Вам также может понравиться

- YüklemeДокумент58 страницYüklemeCenk KurterОценок пока нет

- Savings MaximiserДокумент2 страницыSavings MaximiserselenalaniОценок пока нет

- Bank Reconciliation Statement: Strictly ConfidentialДокумент3 страницыBank Reconciliation Statement: Strictly Confidentialnegussie biruОценок пока нет

- NOVEMBER 2010 Deutsche Bank Americas Company Research List - EXTERNALДокумент2 страницыNOVEMBER 2010 Deutsche Bank Americas Company Research List - EXTERNALkabothutweОценок пока нет

- Crescent Point Energy BMO 9.8.13Документ14 страницCrescent Point Energy BMO 9.8.13JorgeОценок пока нет

- Statement of Account 157008615988:: 31-May-2021: 01-May-2021 To 31-May-2021Документ3 страницыStatement of Account 157008615988:: 31-May-2021: 01-May-2021 To 31-May-2021Suvam MohapatraОценок пока нет

- Seven Generations Energy LTD.: Canada ResearchДокумент27 страницSeven Generations Energy LTD.: Canada ResearchAnonymous m3c6M1Оценок пока нет

- Capital Investments On Corridor X1Документ708 страницCapital Investments On Corridor X1Web BirdyОценок пока нет

- Analisis Banco SantanderДокумент6 страницAnalisis Banco Santanderperro_mx0% (1)

- Transaction Details - PayPalДокумент1 страницаTransaction Details - PayPalHamenodОценок пока нет

- CG Egypt SME 569900 - AS Implementation PlanДокумент18 страницCG Egypt SME 569900 - AS Implementation PlanMohamed Ali AtigОценок пока нет

- Fastag E-Statement: Customer Details Bank DetailsДокумент2 страницыFastag E-Statement: Customer Details Bank DetailsKunjemy EmyОценок пока нет

- Bank of Kigali Announces Q1 2010 ResultsДокумент7 страницBank of Kigali Announces Q1 2010 ResultsBank of KigaliОценок пока нет

- ADIBДокумент5 страницADIBMohamed BathaqiliОценок пока нет

- Orange - Equity Research ReportДокумент6 страницOrange - Equity Research Reportosama aboualamОценок пока нет

- 1.accounts 2012 AcnabinДокумент66 страниц1.accounts 2012 AcnabinArman Hossain WarsiОценок пока нет

- CSR Kuwait Retail Industry July2010Документ15 страницCSR Kuwait Retail Industry July2010Daty HassanОценок пока нет

- UBS Subordinated Bank Bonds 20100916Документ17 страницUBS Subordinated Bank Bonds 20100916dtm541Оценок пока нет

- Goldman 07 Internet RoadmapДокумент95 страницGoldman 07 Internet Roadmapapi-3747284Оценок пока нет

- V Office 2019Документ1 страницаV Office 2019zulhirsan laluОценок пока нет

- Bank Reconciliation Statement 0007Документ16 страницBank Reconciliation Statement 0007Hussein Abdou HassanОценок пока нет

- Passbookstmt 1610356751839Документ4 страницыPassbookstmt 1610356751839Vicky KumarОценок пока нет

- Account StatementДокумент12 страницAccount StatementLoan LoanОценок пока нет

- The "Best" Investor Pitch Deck Outline: (Your Logo Here)Документ28 страницThe "Best" Investor Pitch Deck Outline: (Your Logo Here)Abhijit PathakОценок пока нет

- Interview Notes For The Tax Review of New Audit Clients (CPTX) 2022.03.17Документ19 страницInterview Notes For The Tax Review of New Audit Clients (CPTX) 2022.03.17AdamОценок пока нет

- Anna Brockle-2 PDFДокумент1 страницаAnna Brockle-2 PDFNoticias FarándulasОценок пока нет

- Uvw DIUdox NJ1 Cs MДокумент8 страницUvw DIUdox NJ1 Cs Msiva kodaliОценок пока нет

- Concentrix Form 16Документ9 страницConcentrix Form 16Neeraj M.RОценок пока нет

- Your Statement: Smart AccessДокумент3 страницыYour Statement: Smart AccesscynthiaОценок пока нет

- 01-Apr-2020Документ1 страница01-Apr-2020mubeen khanОценок пока нет

- SABB Platinum Visa Credit Card StatementДокумент2 страницыSABB Platinum Visa Credit Card StatementMujahed AhmedОценок пока нет

- ZTBL 2008Документ62 страницыZTBL 2008Mahmood KhanОценок пока нет

- Payment Slip: Summary of Charges / Payments Current Bill AnalysisДокумент4 страницыPayment Slip: Summary of Charges / Payments Current Bill AnalysisMohd Salleh AmboОценок пока нет

- AprilДокумент3 страницыAprilLathaRajRajandrenОценок пока нет

- Application Form Account Opening20112016031008Документ4 страницыApplication Form Account Opening20112016031008Jim AlanОценок пока нет

- View / Print Statement: Select Your Account / Credit Card Statement View SettingsДокумент2 страницыView / Print Statement: Select Your Account / Credit Card Statement View Settingskhadeerabk7925Оценок пока нет

- CardStatement 2016-11-19Документ6 страницCardStatement 2016-11-19manjuОценок пока нет

- Solution 1: Calculation of Total Assessable Income, Taxable Income, Tax LiabilityДокумент14 страницSolution 1: Calculation of Total Assessable Income, Taxable Income, Tax LiabilityDevender SharmaОценок пока нет

- Icici Bank Gstinvoice May 2021 Xxxxxxxx2165Документ1 страницаIcici Bank Gstinvoice May 2021 Xxxxxxxx2165Solomon PasulaОценок пока нет

- Dubai Islamic Bank P.J.S.C. (DIB) - Financial and Strategic SWOT Analysis ReviewДокумент32 страницыDubai Islamic Bank P.J.S.C. (DIB) - Financial and Strategic SWOT Analysis ReviewChiranjiv Jain75% (4)

- QatarДокумент2 страницыQatarKelz YouknowmynameОценок пока нет

- T1 General PDFДокумент4 страницыT1 General PDFbatmanbittuОценок пока нет

- Balance Sheet: United Spirits Limited Annual ReportДокумент4 страницыBalance Sheet: United Spirits Limited Annual ReportUppiliappan GopalanОценок пока нет

- State Bank of IndiaДокумент1 страницаState Bank of IndiaBala SundarОценок пока нет

- Account No: Total Amount Due:: Important InformationДокумент2 страницыAccount No: Total Amount Due:: Important InformationWinnie LuongОценок пока нет

- Individual Account Opening Form: (Demat + Trading)Документ30 страницIndividual Account Opening Form: (Demat + Trading)ONE STEP for othersОценок пока нет

- Project DescriptionДокумент4 страницыProject DescriptionVenu GopalОценок пока нет

- 3556 - Etisalat - ID Exception-App Form - Eng Oct 2012Документ2 страницы3556 - Etisalat - ID Exception-App Form - Eng Oct 2012zahid_497Оценок пока нет

- Account Statement 220320 150321Документ170 страницAccount Statement 220320 150321Venkatesh DoodamОценок пока нет

- Notes SAR'000 (Unaudited) 14,482,456 6,998,836 34,094,654 115,286,635 399,756 411,761 1,749,778 3,671,357Документ10 страницNotes SAR'000 (Unaudited) 14,482,456 6,998,836 34,094,654 115,286,635 399,756 411,761 1,749,778 3,671,357Arafath CholasseryОценок пока нет

- Vanguard FTSE All-World UCITS ETF: (USD) Distributing - An Exchange-Traded FundДокумент4 страницыVanguard FTSE All-World UCITS ETF: (USD) Distributing - An Exchange-Traded FundFranco CalabiОценок пока нет

- Account Statement From 1 Dec 2020 To 20 Jan 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceДокумент4 страницыAccount Statement From 1 Dec 2020 To 20 Jan 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceNiranjanPandeyОценок пока нет

- Bank of Kigali 1H 2010 Results UpdateДокумент48 страницBank of Kigali 1H 2010 Results UpdateBank of KigaliОценок пока нет

- Dintle StatementДокумент3 страницыDintle StatementMANDLAОценок пока нет

- 335872Документ7 страниц335872pradhan13Оценок пока нет

- Statement NewДокумент2 страницыStatement NewabhiramОценок пока нет

- 1487857618519Hf5kgO9kysK6TDI2 PDFДокумент2 страницы1487857618519Hf5kgO9kysK6TDI2 PDFKARTHICKОценок пока нет

- InvoiceДокумент1 страницаInvoiceKroma ServicesОценок пока нет

- Bajaj Finance - Incred EquitiesДокумент42 страницыBajaj Finance - Incred Equitieskumar somyaОценок пока нет

- HDFC Bank: CMP: INR1,872 The JuggernautДокумент22 страницыHDFC Bank: CMP: INR1,872 The JuggernautSwapnil pawarОценок пока нет

- Aditya Birla Low Duration Fund - One PagerДокумент2 страницыAditya Birla Low Duration Fund - One PagerjoycoolОценок пока нет

- Fund Factsheet For AprilДокумент71 страницаFund Factsheet For ApriljoycoolОценок пока нет

- SBI Bluechip Fund - One PagerДокумент1 страницаSBI Bluechip Fund - One PagerjoycoolОценок пока нет

- Axis Bluechip Fund - One PagerДокумент3 страницыAxis Bluechip Fund - One PagerjoycoolОценок пока нет

- ICICI Balanced Advantage Fund - One PagerДокумент2 страницыICICI Balanced Advantage Fund - One PagerjoycoolОценок пока нет

- Dixon 1QFY22 Result Update - OthersДокумент14 страницDixon 1QFY22 Result Update - OthersjoycoolОценок пока нет

- YBL Investor Presentation - June29Документ20 страницYBL Investor Presentation - June29joycoolОценок пока нет

- YBL Capital Raise - Release - 260320Документ2 страницыYBL Capital Raise - Release - 260320joycoolОценок пока нет

- Allcargo Global Logistics LTD.: CompanyДокумент5 страницAllcargo Global Logistics LTD.: CompanyjoycoolОценок пока нет

- Nomura - Jun 23 - Minda IndustriesДокумент7 страницNomura - Jun 23 - Minda IndustriesjoycoolОценок пока нет

- Solar Industries (SOLEXP) : Detonating To Explosive GrowthДокумент32 страницыSolar Industries (SOLEXP) : Detonating To Explosive GrowthjoycoolОценок пока нет

- Dr. Ashok Jhunjhunwala IIT MadrasДокумент10 страницDr. Ashok Jhunjhunwala IIT Madrasjoycool100% (1)

- Clariant Chemicals PDFДокумент13 страницClariant Chemicals PDFjoycoolОценок пока нет

- My Internship Report at EFUДокумент212 страницMy Internship Report at EFUAyesha Yasin85% (13)

- Listing Guide in TadaWulДокумент39 страницListing Guide in TadaWulJafferОценок пока нет

- Technical Analysis PDFДокумент37 страницTechnical Analysis PDFPriyanashi JainОценок пока нет

- ROA and ROEДокумент20 страницROA and ROEPassmore DubeОценок пока нет

- Sri Lanka PresentationДокумент26 страницSri Lanka PresentationADB_SAEN_ProjectsОценок пока нет

- Project in Birla Sun LifeДокумент27 страницProject in Birla Sun LifeRenny M PОценок пока нет

- Debtors Turnover RatioДокумент7 страницDebtors Turnover RatiorachitdedhiaОценок пока нет

- Bharat ReportДокумент99 страницBharat Reportjagrutisolanki01Оценок пока нет

- Chapter 9 Answer SheetДокумент10 страницChapter 9 Answer SheetJoan Gayle BalisiОценок пока нет

- Role of Fdi in Banking Sector Towards Stimulating Green BankingДокумент12 страницRole of Fdi in Banking Sector Towards Stimulating Green Bankingapi-33150260Оценок пока нет

- FINДокумент16 страницFINAnbang Xiao50% (2)

- INSURANCE-beda Reviewer PDFДокумент24 страницыINSURANCE-beda Reviewer PDFYen JonsonОценок пока нет

- Lotto NZ Winner's BookДокумент64 страницыLotto NZ Winner's BookStuff NewsroomОценок пока нет

- Capital Investment Decisions Answers To End of Chapter ExercisesДокумент3 страницыCapital Investment Decisions Answers To End of Chapter ExercisesJay BrockОценок пока нет

- Taj Textile Mills Limited: Quarterly Accounts September 30, 2006 (Un-Audited)Документ8 страницTaj Textile Mills Limited: Quarterly Accounts September 30, 2006 (Un-Audited)Muhammad Karim KhanОценок пока нет

- Macroeconomics Debate Final - Keynes Fiscal Stimulus PresentationДокумент24 страницыMacroeconomics Debate Final - Keynes Fiscal Stimulus Presentationapi-438130972Оценок пока нет

- Retail Banking An Introduction Research Methodology: Title of Project Statement of The Problem Objective of The StudyДокумент9 страницRetail Banking An Introduction Research Methodology: Title of Project Statement of The Problem Objective of The StudySandeep KumarОценок пока нет

- Unit I - Working Capital PolicyДокумент16 страницUnit I - Working Capital Policyjaskahlon92Оценок пока нет

- The Goals and Functions of Financial ManagementДокумент55 страницThe Goals and Functions of Financial ManagementwerlamodeОценок пока нет

- Benihana Cost F08 25-Jun-2008Документ19 страницBenihana Cost F08 25-Jun-2008Sheeba Naz100% (1)

- Final PPT of ProjectДокумент26 страницFinal PPT of ProjectPranav JhinaОценок пока нет

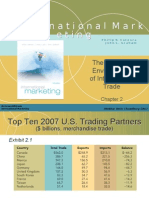

- International Marketing Chapter 2 (The Dynamic Environment of International Trade)Документ39 страницInternational Marketing Chapter 2 (The Dynamic Environment of International Trade)Nitin Jain0% (1)

- Strategic AlliancesДокумент22 страницыStrategic AlliancesAngel Anita100% (2)

- 40 SitaraДокумент2 страницы40 SitaraTIN_CUP_87100% (1)

- Complete The Following Balance Sheet Using This InformationДокумент4 страницыComplete The Following Balance Sheet Using This InformationSaleem Jaffer50% (2)

- BEC Vantage Practice TestsДокумент35 страницBEC Vantage Practice TestsNadieОценок пока нет

- Borrowing Costs CVДокумент34 страницыBorrowing Costs CVRigine Pobe Morgadez100% (1)

- PIALEFДокумент1 страницаPIALEFEileen LauОценок пока нет

- Turn Your Trading Easy With Automated TR PDFДокумент1 страницаTurn Your Trading Easy With Automated TR PDFtico ortiz aguilarОценок пока нет

- Preliminary Topic Five - Financial MarketsДокумент12 страницPreliminary Topic Five - Financial MarketsBaro LeeОценок пока нет

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!От EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Рейтинг: 4.5 из 5 звезд4.5/5 (14)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindОт EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindРейтинг: 5 из 5 звезд5/5 (231)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)От EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Рейтинг: 4.5 из 5 звезд4.5/5 (13)

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineОт EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineОценок пока нет

- Getting to Yes: How to Negotiate Agreement Without Giving InОт EverandGetting to Yes: How to Negotiate Agreement Without Giving InРейтинг: 4 из 5 звезд4/5 (652)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesОт EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesОценок пока нет

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)От EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Рейтинг: 4 из 5 звезд4/5 (33)

- The One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyОт EverandThe One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyРейтинг: 4.5 из 5 звезд4.5/5 (37)

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsОт EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsОценок пока нет

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsОт EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsРейтинг: 5 из 5 звезд5/5 (1)

- The Credit Formula: The Guide To Building and Rebuilding Lendable CreditОт EverandThe Credit Formula: The Guide To Building and Rebuilding Lendable CreditРейтинг: 5 из 5 звезд5/5 (1)

- The E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItОт EverandThe E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItРейтинг: 5 из 5 звезд5/5 (13)

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)От EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Рейтинг: 4.5 из 5 звезд4.5/5 (5)

- Finance Basics (HBR 20-Minute Manager Series)От EverandFinance Basics (HBR 20-Minute Manager Series)Рейтинг: 4.5 из 5 звезд4.5/5 (32)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelОт Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelОценок пока нет

- How to Measure Anything: Finding the Value of "Intangibles" in BusinessОт EverandHow to Measure Anything: Finding the Value of "Intangibles" in BusinessРейтинг: 4.5 из 5 звезд4.5/5 (28)

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsОт EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsРейтинг: 4 из 5 звезд4/5 (7)

- Excel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetОт EverandExcel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetОценок пока нет

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyОт EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyРейтинг: 5 из 5 звезд5/5 (1)

- Start, Study and Pass The CPA Exam FAST - Proven 8 Step CPA Exam Study PlaybookОт EverandStart, Study and Pass The CPA Exam FAST - Proven 8 Step CPA Exam Study PlaybookРейтинг: 5 из 5 звезд5/5 (4)

- Accounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCОт EverandAccounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCРейтинг: 5 из 5 звезд5/5 (1)

- Your Amazing Itty Bitty(R) Personal Bookkeeping BookОт EverandYour Amazing Itty Bitty(R) Personal Bookkeeping BookОценок пока нет