Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Rain Industries: CMP: INR381 TP: INR480 (+26%) Carbon Prices and Margins Continue To ImproveДокумент8 страницRain Industries: CMP: INR381 TP: INR480 (+26%) Carbon Prices and Margins Continue To ImprovedidwaniasОценок пока нет

- Rbi Allowed Banks To Increase Limit From 10 To 15 PercentДокумент10 страницRbi Allowed Banks To Increase Limit From 10 To 15 PercentdidwaniasОценок пока нет

- BandhanBank 15 3 18 PLДокумент1 страницаBandhanBank 15 3 18 PLdidwaniasОценок пока нет

- Idfc QTR FinancialsДокумент2 страницыIdfc QTR FinancialsdidwaniasОценок пока нет

- APL Apollo Antique Stock Broking Coverage Aprl 17Документ17 страницAPL Apollo Antique Stock Broking Coverage Aprl 17didwaniasОценок пока нет

- MARKET ESTIMATES FOR Sep, 2008 Results To Be Announced TodayДокумент2 страницыMARKET ESTIMATES FOR Sep, 2008 Results To Be Announced TodaydidwaniasОценок пока нет

- Information Technology: Covid-19, Oil Price Dip To Pose Near Term HeadwindsДокумент8 страницInformation Technology: Covid-19, Oil Price Dip To Pose Near Term HeadwindsdidwaniasОценок пока нет

- Industry Report Card April 2018Документ16 страницIndustry Report Card April 2018didwaniasОценок пока нет

- 0hsie F PDFДокумент416 страниц0hsie F PDFchemkumar16Оценок пока нет

- Weekly Technical PicksДокумент4 страницыWeekly Technical PicksMaruthee SharmaОценок пока нет

- Sensex AnalysisДокумент2 страницыSensex AnalysisdidwaniasОценок пока нет

- Bandhan Bank Building Strong Franchise Through Retail FocusДокумент13 страницBandhan Bank Building Strong Franchise Through Retail FocusdidwaniasОценок пока нет

- IDEA One PagerДокумент6 страницIDEA One PagerdidwaniasОценок пока нет

- Financials 7-11-08Документ6 страницFinancials 7-11-08didwaniasОценок пока нет

- Sponge Iron Industry B K Oct 06 PDFДокумент30 страницSponge Iron Industry B K Oct 06 PDFdidwaniasОценок пока нет

- Mawana FinancialsДокумент8 страницMawana FinancialsdidwaniasОценок пока нет

- IFLEX One PagerДокумент1 страницаIFLEX One PagerdidwaniasОценок пока нет

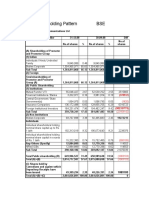

- Shareholding Pattern BSEДокумент3 страницыShareholding Pattern BSEdidwaniasОценок пока нет

- BHEL One PagerДокумент1 страницаBHEL One PagerdidwaniasОценок пока нет

- 24 Jun 08 - BHELДокумент4 страницы24 Jun 08 - BHELdidwaniasОценок пока нет

- HSBC Private Bank Strategy MattersДокумент4 страницыHSBC Private Bank Strategy MattersdidwaniasОценок пока нет

- 'A' Grade Turnaround: Associated Cement CompaniesДокумент3 страницы'A' Grade Turnaround: Associated Cement CompaniesdidwaniasОценок пока нет

- Citizens Guide 2008Документ12 страницCitizens Guide 2008DeliajrsОценок пока нет

- The Subprime Meltdown: Understanding Accounting-Related AllegationsДокумент7 страницThe Subprime Meltdown: Understanding Accounting-Related AllegationsdidwaniasОценок пока нет

- IAG+ +India+Strategy+ (June+08)Документ17 страницIAG+ +India+Strategy+ (June+08)api-3862995Оценок пока нет

- Sanjiv KaulДокумент18 страницSanjiv KaulsdОценок пока нет

- IAG+ +India+Strategy+ (June+08)Документ17 страницIAG+ +India+Strategy+ (June+08)api-3862995Оценок пока нет

- Income & Growth One Pager 06302008Документ2 страницыIncome & Growth One Pager 06302008didwaniasОценок пока нет

- CKP PresentationДокумент39 страницCKP PresentationdidwaniasОценок пока нет

- Kpo VsbpoДокумент3 страницыKpo VsbposdОценок пока нет

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Importance of Stock MarketДокумент4 страницыImportance of Stock MarketRajdeep KaurОценок пока нет

- A Report On The Indian Exchange Traded Funds (ETF) IndustryДокумент26 страницA Report On The Indian Exchange Traded Funds (ETF) IndustryHitendra PanchalОценок пока нет

- HDFC Mutual FundДокумент93 страницыHDFC Mutual FundKomal MansukhaniОценок пока нет

- Exchange Traded Funds (Etfs) What Is An Etf?Документ3 страницыExchange Traded Funds (Etfs) What Is An Etf?RahulОценок пока нет

- FDI Impact on Indian Airline IndustryДокумент45 страницFDI Impact on Indian Airline IndustryVaibhav BhadauriaОценок пока нет

- Tourism PlanningДокумент14 страницTourism PlanningAsiful AlamОценок пока нет

- Corporate Governance & Business EthicsДокумент79 страницCorporate Governance & Business EthicsRishi Ahuja0% (1)

- #Stock Trading SecretsДокумент40 страниц#Stock Trading Secretsmatsumoto100% (2)

- FM&SДокумент18 страницFM&SVinay Gowda D MОценок пока нет

- Chapter 9 Project Cash FlowsДокумент28 страницChapter 9 Project Cash FlowsGovinda AgrawalОценок пока нет

- Lecture 4 - ReformattingДокумент31 страницаLecture 4 - ReformattingnopeОценок пока нет

- Fundamental Analysis of Banking Industry in IndiaДокумент42 страницыFundamental Analysis of Banking Industry in IndiaGurpreet Kaur86% (7)

- SOURAV'S SIP ON SBI MUTUAL FUND (Introduction)Документ106 страницSOURAV'S SIP ON SBI MUTUAL FUND (Introduction)sourabha86100% (1)

- Importance of Descriptive Statistics For Business Decision Making.Документ7 страницImportance of Descriptive Statistics For Business Decision Making.Lasitha NawarathnaОценок пока нет

- Tax Incentives G. 07 BsДокумент10 страницTax Incentives G. 07 BsLevenson KadegheОценок пока нет

- Journal (Jaya College) - Investment Awareness of Working Women Investors in Chennai CityДокумент12 страницJournal (Jaya College) - Investment Awareness of Working Women Investors in Chennai CityMythili Karthikeyan100% (1)

- Sukuk vs. Bonds: Stock ReactionДокумент17 страницSukuk vs. Bonds: Stock ReactionWasim ShahОценок пока нет

- Mutual Fund Analysis ComparisonДокумент76 страницMutual Fund Analysis ComparisonsantoshbansodeОценок пока нет

- Assign No 5 - OpleДокумент3 страницыAssign No 5 - OpleLester Nazarene OpleОценок пока нет

- Venture Capital - Fund Raising and Fund StructureДокумент52 страницыVenture Capital - Fund Raising and Fund StructureSimon ChenОценок пока нет

- Akash CPДокумент48 страницAkash CPEr Aks PatelОценок пока нет

- Bse Trading SystemДокумент4 страницыBse Trading SystemRaman Kumar67% (3)

- The Stock Market For DummiesДокумент2 страницыThe Stock Market For DummiesjikolpОценок пока нет

- ANAND-RATHI Tanuj Kumar ProjectДокумент90 страницANAND-RATHI Tanuj Kumar ProjectTanuj Kumar50% (2)

- SEBI Regulations Explained in 40 CharactersДокумент19 страницSEBI Regulations Explained in 40 CharactersMurugesh KumarОценок пока нет

- JPM Private BankДокумент31 страницаJPM Private BankZerohedge100% (2)

- Political Risk Factors and TheirДокумент21 страницаPolitical Risk Factors and TheircrsalinasОценок пока нет

- Enigma Case StudyДокумент7 страницEnigma Case Studyutkarsh bhargavaОценок пока нет

- Chapter 004 F2009Документ7 страницChapter 004 F2009mallumainhunmailОценок пока нет

- BS NOTES Kombaz-1Документ331 страницаBS NOTES Kombaz-1tiller kambanjeОценок пока нет