Вам также может понравиться

- Seminar PPT - Storm Water & Sewerage Design-1 - 2915Документ12 страницSeminar PPT - Storm Water & Sewerage Design-1 - 2915Abhijit Haval100% (1)

- Coordination With Other DepartmentДокумент3 страницыCoordination With Other Departmentdanishsaifi2007Оценок пока нет

- Guidelines For Adopting Multi Use of Stormwater Management FacilitiesДокумент24 страницыGuidelines For Adopting Multi Use of Stormwater Management FacilitiesMohamedОценок пока нет

- Draft Common SSR 2019-20 .01-11-2019 APДокумент186 страницDraft Common SSR 2019-20 .01-11-2019 APvteja214Оценок пока нет

- Unequal Lives DruryДокумент3 страницыUnequal Lives DruryZahid HussainОценок пока нет

- 9.volume IV-Preamble To Price Bid PDFДокумент29 страниц9.volume IV-Preamble To Price Bid PDFHussain ShaikhОценок пока нет

- Analysis of Clause 10CC of Contract AgreementДокумент25 страницAnalysis of Clause 10CC of Contract AgreementMafaka Maxx100% (1)

- DPR ReviewДокумент81 страницаDPR ReviewgallantprakashОценок пока нет

- Design Basis ReportДокумент9 страницDesign Basis ReportRadhika KhandelwalОценок пока нет

- Data Collection FormДокумент16 страницData Collection FormRohit JainОценок пока нет

- Hvac Design Thumb Rules PDFДокумент52 страницыHvac Design Thumb Rules PDFmohd yusuf ansariОценок пока нет

- Part 1 - Unit 1 Introduction To Mechanical and Electrical Building Systems-LockДокумент10 страницPart 1 - Unit 1 Introduction To Mechanical and Electrical Building Systems-LockNicco de VeraОценок пока нет

- Report 3 Operations and Maintenance SystemsДокумент141 страницаReport 3 Operations and Maintenance SystemsAjit PatilОценок пока нет

- Blackall Aerodrome Lighting QuotationДокумент53 страницыBlackall Aerodrome Lighting Quotationgraceenggint8799Оценок пока нет

- SDM College of Engineering and Technology DHARWAD-580002: Case Study of Delhi Metro ProjectДокумент14 страницSDM College of Engineering and Technology DHARWAD-580002: Case Study of Delhi Metro ProjectNikhil LamaniОценок пока нет

- Chapter 56 Highway LightingДокумент56 страницChapter 56 Highway Lightingjaythakar8887Оценок пока нет

- 4646396Документ28 страниц4646396Samuel OnyewuenyiОценок пока нет

- TOR of Airport SampleДокумент5 страницTOR of Airport SampleNal Bikram ThapaОценок пока нет

- Electric Distribution ProcessДокумент45 страницElectric Distribution ProcessJeanfel Pacis TumbagaОценок пока нет

- المواصفات العامة للهاتف - وزارة المواصلاتДокумент22 страницыالمواصفات العامة للهاتف - وزارة المواصلاتAmir AmaraОценок пока нет

- 9 Physical and Non Physical Determinants of City Form PatternДокумент31 страница9 Physical and Non Physical Determinants of City Form Patterntanie100% (8)

- HD - 5.6 Schedule of Electrical RequirementsДокумент83 страницыHD - 5.6 Schedule of Electrical RequirementsGajendra SinghОценок пока нет

- Expansion of Lydd Airport Approved.Документ365 страницExpansion of Lydd Airport Approved.Stop City Airport MasterplanОценок пока нет

- A Perfect Destination To: Meet With SuccessДокумент27 страницA Perfect Destination To: Meet With Successhrithik agnihotriОценок пока нет

- Detailed Method Statement For Erection of PFBДокумент6 страницDetailed Method Statement For Erection of PFBPraveen Prakash100% (1)

- SethiДокумент89 страницSethiankurОценок пока нет

- Lets Go For A Ride Towards Pune!!!: Presented ByДокумент22 страницыLets Go For A Ride Towards Pune!!!: Presented ByPrasad RaiОценок пока нет

- Draft-GUIDELINES-FOR-PLANNING-DESIGN-ROADSHIGHWAY - PROJECTS-KIIFB PDFДокумент123 страницыDraft-GUIDELINES-FOR-PLANNING-DESIGN-ROADSHIGHWAY - PROJECTS-KIIFB PDFAkshay Aithal KandoorОценок пока нет

- Chapter 1 - Foundations of Engineering EconomyДокумент28 страницChapter 1 - Foundations of Engineering EconomyBich Lien PhamОценок пока нет

- PGCILДокумент3 страницыPGCILmahi9892Оценок пока нет

- Latestyearcoursefile Nce043Документ54 страницыLatestyearcoursefile Nce043Mohd AmirОценок пока нет

- Tender Iitjmusp 0532018Документ78 страницTender Iitjmusp 0532018Srini VaSОценок пока нет

- HP Apprsd IPDSDPR - Solan - FinaluploadДокумент108 страницHP Apprsd IPDSDPR - Solan - FinaluploadManoj ManhasОценок пока нет

- Andhra - Pradesh - Govt Rules For Epc ContractsДокумент29 страницAndhra - Pradesh - Govt Rules For Epc Contractsanon_740216180Оценок пока нет

- HSD-1 Commissioning Test Protocol VerDДокумент57 страницHSD-1 Commissioning Test Protocol VerDsonuchakdeОценок пока нет

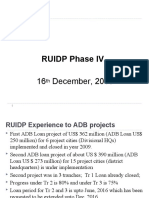

- RUIDP Phase IV - Presentation FinalДокумент15 страницRUIDP Phase IV - Presentation FinalNarendra AjmeraОценок пока нет

- Manhole Head LossesДокумент11 страницManhole Head Lossesjoseph_mscОценок пока нет

- DPR: Detailed Project Reports - NIT Cost Estimate - SOR: Schedule of RatesДокумент70 страницDPR: Detailed Project Reports - NIT Cost Estimate - SOR: Schedule of RatesGirija Sankar PatiОценок пока нет

- Peak Flow Calculation-LunugalaДокумент3 страницыPeak Flow Calculation-LunugalakanishkaОценок пока нет

- A-E SOW FinalTucsonДокумент68 страницA-E SOW FinalTucsonmdtaahОценок пока нет

- MEP Internship Training Report Main PageДокумент40 страницMEP Internship Training Report Main PageHhОценок пока нет

- Report On DamsДокумент37 страницReport On DamsNoli CorralОценок пока нет

- MEP Work PresentationДокумент6 страницMEP Work PresentationdavethiyaguОценок пока нет

- FinalДокумент46 страницFinalSunWanОценок пока нет

- Revision of CPWD Specifications and Schedule of Rates For Ecbc ComplianceДокумент60 страницRevision of CPWD Specifications and Schedule of Rates For Ecbc ComplianceChandan vatsОценок пока нет

- Uttar Pradesh Expressway Toll LevyДокумент11 страницUttar Pradesh Expressway Toll LevynikhilОценок пока нет

- Section7-Conceptual Design and CostingДокумент20 страницSection7-Conceptual Design and CostingtanujaayerОценок пока нет

- Itu-T: The International Identification Plan For Public Networks and SubscriptionsДокумент26 страницItu-T: The International Identification Plan For Public Networks and SubscriptionspluedonОценок пока нет

- CSCEC M&E Works in The Construction Industry (Engineering, Procurement and Construction Contractor)Документ3 страницыCSCEC M&E Works in The Construction Industry (Engineering, Procurement and Construction Contractor)nik haslaОценок пока нет

- Cost dataFY 2018-19Документ88 страницCost dataFY 2018-19Vivek TiwariОценок пока нет

- Drainage EngineeringДокумент72 страницыDrainage EngineeringDominic dominic100% (1)

- 113 Dr. Fixit FastflexДокумент3 страницы113 Dr. Fixit FastflexNaing Ye Htun100% (1)

- Is.2470.1.1985 Septic Tank Part 2Документ29 страницIs.2470.1.1985 Septic Tank Part 2V Jay KrОценок пока нет

- Cipaa PDFДокумент11 страницCipaa PDFdownloademail100% (2)

- Operation and Maintenance of A Substation-Libre PDFДокумент60 страницOperation and Maintenance of A Substation-Libre PDFShareef KhanОценок пока нет

- ECV 401 CAT Two 2013Документ1 страницаECV 401 CAT Two 2013Daniel KariukiОценок пока нет

- Building Energy-Consumption Status Worldwide and The State-Of-The-Art Technologies For Zero-Energy Buildings During The Past DecadeДокумент16 страницBuilding Energy-Consumption Status Worldwide and The State-Of-The-Art Technologies For Zero-Energy Buildings During The Past DecadeRamonn ToporowiczОценок пока нет

- Faires Burden PDFДокумент2 страницыFaires Burden PDFCaleb0% (1)

- Report - Energy Consumption SurveyДокумент30 страницReport - Energy Consumption SurveyEdin MuratiОценок пока нет

- Dokumen - Tips Cec 103 Workshop Technology 1Документ128 страницDokumen - Tips Cec 103 Workshop Technology 1Yusuf MuhammedОценок пока нет

- Measuring Drainage Below Ground in Accordance With ARM4 - An IntrodДокумент32 страницыMeasuring Drainage Below Ground in Accordance With ARM4 - An IntrodMhando IgnasОценок пока нет

- Annex A Requirement Specs - HVLS Fan 20 Feb FinalДокумент3 страницыAnnex A Requirement Specs - HVLS Fan 20 Feb FinalJia WenjieОценок пока нет

- College of Engineering and TechnologyДокумент3 страницыCollege of Engineering and TechnologyShroukAdelMohamedGaribОценок пока нет

- ECBC - Transformer PDFДокумент24 страницыECBC - Transformer PDFSOYAL CHAUHANОценок пока нет

- ToR - Electrical EngineerДокумент4 страницыToR - Electrical EngineerBruno SamosОценок пока нет

- Ethiopia - Wacha-Maji Road Upgrading Project - Appraisal Report 0041-0050Документ10 страницEthiopia - Wacha-Maji Road Upgrading Project - Appraisal Report 0041-0050SISAYОценок пока нет

- S. No. Particulars SD D N A SAДокумент2 страницыS. No. Particulars SD D N A SARAVI RAUSHAN JHAОценок пока нет

- Visvesvaraya Technological University: Internship Report On B.M.R.C.LДокумент30 страницVisvesvaraya Technological University: Internship Report On B.M.R.C.LJinendra Bafna100% (2)

- The-Statesman Delhi - 05-03-2018.@towardstomorrow - 1396-12-14-5-28Документ16 страницThe-Statesman Delhi - 05-03-2018.@towardstomorrow - 1396-12-14-5-28Rahul R KurilОценок пока нет

- ChalanДокумент1 страницаChalandildar123Оценок пока нет

- Delhi Metro Rail Corporation Limited (DMRC) Is A Centre-State PublicДокумент3 страницыDelhi Metro Rail Corporation Limited (DMRC) Is A Centre-State Publicamitmohanty49Оценок пока нет

- Metro PDFДокумент2 страницыMetro PDFYash PratapОценок пока нет

- Delhi Metro Rail: Beyond Mass TransitДокумент5 страницDelhi Metro Rail: Beyond Mass TransitVivek AggarwalОценок пока нет

- Jan Issue 2019Документ64 страницыJan Issue 2019DEBASIS BARMANОценок пока нет

- Research Paper On Delhi MetroДокумент8 страницResearch Paper On Delhi Metroznsgjgvnd100% (1)

- On High Speed RailwaysДокумент25 страницOn High Speed RailwaysNabh AgrawalОценок пока нет

- Curriculum Vitae Pankaj Kapil: Rites LTDДокумент4 страницыCurriculum Vitae Pankaj Kapil: Rites LTDPankaj KapilОценок пока нет

- DPR - Metro - NOV - 2015 - Page 108 & 109 PDFДокумент515 страницDPR - Metro - NOV - 2015 - Page 108 & 109 PDFOm SinghОценок пока нет

- Annexure 21 PDFДокумент17 страницAnnexure 21 PDFchinky_movieОценок пока нет

- Cupid CallingДокумент21 страницаCupid CallingGaurav SharmaОценок пока нет

- BS English 16 - 9 PDFДокумент17 страницBS English 16 - 9 PDFDilip Kumar ThumatiОценок пока нет

- Chennai PDFДокумент1 233 страницыChennai PDFApple AdsОценок пока нет

- CE&CR Magazine June '20Документ60 страницCE&CR Magazine June '20Sudipto PaulОценок пока нет

- Delhi Metro RailДокумент24 страницыDelhi Metro RailTYAGI PROJECTSОценок пока нет

- Harmonization of HR Policies - RoughДокумент119 страницHarmonization of HR Policies - RoughFrancis SoiОценок пока нет

- Delhi Metro Rail Recruitment Official Notification 2018Документ5 страницDelhi Metro Rail Recruitment Official Notification 2018Kshitija100% (3)

- Final Project of DMRC - Collegeprojects1.Blogspot - inДокумент58 страницFinal Project of DMRC - Collegeprojects1.Blogspot - inShiyas IbrahimОценок пока нет

- PGDM 3 Semester.: Delhi Metro Case StudyДокумент11 страницPGDM 3 Semester.: Delhi Metro Case StudyPuja JhaОценок пока нет

- Delhi Meerut RRTS Stations Information by Abhinav SharmaДокумент2 страницыDelhi Meerut RRTS Stations Information by Abhinav SharmaAbhinav SharmaОценок пока нет

- RVNLДокумент8 страницRVNLRakesh SahooОценок пока нет