Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Pi 2015 WWW - Questionpaperz.inДокумент22 страницыPi 2015 WWW - Questionpaperz.inATUL CHAUHANОценок пока нет

- GATE 2015 Question Papers With Answers For ME - Mechanical Engineering PDFДокумент23 страницыGATE 2015 Question Papers With Answers For ME - Mechanical Engineering PDFATUL CHAUHANОценок пока нет

- Basic ThermoДокумент12 страницBasic ThermoATUL CHAUHANОценок пока нет

- Top Museums in India: A State-by-State GuideДокумент12 страницTop Museums in India: A State-by-State GuideATUL CHAUHANОценок пока нет

- GATE 2015 Question Papers With Answers For MA - MathematicsДокумент19 страницGATE 2015 Question Papers With Answers For MA - MathematicsATUL CHAUHANОценок пока нет

- Highest Mountain Peaks StatewiseДокумент3 страницыHighest Mountain Peaks StatewiseATUL CHAUHANОценок пока нет

- Second Law of ThermodynamicsДокумент40 страницSecond Law of ThermodynamicscaptainhassОценок пока нет

- GATE 2015 Question Papers With Answers For ME - Mechanical Engineering PDFДокумент23 страницыGATE 2015 Question Papers With Answers For ME - Mechanical Engineering PDFATUL CHAUHANОценок пока нет

- GATE 2015 Question Papers With Answers For in - Instrumentation EngineeringДокумент26 страницGATE 2015 Question Papers With Answers For in - Instrumentation EngineeringATUL CHAUHANОценок пока нет

- Module 8Документ12 страницModule 8Vallapureddy VenkateshОценок пока нет

- Clausius InequalityДокумент53 страницыClausius InequalityNandhanОценок пока нет

- Pure SubstancesДокумент42 страницыPure SubstancesATUL CHAUHANОценок пока нет

- List of PhobiasДокумент8 страницList of PhobiasATUL CHAUHANОценок пока нет

- Important Insurance Abbreviations Cheat SheetДокумент36 страницImportant Insurance Abbreviations Cheat SheetATUL CHAUHANОценок пока нет

- FC Basics Technology TypesДокумент2 страницыFC Basics Technology TypesATUL CHAUHANОценок пока нет

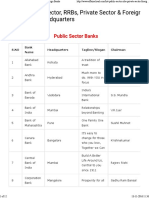

- Banks at GalanceДокумент12 страницBanks at GalanceATUL CHAUHANОценок пока нет

- Discretization of Convection-Diffusion Equation - Afinite Volume Approach - 5Документ19 страницDiscretization of Convection-Diffusion Equation - Afinite Volume Approach - 5ATUL CHAUHANОценок пока нет

- Important Gardens in IndiaДокумент3 страницыImportant Gardens in IndiaATUL CHAUHANОценок пока нет

- Conservation Equation PDFДокумент32 страницыConservation Equation PDFATUL CHAUHANОценок пока нет

- MMEMD 103 CAD in ManufacturingДокумент3 страницыMMEMD 103 CAD in ManufacturingRaghuОценок пока нет

- L-04 BSplines NURBS.6Документ10 страницL-04 BSplines NURBS.6ATUL CHAUHANОценок пока нет

- Geometric Modelling2Документ287 страницGeometric Modelling2ATUL CHAUHANОценок пока нет

- CFD Lecture1Документ25 страницCFD Lecture1GCVishnuKumar100% (1)

- 8a CurvesДокумент67 страниц8a CurvesMady MathurОценок пока нет

- Cubic SplineДокумент29 страницCubic SplineATUL CHAUHANОценок пока нет

- Cubic Hermite Spline Interpolation IIДокумент6 страницCubic Hermite Spline Interpolation IIATUL CHAUHANОценок пока нет

- Chapter 3 InterpolationДокумент35 страницChapter 3 InterpolationATUL CHAUHAN100% (1)

- CurvesДокумент4 страницыCurvesKannan SreenivasanОценок пока нет

- Cubic Hermite Spline Interpolation IIДокумент6 страницCubic Hermite Spline Interpolation IIATUL CHAUHANОценок пока нет

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Time Dependent SEДокумент14 страницTime Dependent SEabdullhОценок пока нет

- Lecture Notes On Classical Mechanics (PDFDrive)Документ463 страницыLecture Notes On Classical Mechanics (PDFDrive)William CruzОценок пока нет

- Summative Test No. 2 Grade 8Документ3 страницыSummative Test No. 2 Grade 8LENETTE ALAGON100% (1)

- Mobile Robot KinematicsДокумент22 страницыMobile Robot Kinematicsdtungtnt167Оценок пока нет

- Magnetic Field Splitting of Spectral LinesДокумент2 страницыMagnetic Field Splitting of Spectral LinesSio MoОценок пока нет

- Pre-Calculus Cartesian Coordinate System GuideДокумент13 страницPre-Calculus Cartesian Coordinate System GuideMaui FloresОценок пока нет

- NPTEL Web Course On Complex Analysis: A. SwaminathanДокумент16 страницNPTEL Web Course On Complex Analysis: A. SwaminathanAditya KoutharapuОценок пока нет

- CENTER OF MASS MOTION AND MOMENTUMДокумент11 страницCENTER OF MASS MOTION AND MOMENTUMsolomon mwatiОценок пока нет

- Hydrostatic Force On Plane SurfacesДокумент3 страницыHydrostatic Force On Plane SurfaceskarthikОценок пока нет

- Sample Paper-1maths-XiiДокумент3 страницыSample Paper-1maths-XiiPubg BoyОценок пока нет

- CH 30 Quantum PhysicsДокумент1 страницаCH 30 Quantum PhysicsHassan Ali BhuttaОценок пока нет

- (2020) - M. Nadkarni. Spectral Theory of Dynamical SystemsДокумент223 страницы(2020) - M. Nadkarni. Spectral Theory of Dynamical SystemsJORGE LUIS JUNIOR JIMENEZ GOMEZОценок пока нет

- Summary of Vector Calculus PDFДокумент2 страницыSummary of Vector Calculus PDFRanu GamesОценок пока нет

- Modified WKB Approximation For Fowler-Nordheim Tunneling Phenomenon in Nano-Structure Based SemiconductorsДокумент18 страницModified WKB Approximation For Fowler-Nordheim Tunneling Phenomenon in Nano-Structure Based Semiconductorsmaheshwarivikas1982Оценок пока нет

- Easiest definition of entropy in one sentenceДокумент19 страницEasiest definition of entropy in one sentenceMark J. Burton IIОценок пока нет

- ATOMIC STRUCTURE: SUBATOMIC PARTICLES, NUCLEUS, PROTONS, NEUTRONS, ELECTRONSДокумент34 страницыATOMIC STRUCTURE: SUBATOMIC PARTICLES, NUCLEUS, PROTONS, NEUTRONS, ELECTRONSYieksh BernaldeОценок пока нет

- Plastic Analysis of Slabs Using Yield-Line and Strip MethodsДокумент11 страницPlastic Analysis of Slabs Using Yield-Line and Strip MethodsDobromir DinevОценок пока нет

- INDEX - The Feynman Lectures On PhysicsДокумент5 страницINDEX - The Feynman Lectures On PhysicsJuanLoredoОценок пока нет

- Xy 2 Xyz XTT 2x+3tДокумент2 страницыXy 2 Xyz XTT 2x+3tSketchily SebenteОценок пока нет

- Tensor Algebra v02Документ45 страницTensor Algebra v02Sharjeel Ahmed ShakeelОценок пока нет

- Gravitational Flux and Space Curvatures Under Gravitational ForcesДокумент4 страницыGravitational Flux and Space Curvatures Under Gravitational ForcespaharalalageОценок пока нет

- Parton Brian Lesson WorksheetsДокумент9 страницParton Brian Lesson Worksheetsapi-353457841Оценок пока нет

- Fys2140 Oblig 02Документ4 страницыFys2140 Oblig 02은지Оценок пока нет

- Chemistry (Atom and Subatomic Particles)Документ7 страницChemistry (Atom and Subatomic Particles)Meo Angelo AlcantaraОценок пока нет

- Development of The Atomic TheoryДокумент2 страницыDevelopment of The Atomic TheoryJimmy gogoОценок пока нет

- Symmetry Operations and Point GroupДокумент13 страницSymmetry Operations and Point GroupRahul AroraОценок пока нет

- Linear Algebra and its Applications: Functions of a matrix and Krylov matrices聻Документ16 страницLinear Algebra and its Applications: Functions of a matrix and Krylov matrices聻krrrОценок пока нет

- Answer KeyДокумент4 страницыAnswer KeyNajwa KayyaliОценок пока нет

- Goldstein CoverДокумент1 страницаGoldstein CoverJuan Sebastian RamirezОценок пока нет

- ME Chapter 2Документ1 страницаME Chapter 2allovid50% (2)