Вам также может понравиться

- 2018 9 - Barclays CSNY634764 Finding - Alpha A4Документ24 страницы2018 9 - Barclays CSNY634764 Finding - Alpha A4elizabethrasskazovaОценок пока нет

- 2021 Subsector OutlooksДокумент24 страницы2021 Subsector OutlooksHungОценок пока нет

- ECON+2105+exam +3+study+guide Chapters+6-8 Exam+date+04152015Документ56 страницECON+2105+exam +3+study+guide Chapters+6-8 Exam+date+04152015Likhit NayakОценок пока нет

- Sample Feasibility StudyДокумент17 страницSample Feasibility Studyim_isolated100% (1)

- BNP FX WeeklyДокумент22 страницыBNP FX WeeklyPhillip HsiaОценок пока нет

- Fed To Eventually Remove The Punch Bowl: Global FX WeeklyДокумент28 страницFed To Eventually Remove The Punch Bowl: Global FX Weeklygerrich rusОценок пока нет

- Barclays The FX Volatility Risk Premium Identifying Drivers and Investigating ReДокумент20 страницBarclays The FX Volatility Risk Premium Identifying Drivers and Investigating ReNeil SchofieldОценок пока нет

- Rabobank Quant Models Research MethodologiesДокумент15 страницRabobank Quant Models Research MethodologiesCynthia SerraoОценок пока нет

- CS - FX Compass Looking For Cracks 20230131Документ10 страницCS - FX Compass Looking For Cracks 20230131G.Trading.FxОценок пока нет

- CACIB - FAST FX Model 20230206Документ7 страницCACIB - FAST FX Model 20230206G.Trading.FxОценок пока нет

- Fair Value Model - Hardcoded DateДокумент9 страницFair Value Model - Hardcoded DateforexОценок пока нет

- 03 01 10 EOTM AppendixДокумент3 страницы03 01 10 EOTM AppendixZerohedge100% (1)

- Gs WeeklykickstartДокумент28 страницGs WeeklykickstartArtur SilvaОценок пока нет

- Morning Pack: Regional EquitiesДокумент59 страницMorning Pack: Regional Equitiesmega_richОценок пока нет

- BofA - FX Quant Signals For The FOMC and ECB 20230130Документ9 страницBofA - FX Quant Signals For The FOMC and ECB 20230130G.Trading.FxОценок пока нет

- CS Sprout 2018Документ35 страницCS Sprout 2018Nicolas Arroyo ScalabroniОценок пока нет

- Money Market Black SwanДокумент29 страницMoney Market Black SwanZerohedgeОценок пока нет

- How To Succeed As A Sell Side Trader: Brent DonnellyДокумент9 страницHow To Succeed As A Sell Side Trader: Brent DonnellyAlvinОценок пока нет

- FE-Seminar 10 15 2012Документ38 страницFE-Seminar 10 15 2012yerytОценок пока нет

- State of Market Feb 2008Документ42 страницыState of Market Feb 2008azharaqОценок пока нет

- Barcap India - Capital - Goods 7 Dec 2011Документ159 страницBarcap India - Capital - Goods 7 Dec 2011Sunayan PalОценок пока нет

- Barclays Global FX Quarterly Fed On Hold Eyes On GrowthДокумент42 страницыBarclays Global FX Quarterly Fed On Hold Eyes On GrowthgneymanОценок пока нет

- JPM Midyear Emerging Mar 2018-06-08 2686356Документ79 страницJPM Midyear Emerging Mar 2018-06-08 2686356rumi mahmoodОценок пока нет

- ACB - JP MorganДокумент23 страницыACB - JP MorganNam Phuong DangОценок пока нет

- Week in Pictures 10 17 22 1666106256Документ13 страницWeek in Pictures 10 17 22 1666106256Barry HeОценок пока нет

- Asean Strategy - JPM PDFДокумент19 страницAsean Strategy - JPM PDFRizkyAufaSОценок пока нет

- Launch of Conviction ListДокумент11 страницLaunch of Conviction ListWilson WongОценок пока нет

- Manulife - Indonesia Macro Outlook q4 2021 PDFДокумент48 страницManulife - Indonesia Macro Outlook q4 2021 PDFUdan RMОценок пока нет

- Oil & Commodities Monthly - February 2011Документ13 страницOil & Commodities Monthly - February 2011ILoveDubsОценок пока нет

- FX Insights: Global Foreign Exchange ResearchДокумент9 страницFX Insights: Global Foreign Exchange ResearchMyDoc09Оценок пока нет

- GBP Rates Strategy 28 January 2020Документ4 страницыGBP Rates Strategy 28 January 2020Nikolaus HildebrandОценок пока нет

- ING - FX TalkingДокумент18 страницING - FX TalkingCiocoiu Vlad AndreiОценок пока нет

- Foreign Exchange OutlookДокумент17 страницForeign Exchange Outlookdey.parijat209Оценок пока нет

- Global - Macro - Weekly - 8 March 2019 PDFДокумент60 страницGlobal - Macro - Weekly - 8 March 2019 PDFchaotic_pandemoniumОценок пока нет

- Corr and RegressДокумент42 страницыCorr and Regresspasan lahiruОценок пока нет

- HSBC - Currency Outlook DecemberДокумент46 страницHSBC - Currency Outlook Decembermgroble3Оценок пока нет

- Week Summary: Macro StrategyДокумент10 страницWeek Summary: Macro StrategyNoel AndreottiОценок пока нет

- Treasury Outlook MarДокумент6 страницTreasury Outlook Marelise_stefanikОценок пока нет

- Latin America Instrument and Market Guide - HSBCДокумент55 страницLatin America Instrument and Market Guide - HSBCmt5902Оценок пока нет

- Goldman Funds SicavДокумент658 страницGoldman Funds SicavThanh NguyenОценок пока нет

- Nordea TaaДокумент25 страницNordea Taaintel74Оценок пока нет

- Sessions 2 and 3 - Equity Valuation - in Session - Section EДокумент88 страницSessions 2 and 3 - Equity Valuation - in Session - Section EAnurag JainОценок пока нет

- Credit Suisse Investment Outlook 2018Документ64 страницыCredit Suisse Investment Outlook 2018dpbasic100% (1)

- Global Data Watch: Bumpy, A Little Better, and A Lot Less RiskyДокумент49 страницGlobal Data Watch: Bumpy, A Little Better, and A Lot Less RiskyAli Motlagh KabirОценок пока нет

- Mutual Funds Sahi HaiДокумент24 страницыMutual Funds Sahi Haishiva1602Оценок пока нет

- (BNP Paribas) DivDax. Trade 2009-2010 Dividend SwapДокумент10 страниц(BNP Paribas) DivDax. Trade 2009-2010 Dividend SwapaacmasterblasterОценок пока нет

- Bar Cap 3Документ11 страницBar Cap 3Aquila99999Оценок пока нет

- Economics Docs 2022 184258.ashxДокумент65 страницEconomics Docs 2022 184258.ashxTshepo ThaisiОценок пока нет

- FX Options 0907 Poster 1Документ1 страницаFX Options 0907 Poster 1ajayvmehtaОценок пока нет

- 2019 Themes Strategy En-2Документ44 страницы2019 Themes Strategy En-2Yahia Mohammed AbdelatifОценок пока нет

- FX Talking: Ing'S View On The Major Bullish and Bearish Currency ThemesДокумент20 страницFX Talking: Ing'S View On The Major Bullish and Bearish Currency ThemesCiocoiu Vlad AndreiОценок пока нет

- Industrial OutputДокумент7 страницIndustrial OutputAishwarya Mani KachhalОценок пока нет

- Ubs Year Ahead 2024 enДокумент72 страницыUbs Year Ahead 2024 enTony J. Soler100% (1)

- Macroeconomics Update BCAДокумент41 страницаMacroeconomics Update BCAikutmilisОценок пока нет

- Financial Statement Analysis and Security Valuation: - October 19, 2022 Arnt VerriestДокумент62 страницыFinancial Statement Analysis and Security Valuation: - October 19, 2022 Arnt VerriestfelipeОценок пока нет

- Understanding Vietnam - A Look Beyond The Facts and PDFДокумент24 страницыUnderstanding Vietnam - A Look Beyond The Facts and PDFDawood GacayanОценок пока нет

- JPM US Fixed Income Over 2022-05-13 4094360Документ22 страницыJPM US Fixed Income Over 2022-05-13 4094360Kurt ZhangОценок пока нет

- Global Market Outlook - August 2013 - GWMДокумент14 страницGlobal Market Outlook - August 2013 - GWMFauzi DjauhariОценок пока нет

- 8 FullДокумент13 страниц8 FullAnh TranОценок пока нет

- TD CTA Position Tracker 20220421Документ11 страницTD CTA Position Tracker 20220421SubG 08Оценок пока нет

- G10 FX Week Ahead: Tailgating Treasury YieldsДокумент8 страницG10 FX Week Ahead: Tailgating Treasury YieldsrockieballОценок пока нет

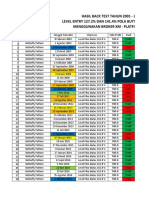

- Hasil Back Test Tahun 2001 - 2022 Level Entry 127.2% Dan 141.4% Pola Butterfly Pattern Menggunakan Broker XM - Platform Mt5Документ4 страницыHasil Back Test Tahun 2001 - 2022 Level Entry 127.2% Dan 141.4% Pola Butterfly Pattern Menggunakan Broker XM - Platform Mt5Nova AnnuristianОценок пока нет

- Roi & RWLДокумент6 страницRoi & RWLNova AnnuristianОценок пока нет

- FOREXXДокумент48 страницFOREXXNova AnnuristianОценок пока нет

- Roi & RWLДокумент6 страницRoi & RWLNova AnnuristianОценок пока нет

- EURUSD Membentuk Pola Shark Pattern Dan Berpotensi BullishДокумент1 страницаEURUSD Membentuk Pola Shark Pattern Dan Berpotensi BullishNova AnnuristianОценок пока нет

- Teknikal Plan XAU & UCAD Juni 17 - 21, 2019Документ1 страницаTeknikal Plan XAU & UCAD Juni 17 - 21, 2019Nova AnnuristianОценок пока нет

- Teknikal Plan 27 - 31 Maret 2019 (Xauusd & Usdcad)Документ1 страницаTeknikal Plan 27 - 31 Maret 2019 (Xauusd & Usdcad)Nova AnnuristianОценок пока нет

- Teknikal Plan 27 - 31 Maret 2019 (Eurusd & Gbpusd)Документ1 страницаTeknikal Plan 27 - 31 Maret 2019 (Eurusd & Gbpusd)Nova AnnuristianОценок пока нет

- Versi IkoДокумент2 страницыVersi IkoNova AnnuristianОценок пока нет

- EURUSD Membentuk Pola Shark Pattern Dan Berpotensi BullishДокумент1 страницаEURUSD Membentuk Pola Shark Pattern Dan Berpotensi BullishNova AnnuristianОценок пока нет

- Ujian SisterДокумент4 страницыUjian SisterNova AnnuristianОценок пока нет

- 9 10sifat Koligatif LarutanДокумент3 страницы9 10sifat Koligatif LarutanNova AnnuristianОценок пока нет

- No. Abs 13 Kelas 12 MIPA-3 (Ikhtiar)Документ3 страницыNo. Abs 13 Kelas 12 MIPA-3 (Ikhtiar)Nova AnnuristianОценок пока нет

- Zimbabwe Booklet May 2012Документ73 страницыZimbabwe Booklet May 2012Willem Dirk KadijkОценок пока нет

- Parent, Inc Actual Financial Statements For 2012 and OlsenДокумент23 страницыParent, Inc Actual Financial Statements For 2012 and OlsenManal ElkhoshkhanyОценок пока нет

- B. Downward UpwardДокумент9 страницB. Downward Upwardtuân okОценок пока нет

- European Union NotesДокумент24 страницыEuropean Union Notesapi-204493496Оценок пока нет

- No$GBAДокумент8 страницNo$GBAHenraОценок пока нет

- Safeguarding Electronic Money FundsДокумент13 страницSafeguarding Electronic Money FundsFelix LeMarcОценок пока нет

- IE 343 Engineering Economics: Lecture 34: Chapter 9 - Replacement Analysis Instructor: Tian NiДокумент38 страницIE 343 Engineering Economics: Lecture 34: Chapter 9 - Replacement Analysis Instructor: Tian NiAnjo VasquezОценок пока нет

- White PaperДокумент41 страницаWhite PaperParnasree ChowdhuryОценок пока нет

- Q4 2011 Earnings Call Company Participants: OperatorДокумент15 страницQ4 2011 Earnings Call Company Participants: Operatorfrontier11Оценок пока нет

- Bloomberg ReferenceДокумент111 страницBloomberg Referencerranjan27Оценок пока нет

- Acct 260 Chapter 12Документ20 страницAcct 260 Chapter 12John Guy100% (1)

- Plum Consulting Valuation of Public Mobile Spectrum at 825 845 MHZ and 870 890 MHZДокумент29 страницPlum Consulting Valuation of Public Mobile Spectrum at 825 845 MHZ and 870 890 MHZsanjeevk05Оценок пока нет

- NCRE - Sample Exam - 2009Документ24 страницыNCRE - Sample Exam - 2009MiaDjojowasito100% (1)

- Chapter 10 Europe, Africa and The Middle EastДокумент45 страницChapter 10 Europe, Africa and The Middle EastDonald Picauly100% (1)

- SBCL Purchase 38+2% DoaДокумент15 страницSBCL Purchase 38+2% DoaVIP smailОценок пока нет

- 2006 FinalДокумент30 страниц2006 Finalriders29Оценок пока нет

- Economy of India: Fdi in Indian Pharma SectorДокумент38 страницEconomy of India: Fdi in Indian Pharma Sectorsandeep patialОценок пока нет

- The Effects of Currency Fluctuations On The EconomyДокумент3 страницыThe Effects of Currency Fluctuations On The EconomyKhairun NisyaОценок пока нет

- C15 Krugman 12e Accessible EdДокумент48 страницC15 Krugman 12e Accessible Ed7ARDELIA GRANDIVA CIPTAMURTIОценок пока нет

- (Rapra Review Reports) S.M. Halliwell-Polymers in Building and Construction-Smithers Rapra Press (2003)Документ150 страниц(Rapra Review Reports) S.M. Halliwell-Polymers in Building and Construction-Smithers Rapra Press (2003)Leandro RosendoОценок пока нет

- The Home DepotДокумент30 страницThe Home DepotAnoop SrivastavaОценок пока нет

- Role of Government in Economic GrowthДокумент26 страницRole of Government in Economic GrowthAbhay BajwaОценок пока нет

- Informe de BullTick Sobre ArgentinaДокумент4 страницыInforme de BullTick Sobre ArgentinaEl DestapeОценок пока нет

- A REIT - 2014 Annual ReportДокумент218 страницA REIT - 2014 Annual Reportvic2clarionОценок пока нет

- Foreign Exchange RateДокумент9 страницForeign Exchange RateDimple DaswaniОценок пока нет

- Pembahasan Soal Materi Akl2 - Chapter 12Документ47 страницPembahasan Soal Materi Akl2 - Chapter 12Ditiya PratamaОценок пока нет

- Aegon Annual Report 2016Документ386 страницAegon Annual Report 2016rohitmahaliОценок пока нет

- Zeke Ashton Apples To ApplesДокумент30 страницZeke Ashton Apples To ApplesValueWalk100% (1)