Вам также может понравиться

- Citzn CHTR eДокумент5 страницCitzn CHTR eBanavaram UmapathiОценок пока нет

- Quarantining Illicit TobaccoДокумент19 страницQuarantining Illicit TobaccoTobacco IndustryОценок пока нет

- Customs Customs Administration Modernization Project (CAM-1)Документ6 страницCustoms Customs Administration Modernization Project (CAM-1)khshiblyОценок пока нет

- 3.2 Eduardo Jimenez - OECD - VAT - ENGДокумент15 страниц3.2 Eduardo Jimenez - OECD - VAT - ENGMaria Ximena Lopez DominguezОценок пока нет

- Legal Metrology Awareness Campaign and Public Participation 2014 Edited LMДокумент17 страницLegal Metrology Awareness Campaign and Public Participation 2014 Edited LMJoe MaharajОценок пока нет

- Se BДокумент1 страницаSe B22-0188cОценок пока нет

- Analytics COI Compendium of Project Abstracts 2018Документ115 страницAnalytics COI Compendium of Project Abstracts 2018John KimutaiОценок пока нет

- Taxation International Taxation E-Commerce Issues in Cyber SpaceДокумент73 страницыTaxation International Taxation E-Commerce Issues in Cyber SpaceAmit KumarОценок пока нет

- Foreword: Central Board of Excise and CustomsДокумент9 страницForeword: Central Board of Excise and CustomshydexcustОценок пока нет

- Modalities For Importation of Goods and IncentivesДокумент4 страницыModalities For Importation of Goods and IncentivesState House NigeriaОценок пока нет

- UNIT 5 - Recent Trends in AuditingДокумент11 страницUNIT 5 - Recent Trends in AuditingNeetika Chawla100% (4)

- Discussion Paper On Value Added Tax Modernisation 16205Документ12 страницDiscussion Paper On Value Added Tax Modernisation 16205Tiaan SmitОценок пока нет

- Accreditation of Paying Agencies Controlling Agricultural ExpenditureДокумент22 страницыAccreditation of Paying Agencies Controlling Agricultural ExpenditureIvana ZlatanovićОценок пока нет

- Chapter 8 Systems and ControlsДокумент4 страницыChapter 8 Systems and Controlsrishi kareliaОценок пока нет

- Wright A Comprehensive and Summarized Note About, Tax Audit Techniques in Ethiopia For Manufacturing, Merchandising and Service Business. 1.1auditingДокумент9 страницWright A Comprehensive and Summarized Note About, Tax Audit Techniques in Ethiopia For Manufacturing, Merchandising and Service Business. 1.1auditingGEREMEW ADEREОценок пока нет

- 7.5 Chinese Taipei - Case Study of Customs Post-Clearance Audit System by Chinese TaipeiДокумент7 страниц7.5 Chinese Taipei - Case Study of Customs Post-Clearance Audit System by Chinese TaipeiRuwen Joice Abacan BunquinОценок пока нет

- Practical - 10Документ5 страницPractical - 10Priyanshu ChaubeyОценок пока нет

- CH13 and 14: November 29, 2022 3:26 PMДокумент6 страницCH13 and 14: November 29, 2022 3:26 PMdre thegreatОценок пока нет

- CH8 - Internal Control SystemsДокумент6 страницCH8 - Internal Control SystemsGrigoras Alexandru NicolaeОценок пока нет

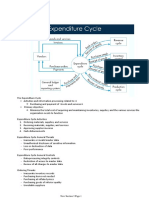

- The Expenditure CycleДокумент8 страницThe Expenditure Cyclemoknetone100% (1)

- Chapter 8. Other StandardsДокумент40 страницChapter 8. Other StandardsАйбар КарабековОценок пока нет

- Acc231 - CH 1Документ16 страницAcc231 - CH 1alaamabood6Оценок пока нет

- Auditing and Internal Control: Prepared By: Ambrocio, Sheila Mae BДокумент31 страницаAuditing and Internal Control: Prepared By: Ambrocio, Sheila Mae BLeslie DiamondОценок пока нет

- CT Pat Human ResourceДокумент23 страницыCT Pat Human Resourcedinesh_haiОценок пока нет

- 7 Chapter07Документ24 страницы7 Chapter07Kalkidan ZerihunОценок пока нет

- Ctpat April 2014Документ39 страницCtpat April 2014vcespedespОценок пока нет

- 톰슨로이터 간접세 솔루션 - - 20120409Документ20 страниц톰슨로이터 간접세 솔루션 - - 20120409Sunggyun ChoОценок пока нет

- Elements of Supply Chain MGT 1. Procurement (Contd)Документ36 страницElements of Supply Chain MGT 1. Procurement (Contd)HaadОценок пока нет

- ch07 Godfrey Teori AkuntansiДокумент34 страницыch07 Godfrey Teori Akuntansiuphevanbogs100% (2)

- Audit PlanningДокумент12 страницAudit Planningsadananda52Оценок пока нет

- Class Notes - Challenges & Factor Driving LogesticsДокумент17 страницClass Notes - Challenges & Factor Driving LogesticsSohail Wahab (E&I)Оценок пока нет

- Comodities and Supplies Management For ElearningДокумент18 страницComodities and Supplies Management For Elearningemmanuelgk100Оценок пока нет

- Controlling Information Systems: Introduction To Internal ControlДокумент29 страницControlling Information Systems: Introduction To Internal ControlPeishi OngОценок пока нет

- Icc CTC Practiceprinciples 2020Документ5 страницIcc CTC Practiceprinciples 2020Max muster WoodОценок пока нет

- PT 3 AccountingДокумент19 страницPT 3 AccountingYzzabel Denise L. TolentinoОценок пока нет

- India Direct Tax - Changes & ImpactДокумент5 страницIndia Direct Tax - Changes & ImpactPiyush MittalОценок пока нет

- Auditing IT (F)Документ39 страницAuditing IT (F)Abdulkarim Hamisi KufakunogaОценок пока нет

- Management Accounting:: Major Differences: Legal Requirements, Focus On, Bodies, Time Dimension, Report FrequencyДокумент2 страницыManagement Accounting:: Major Differences: Legal Requirements, Focus On, Bodies, Time Dimension, Report FrequencyOlga SîrbuОценок пока нет

- Country Presentation Customs KenyaДокумент5 страницCountry Presentation Customs KenyavictormathaiyaОценок пока нет

- Production Cycle ReportingДокумент6 страницProduction Cycle ReportingAira Jaimee GonzalesОценок пока нет

- What'SCost AccountingДокумент4 страницыWhat'SCost AccountingLeno MathewОценок пока нет

- Qualified PersonДокумент23 страницыQualified PersonMorcos LokaОценок пока нет

- Assignment On: Public Finance For Bangladesh PerspectiveДокумент6 страницAssignment On: Public Finance For Bangladesh PerspectiveNazib UllahОценок пока нет

- Chapter - I 2009Документ39 страницChapter - I 2009Gemechu JebesaОценок пока нет

- Bản Sao Của Compliance AuditДокумент5 страницBản Sao Của Compliance Auditqgminh7114Оценок пока нет

- Audit and Assurance - Logistics and TransportationДокумент22 страницыAudit and Assurance - Logistics and TransportationJohann Villegas67% (3)

- Fkakasa BookletДокумент8 страницFkakasa BookletLaban Lakers PhilclaraОценок пока нет

- Rmo 5 2012Документ2 страницыRmo 5 2012Denver TanhuanОценок пока нет

- Information Technology (IT) AuditДокумент31 страницаInformation Technology (IT) AuditCharmaine ChuaОценок пока нет

- Trabajo InglesДокумент3 страницыTrabajo Inglesshalom mendozaОценок пока нет

- Navigating The Complexities of Tax LawДокумент2 страницыNavigating The Complexities of Tax LawReign Dela CruzОценок пока нет

- Conceptualization of Trade FacilitationДокумент13 страницConceptualization of Trade FacilitationK59 TRAN VY TRAОценок пока нет

- AMITY Business School: Cost Accounting Nupur AgarwalДокумент41 страницаAMITY Business School: Cost Accounting Nupur AgarwalNupur AgarwalОценок пока нет

- CIS MidtermsДокумент42 страницыCIS MidtermsKM MacatangayОценок пока нет

- IPP Audit PlanДокумент6 страницIPP Audit PlanRuwan GunarathnaОценок пока нет

- Accounting Information SystemsДокумент46 страницAccounting Information SystemsSuptoОценок пока нет

- Key Features of Foreign Trade PolicyДокумент6 страницKey Features of Foreign Trade PolicyastikdubeyОценок пока нет

- Audit Risk Alert: Government Auditing Standards and Single Audit Developments: Strengthening Audit Integrity 2018/19От EverandAudit Risk Alert: Government Auditing Standards and Single Audit Developments: Strengthening Audit Integrity 2018/19Оценок пока нет

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsОт EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsРейтинг: 5 из 5 звезд5/5 (1)

- Audit Risk Alert: General Accounting and Auditing Developments 2018/19От EverandAudit Risk Alert: General Accounting and Auditing Developments 2018/19Оценок пока нет

- Company Profile Bureau Veritas ThailandДокумент13 страницCompany Profile Bureau Veritas ThailandPitichai PakornrersiriОценок пока нет

- Stainless Tubing in BiotechДокумент14 страницStainless Tubing in BiotechClaudia MmsОценок пока нет

- TRIAS - Master ProposalДокумент12 страницTRIAS - Master ProposalHafidGaneshaSecretrdreamholicОценок пока нет

- ZF 2000 Series: Product DetailsДокумент4 страницыZF 2000 Series: Product DetailsJhonAlexRiveroОценок пока нет

- Training Wall Height On Convergent Stepped SpillwaysДокумент10 страницTraining Wall Height On Convergent Stepped Spillwayschutton681Оценок пока нет

- Big Breakfasts Help Us Burn Double The CaloriesДокумент4 страницыBig Breakfasts Help Us Burn Double The CaloriesBastian IgnacioОценок пока нет

- Entrepreneurship in The PhilippinesДокумент7 страницEntrepreneurship in The Philippinesjoanne rivera100% (1)

- NCQCДокумент73 страницыNCQCSaurabh Jaiswal JassiОценок пока нет

- Interdependence and The Gains From TradeДокумент30 страницInterdependence and The Gains From TradeAnusree P hs20h011Оценок пока нет

- 10.1007@s10157 020 01867 yДокумент6 страниц10.1007@s10157 020 01867 yGin RummyОценок пока нет

- Live IT Oct09Документ132 страницыLive IT Oct09indianebooksОценок пока нет

- Industrial Automation Lab: Project ProposalДокумент3 страницыIndustrial Automation Lab: Project ProposalAmaan MajidОценок пока нет

- Quiz ErrorsДокумент5 страницQuiz Errorsanon_843459121Оценок пока нет

- Bilingual First Language Acquisition: January 2008Документ11 страницBilingual First Language Acquisition: January 2008Katsiaryna HurbikОценок пока нет

- A Review of The Book That Made Your World. by Vishal MangalwadiДокумент6 страницA Review of The Book That Made Your World. by Vishal Mangalwadigaylerob100% (1)

- A044 2019 20 Readiness Review Template For EAC 3-12-2018 FinalДокумент25 страницA044 2019 20 Readiness Review Template For EAC 3-12-2018 FinalMohamed AbdelSalamОценок пока нет

- RET541 543ParlistENaДокумент145 страницRET541 543ParlistENaMatthew Mason100% (1)

- Diagnosis Dan Tatalaksana Pasien Dengan Insufisiensi Akomodasi - Sri Hudaya WidihasthaДокумент13 страницDiagnosis Dan Tatalaksana Pasien Dengan Insufisiensi Akomodasi - Sri Hudaya WidihasthamalaОценок пока нет

- Revenge, Hypnotism, and Oedipus in OldboyДокумент13 страницRevenge, Hypnotism, and Oedipus in OldboyAdrián PiqueroОценок пока нет

- Spacex PDFДокумент69 страницSpacex PDFEmerovsky ReyesОценок пока нет

- Return To Sport After Surgical Management of Posterior Shoulder InstabilityДокумент13 страницReturn To Sport After Surgical Management of Posterior Shoulder InstabilityAziz CupinОценок пока нет

- BCM Notes Unit No. IIДокумент14 страницBCM Notes Unit No. IIMahesh RamtekeОценок пока нет

- Dan Millman: The Hidden SchoolДокумент1 страницаDan Millman: The Hidden SchoolWPW50% (2)

- IO: Barriers To Entry and Exit in MarketsДокумент4 страницыIO: Barriers To Entry and Exit in MarketsSamuel Liël OdiaОценок пока нет

- Indra: Detail Pre-Commissioning Procedure For Service Test of Service Water For Unit 040/041/042/043Документ28 страницIndra: Detail Pre-Commissioning Procedure For Service Test of Service Water For Unit 040/041/042/043AnhTuấnPhanОценок пока нет

- Nakul VermaДокумент112 страницNakul VermaNakul VermaОценок пока нет

- Surveying Lesson 6 To 10 PDFДокумент68 страницSurveying Lesson 6 To 10 PDFNadane AldoverОценок пока нет

- Capitec Case StudyДокумент6 страницCapitec Case StudyMpho SeutloaliОценок пока нет

- Cultural Appropriation in The Fashion IndustryДокумент2 страницыCultural Appropriation in The Fashion IndustrykristiancobaesОценок пока нет

- Megawatt Station Inverter PVS800 1 To 1.25MW-ABBДокумент4 страницыMegawatt Station Inverter PVS800 1 To 1.25MW-ABBkimscribd66Оценок пока нет