент13 страницSolutions To End-of-Chapter Three ProblemsAn HoàiОценок пока нет

- 財管Ch16解答Документ12 страниц財管Ch16解答An HoàiОценок пока нет

- Vsm812s Chapter 5Документ42 страницыVsm812s Chapter 5An HoàiОценок пока нет

- ch20Документ59 страницch20An Hoài100% (1)

- Chapter15 New Thuc Hanh Gia PDFДокумент33 страницыChapter15 New Thuc Hanh Gia PDFAn HoàiОценок пока нет

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Brooks PP CH 9 RTPДокумент53 страницыBrooks PP CH 9 RTPAn HoàiОценок пока нет

- Finance Case Studies With Solutions PDFДокумент3 страницыFinance Case Studies With Solutions PDFAn Hoài33% (15)

- Project Profile: M/S Ragini Kirana Store (Prop Upendra Yadav)Документ18 страницProject Profile: M/S Ragini Kirana Store (Prop Upendra Yadav)Satendra DhakarОценок пока нет

- Additional Bank Recon QuestionsДокумент4 страницыAdditional Bank Recon QuestionsDebbie DebzОценок пока нет

- Accounting Concepts and PrinciplesДокумент8 страницAccounting Concepts and PrinciplesNikki BalsinoОценок пока нет

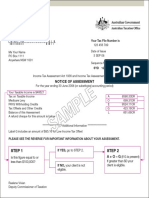

- Step 1 Step 2: Notice of AssessmentДокумент1 страницаStep 1 Step 2: Notice of Assessmentabinash manandharОценок пока нет

- A. Under Statement of Financial Position: Typical Account Titles UsedДокумент6 страницA. Under Statement of Financial Position: Typical Account Titles UsedAshlyn MaeОценок пока нет

- Cash and Cash Equivalents SummaryДокумент2 страницыCash and Cash Equivalents SummaryJulienne UntalascoОценок пока нет

- Annual Report-2076-77 PDFДокумент228 страницAnnual Report-2076-77 PDFAbhishek ChaurasiyaОценок пока нет

- Investment Environment and Investment Management Process-1Документ1 страницаInvestment Environment and Investment Management Process-1CalvinsОценок пока нет

- Part F - Additional QuestionsДокумент9 страницPart F - Additional QuestionsDesmond Grasie ZumankyereОценок пока нет

- Auditing Finance and Accounting FunctionsДокумент14 страницAuditing Finance and Accounting FunctionsApril ManjaresОценок пока нет

- Model Asset and Liability Affidavit D. VДокумент12 страницModel Asset and Liability Affidavit D. VsavagecommentorОценок пока нет

- Quantitative Problems Chapter 5Документ5 страницQuantitative Problems Chapter 5Fatima Sabir Masood Sabir ChaudhryОценок пока нет

- CPP EI IT CalculationДокумент4 страницыCPP EI IT CalculationirfanОценок пока нет

- Cancellation Acord Form - CX149661-Ramon Aguilar-Aguila Trucking PDFДокумент1 страницаCancellation Acord Form - CX149661-Ramon Aguilar-Aguila Trucking PDFBryan ArenasОценок пока нет

- Banks - Sector Update - 22 Dec 21Документ86 страницBanks - Sector Update - 22 Dec 21Kaushal ShahОценок пока нет

- Lira District Report of The Auditor General 2015 PDFДокумент59 страницLira District Report of The Auditor General 2015 PDFlutos2Оценок пока нет

- Working Capital Management Maruti SuzukiДокумент76 страницWorking Capital Management Maruti SuzukiAbhay Gupta81% (32)

- Genet Tadesse - A Small Business Borrower in EthiopiaДокумент2 страницыGenet Tadesse - A Small Business Borrower in EthiopiaWedpPepeОценок пока нет

- 04 QuestionsДокумент7 страниц04 QuestionsfaizthemeОценок пока нет

- Role of Merchant BsnkingДокумент7 страницRole of Merchant BsnkingKishor BiswasОценок пока нет

- 4 Capital Budgeting PDFДокумент45 страниц4 Capital Budgeting PDFmichael christianОценок пока нет

- Topic 14 - Estate PlanningДокумент57 страницTopic 14 - Estate PlanningArun GhatanОценок пока нет

- 2316 Jan 2018 ENCS FinalДокумент2 страницы2316 Jan 2018 ENCS FinalKirsten Bairan100% (2)

- What Is A BCG Growth-Share Matrix?: Minglana, Mitch T. BSA 201Документ3 страницыWhat Is A BCG Growth-Share Matrix?: Minglana, Mitch T. BSA 201Mitch Tokong MinglanaОценок пока нет

- Government Finance Statistics (GFSX) : Valuation of TransactionsДокумент2 страницыGovernment Finance Statistics (GFSX) : Valuation of TransactionsKhenneth BalcetaОценок пока нет

- 14643post 819 WircДокумент945 страниц14643post 819 WircRonak ShahОценок пока нет

- Infra Finance Role Campus JDДокумент3 страницыInfra Finance Role Campus JDJohn DoeОценок пока нет

- Afar 02 P'ship Operation QuizДокумент4 страницыAfar 02 P'ship Operation QuizJohn Laurence LoplopОценок пока нет

- 1 Point: Failure of Rakham To Collect The Debt Within Three Years From The Date It Becomes DueДокумент17 страниц1 Point: Failure of Rakham To Collect The Debt Within Three Years From The Date It Becomes DueClarince Joyce Lao DoroyОценок пока нет

- PT Zalia Cash Receipts JournalДокумент8 страницPT Zalia Cash Receipts Journalsovia deviОценок пока нет

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)От EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Рейтинг: 4.5 из 5 звезд4.5/5 (13)

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)От EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Рейтинг: 4 из 5 звезд4/5 (33)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindОт EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindРейтинг: 5 из 5 звезд5/5 (231)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!От EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Рейтинг: 4.5 из 5 звезд4.5/5 (14)

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsОт EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsРейтинг: 5 из 5 звезд5/5 (1)

- Getting to Yes: How to Negotiate Agreement Without Giving InОт EverandGetting to Yes: How to Negotiate Agreement Without Giving InРейтинг: 4 из 5 звезд4/5 (652)

- The Credit Formula: The Guide To Building and Rebuilding Lendable CreditОт EverandThe Credit Formula: The Guide To Building and Rebuilding Lendable CreditРейтинг: 5 из 5 звезд5/5 (1)