Вам также может понравиться

- IncomeTax Banggawan2019 Ch14Документ12 страницIncomeTax Banggawan2019 Ch14Noreen Ledda0% (1)

- Pay Stub Portal3Документ1 страницаPay Stub Portal3cwhite2150Оценок пока нет

- FORM 102 Petition For Insolvency - Petitioner Corporation Has No More Assets or Property To Pay His Obligations and Had Already Closed Operations.Документ3 страницыFORM 102 Petition For Insolvency - Petitioner Corporation Has No More Assets or Property To Pay His Obligations and Had Already Closed Operations.Alexandrius Van VailocesОценок пока нет

- Solved DM Inc Incurred A 25 000 Net Capital Loss in 2014Документ1 страницаSolved DM Inc Incurred A 25 000 Net Capital Loss in 2014Anbu jaromiaОценок пока нет

- CIR Vs Far East BankДокумент1 страницаCIR Vs Far East BankRodney SantiagoОценок пока нет

- Abscbn Vs CtaДокумент8 страницAbscbn Vs CtaWinnie Ann Daquil Lomosad-MisagalОценок пока нет

- RCBC vs. CIR (GR No. 170257, September 7, 2011)Документ2 страницыRCBC vs. CIR (GR No. 170257, September 7, 2011)Arnold JoseОценок пока нет

- ToledoДокумент1 страницаToledotantum ergumОценок пока нет

- Yabes V FlojoДокумент5 страницYabes V FlojoanailabucaОценок пока нет

- Tax Cases Week 2Документ76 страницTax Cases Week 2Wilfredo Guerrero IIIОценок пока нет

- DigestДокумент8 страницDigestDewm DewmОценок пока нет

- Lectures Atty. Lu Rem 2Документ5 страницLectures Atty. Lu Rem 2JD BallosОценок пока нет

- Corpo 13Документ3 страницыCorpo 13Gabe BedanaОценок пока нет

- CC 64227 - P vs. VIRINA DecisionДокумент8 страницCC 64227 - P vs. VIRINA DecisionPrincess Janine SyОценок пока нет

- Simple AcknowledgementДокумент2 страницыSimple AcknowledgementDarwin BradecinaОценок пока нет

- Philippine Amusement and Gaming Corporation vs. Bureau of Internal Revenue, 782 SCRA 402, January 27, 2016Документ16 страницPhilippine Amusement and Gaming Corporation vs. Bureau of Internal Revenue, 782 SCRA 402, January 27, 2016j0d3Оценок пока нет

- 3.G.R. No. 103092Документ5 страниц3.G.R. No. 103092Lord AumarОценок пока нет

- fflmtiln: Upreme LourtДокумент11 страницfflmtiln: Upreme LourtJesryl 8point8 TeamОценок пока нет

- Mendez V People and CTA 726 SCRA 203 2014Документ13 страницMendez V People and CTA 726 SCRA 203 2014Darrel John Sombilon100% (1)

- 35 Philippine Dream Company Inc. V.20210424-12-1jxqs4iДокумент11 страниц35 Philippine Dream Company Inc. V.20210424-12-1jxqs4iervingabralagbonОценок пока нет

- Tax 1 Cases For Study - Full Tex CasesdocxДокумент209 страницTax 1 Cases For Study - Full Tex CasesdocxwallyОценок пока нет

- Lucas Adamson VsДокумент2 страницыLucas Adamson VsJeff SantosОценок пока нет

- Torres and de Jesus vs. Sicat Vda. de MoralesДокумент6 страницTorres and de Jesus vs. Sicat Vda. de MoralesRoizki Edward MarquezОценок пока нет

- CIR v. Javier Jr. GR No. 78953 31 July 1991 199 SCRA 825Документ2 страницыCIR v. Javier Jr. GR No. 78953 31 July 1991 199 SCRA 825bestie bushОценок пока нет

- Taxation Law LimvsCAДокумент3 страницыTaxation Law LimvsCAJohn Benedict TigsonОценок пока нет

- 2 CIR vs. Sony Phils, Inc. G.R. No. 178697, November 17, 2010Документ17 страниц2 CIR vs. Sony Phils, Inc. G.R. No. 178697, November 17, 2010Alfred GarciaОценок пока нет

- TaxationBarQ26A TaxRemediesДокумент32 страницыTaxationBarQ26A TaxRemediesjuneson agustinОценок пока нет

- CIR vs. United Salvage and Towage, 2014 - CTA - Technical Rules of Evidence - PAN - FANДокумент16 страницCIR vs. United Salvage and Towage, 2014 - CTA - Technical Rules of Evidence - PAN - FANhenzencameroОценок пока нет

- Digest 2Документ27 страницDigest 2Vianice BaroroОценок пока нет

- Cir V Pascor Realty & Dev'T Corp Et. Al. GR No. 128315, June 29, 1999Документ8 страницCir V Pascor Realty & Dev'T Corp Et. Al. GR No. 128315, June 29, 1999Cristy Yaun-CabagnotОценок пока нет

- Legaspi V CAДокумент7 страницLegaspi V CAElizabeth LotillaОценок пока нет

- Regional Trial Court of Cebu BranchДокумент3 страницыRegional Trial Court of Cebu BranchNika RojasОценок пока нет

- Petitioner RespondentsДокумент19 страницPetitioner RespondentsKriszan ManiponОценок пока нет

- Ungab vs. CusiДокумент10 страницUngab vs. CusiKitkat AyalaОценок пока нет

- Tax2 DigestsДокумент11 страницTax2 DigestsErwin Roxas100% (1)

- Great Pacific V CA GДокумент9 страницGreat Pacific V CA GYvon BaguioОценок пока нет

- Cir Vs Metro Super Rama DigestДокумент2 страницыCir Vs Metro Super Rama DigestKobe BryantОценок пока нет

- CIR v. Next Mobile IncДокумент11 страницCIR v. Next Mobile IncPaulineОценок пока нет

- Republic Vs AcebedoДокумент2 страницыRepublic Vs AcebedoMaria Raisa Helga YsaacОценок пока нет

- CIR vs. American Express InternationalДокумент30 страницCIR vs. American Express InternationalMonikkaОценок пока нет

- Churchill and Tait vs. ConcepcionДокумент5 страницChurchill and Tait vs. ConcepcionGee GuevarraОценок пока нет

- Director of Lands v. IAC, 219 SCRA 339Документ4 страницыDirector of Lands v. IAC, 219 SCRA 339FranzMordenoОценок пока нет

- 304-CIR v. Fitness by Design, Inc. G.R. No. 215957 November 9, 2016Документ9 страниц304-CIR v. Fitness by Design, Inc. G.R. No. 215957 November 9, 2016Jopan SJ100% (1)

- Sample Judicial AffidavitДокумент3 страницыSample Judicial AffidavitRoland Bon IntudОценок пока нет

- Cir Vs CA, Cta, GCL Retirement PlanДокумент6 страницCir Vs CA, Cta, GCL Retirement PlanLord AumarОценок пока нет

- Kapatiran Vs TanДокумент3 страницыKapatiran Vs TanPoks Bongat AlejoОценок пока нет

- Frank Uy V BIR Case DigestДокумент2 страницыFrank Uy V BIR Case DigestdОценок пока нет

- Commissioner of Internal Revenue Fireman'S Fund Insurance Company and The Court ofДокумент2 страницыCommissioner of Internal Revenue Fireman'S Fund Insurance Company and The Court ofjulyenfortunatoОценок пока нет

- 001 - Mendoza v. TehДокумент3 страницы001 - Mendoza v. TehMiko Maniwa100% (1)

- CIR v. Asalus CorpДокумент9 страницCIR v. Asalus CorpMeg ReyesОценок пока нет

- 9 - Getz Pharma (Phils.), Inc. v. CIRДокумент13 страниц9 - Getz Pharma (Phils.), Inc. v. CIRCarlota Villaroman100% (1)

- Nego DigestsДокумент22 страницыNego DigestsRachel Anne Diao Lagnason100% (1)

- People Vs MagdadaroДокумент2 страницыPeople Vs MagdadaroBirthday NanamanОценок пока нет

- Tax Review Case DigestsДокумент10 страницTax Review Case DigestsTina MarianoОценок пока нет

- G.R. No. L-15978 December 29, 1960: Davao Gulf Lumber Corporation vs. Hon. N. Baens Del RosarioДокумент3 страницыG.R. No. L-15978 December 29, 1960: Davao Gulf Lumber Corporation vs. Hon. N. Baens Del RosarioFzlBuctuanОценок пока нет

- Consent For Publication FormДокумент1 страницаConsent For Publication FormKentKawashimaОценок пока нет

- Nuez v. Cruz-ApaoДокумент2 страницыNuez v. Cruz-Apaodaboy15Оценок пока нет

- GR 120935 - Adamson Vs CIRДокумент11 страницGR 120935 - Adamson Vs CIRJane MarianОценок пока нет

- CIR v. Aichi Forging Company of Asia, IncДокумент22 страницыCIR v. Aichi Forging Company of Asia, IncAronJamesОценок пока нет

- 3 CIR V SEAGATEДокумент15 страниц3 CIR V SEAGATEjahzelcarpioОценок пока нет

- Sun Life V BacaniДокумент2 страницыSun Life V BacaniSimon James SemillaОценок пока нет

- CIR vs. PL Management Intl Phils. Inc. GR No. 160949Документ4 страницыCIR vs. PL Management Intl Phils. Inc. GR No. 160949ZeusKimОценок пока нет

- Cir Vs Bpi July 2009Документ9 страницCir Vs Bpi July 2009leo.rosarioОценок пока нет

- 19 Commission On Elections Vs ConradocruzДокумент1 страница19 Commission On Elections Vs Conradocruzian ballartaОценок пока нет

- 13Документ3 страницы13ian ballartaОценок пока нет

- Cir Vs Algue, Inc. GR No. L-28896 February 7, 1996Документ2 страницыCir Vs Algue, Inc. GR No. L-28896 February 7, 1996ian ballartaОценок пока нет

- CIR, vs. THE ESTATE OF BENIGNO P. TODA, JR., G.R. No. 147188. September 14, 2004 FactsДокумент1 страницаCIR, vs. THE ESTATE OF BENIGNO P. TODA, JR., G.R. No. 147188. September 14, 2004 Factsian ballartaОценок пока нет

- 76 People Vs Ordoo - DigestedДокумент1 страница76 People Vs Ordoo - Digestedian ballartaОценок пока нет

- 99 PP Vs MalimitДокумент1 страница99 PP Vs Malimitian ballartaОценок пока нет

- 75 People Vs Galit - DigestedДокумент1 страница75 People Vs Galit - Digestedian ballartaОценок пока нет

- 79 People Vs Baloloy - DigestedДокумент1 страница79 People Vs Baloloy - Digestedian ballartaОценок пока нет

- SM Vs City of ManilaДокумент2 страницыSM Vs City of Manilaian ballartaОценок пока нет

- Tax Prelim Exam ReviewerДокумент20 страницTax Prelim Exam ReviewerWawi Dela RosaОценок пока нет

- A-Radha@dxc - Com F16Документ9 страницA-Radha@dxc - Com F16Radha PraveenОценок пока нет

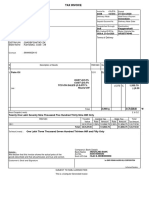

- Tax ReceiptДокумент1 страницаTax ReceiptKen NjorogeОценок пока нет

- Payslip Month of December 2022Документ1 страницаPayslip Month of December 2022Amir SohailОценок пока нет

- Test Bank For Corporations Partnerships Estates and Trusts 2020 43th by RaabeДокумент77 страницTest Bank For Corporations Partnerships Estates and Trusts 2020 43th by RaabeJessica RiffleОценок пока нет

- Accounting VoucherДокумент1 страницаAccounting Voucheradposting wОценок пока нет

- 33AHRPM6127G1Z7: Tax InvoiceДокумент1 страница33AHRPM6127G1Z7: Tax InvoiceMani DeebanОценок пока нет

- Filipinas Synthetic Fiber Corporation V CAДокумент2 страницыFilipinas Synthetic Fiber Corporation V CACedrick TanОценок пока нет

- House Majority Forward's 2020 Form 990Документ49 страницHouse Majority Forward's 2020 Form 990JoeSchoffstallОценок пока нет

- Potvrda o Oporezivi Dohodak Obrazac CPT 106 - Bos I EngДокумент2 страницыPotvrda o Oporezivi Dohodak Obrazac CPT 106 - Bos I EngEldin RatkovicОценок пока нет

- Schedule 1 For 2019 Form 1040Документ1 страницаSchedule 1 For 2019 Form 1040CNBC.comОценок пока нет

- Income Taxation Unit 2 - PreludeДокумент8 страницIncome Taxation Unit 2 - PreludeEllieОценок пока нет

- Bal Sheet (Gail)Документ4 страницыBal Sheet (Gail)SuhailОценок пока нет

- Metro Inc v. CIRДокумент2 страницыMetro Inc v. CIRJahn Avery Mitchel DatukonОценок пока нет

- Bitumen Prices Wef 16 01 12Документ2 страницыBitumen Prices Wef 16 01 12Mahadeva PrasadОценок пока нет

- Ccu To DelДокумент1 страницаCcu To DelP K PANDAОценок пока нет

- RR-14 01Документ9 страницRR-14 01Vel June De LeonОценок пока нет

- AO Code Search For PANДокумент13 страницAO Code Search For PANSubhashis DasОценок пока нет

- GST Question PaperДокумент6 страницGST Question Paperramaswamy dОценок пока нет

- Estate Under Administration-Tax2Документ15 страницEstate Under Administration-Tax2onet88Оценок пока нет

- Krishiv Infotech: Tax InvoiceДокумент3 страницыKrishiv Infotech: Tax InvoiceRiviera SarkhejОценок пока нет

- Form 16 - TCS Part BДокумент4 страницыForm 16 - TCS Part BSai SekharОценок пока нет

- UmMwWHVzMFEwc3paWkRSWkVjS0o3Zz09 InvoiceДокумент2 страницыUmMwWHVzMFEwc3paWkRSWkVjS0o3Zz09 InvoiceNSTI AKKIОценок пока нет

- CIR vs. de La Salle University, Inc., 808 SCRA 156 (2016)Документ2 страницыCIR vs. de La Salle University, Inc., 808 SCRA 156 (2016)Anonymous MikI28PkJc100% (2)

- 1 - Shrout Indictment December 15, 2015Документ5 страниц1 - Shrout Indictment December 15, 2015Freeman LawyerОценок пока нет

- Conscient Heritage Max DealДокумент2 страницыConscient Heritage Max Dealvikas2354_268878339Оценок пока нет

- Circular 26 2019Документ4 страницыCircular 26 2019SnehОценок пока нет