Вам также может понравиться

- Special Educational Needs, Inclusion and DiversityДокумент665 страницSpecial Educational Needs, Inclusion and DiversityAndrej Hodonj100% (1)

- Indonesia Aesthetic MarketДокумент58 страницIndonesia Aesthetic MarketUntung WidjajaОценок пока нет

- Pareto's Principle: Expand your business with the 80/20 ruleОт EverandPareto's Principle: Expand your business with the 80/20 ruleРейтинг: 5 из 5 звезд5/5 (1)

- Eep306 Assessment 1 FeedbackДокумент2 страницыEep306 Assessment 1 Feedbackapi-354631612Оценок пока нет

- Customer Based Brand EquityДокумент13 страницCustomer Based Brand EquityZeeshan BakshiОценок пока нет

- Aristotle Model of CommunicationДокумент4 страницыAristotle Model of CommunicationSem BulagaОценок пока нет

- International Macroeconomics: Slides For Chapter 11: Exchange Rate Policy and UnemploymentДокумент55 страницInternational Macroeconomics: Slides For Chapter 11: Exchange Rate Policy and UnemploymentLiu ChengОценок пока нет

- Economic Forecast Summary Argentina Oecd Economic Outlook November 2016Документ3 страницыEconomic Forecast Summary Argentina Oecd Economic Outlook November 2016Ciurlic MariaОценок пока нет

- What Is The Economic Outlook For OECD Countries?: An Interim AssessmentДокумент17 страницWhat Is The Economic Outlook For OECD Countries?: An Interim AssessmentJohn RotheОценок пока нет

- The U S Economic Outlook The U.S. Economic OutlookДокумент30 страницThe U S Economic Outlook The U.S. Economic OutlookZerohedge100% (3)

- Monthly Economic Bulletin: January 2011Документ15 страницMonthly Economic Bulletin: January 2011lrochekellyОценок пока нет

- ImfДокумент19 страницImfOsama RiazОценок пока нет

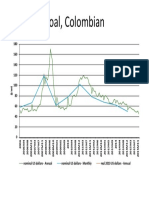

- Coal Price Chart 2006-2015Документ1 страницаCoal Price Chart 2006-2015Iván Andrés Verbel MontesОценок пока нет

- Coal Price Chart 2006-2015Документ1 страницаCoal Price Chart 2006-2015Iván Andrés Verbel MontesОценок пока нет

- Malaysia - Economic Trends: Gross Domestic ProductДокумент5 страницMalaysia - Economic Trends: Gross Domestic ProductyuiclynesОценок пока нет

- Current Edition Contains: 1: SugarДокумент14 страницCurrent Edition Contains: 1: SugarJan KaskaОценок пока нет

- Romania Country Report Highlights Strong Growth But Widens DeficitsДокумент15 страницRomania Country Report Highlights Strong Growth But Widens DeficitsClaudia FilipОценок пока нет

- Principles of Economics: Monopoly and Antitrust PolicyДокумент17 страницPrinciples of Economics: Monopoly and Antitrust Policyaryan mittalОценок пока нет

- Affordable HousingДокумент9 страницAffordable HousingbernardchickeyОценок пока нет

- Economic Forecast Summary South Africa Oecd Economic OutlookДокумент3 страницыEconomic Forecast Summary South Africa Oecd Economic OutlookVirali JadejaОценок пока нет

- Euromonitorinternationalhongkongtoyfair201509122014 150119110421 Conversion Gate02Документ29 страницEuromonitorinternationalhongkongtoyfair201509122014 150119110421 Conversion Gate02pmcardosoОценок пока нет

- 01_Commodity_price_volatilityДокумент12 страниц01_Commodity_price_volatilityjoeОценок пока нет

- Ekonomski Pregled OECD-aДокумент26 страницEkonomski Pregled OECD-aTportal.hrОценок пока нет

- J&J Brand Strategy TemplateДокумент35 страницJ&J Brand Strategy TemplateAmit SahaОценок пока нет

- Business Investment in The United StatesДокумент21 страницаBusiness Investment in The United StatesdoguОценок пока нет

- FDI Impact on Zimbabwe's Trade BalanceДокумент7 страницFDI Impact on Zimbabwe's Trade BalanceRodwellОценок пока нет

- The Evolution of Central BankingДокумент21 страницаThe Evolution of Central BankingKingKrexОценок пока нет

- Economic Developments and Investment Environment in TurkeyДокумент30 страницEconomic Developments and Investment Environment in TurkeyPolat ArıОценок пока нет

- Ya Mar One 060309Документ42 страницыYa Mar One 060309Zerohedge100% (2)

- Global Economic Prospects Jun2020 PressHighlights Chp4Документ3 страницыGlobal Economic Prospects Jun2020 PressHighlights Chp4CristianMilciadesОценок пока нет

- How Participation in Global Value Chains Can Boost Productivity GrowthДокумент17 страницHow Participation in Global Value Chains Can Boost Productivity GrowthPatricia GarciaОценок пока нет

- Macro L6Документ16 страницMacro L6naspgОценок пока нет

- Economy: 2009 Long Island Index EДокумент12 страницEconomy: 2009 Long Island Index EKVОценок пока нет

- Slide 1: Global Fiscal Crisis of 2007-08Документ12 страницSlide 1: Global Fiscal Crisis of 2007-08RUSHABH DESAIОценок пока нет

- Economic Highlights - Leading Index Rebounded in March, Pointing To A Resilient Economic Growth in 2H 2010 - 17/5/2010Документ2 страницыEconomic Highlights - Leading Index Rebounded in March, Pointing To A Resilient Economic Growth in 2H 2010 - 17/5/2010Rhb InvestОценок пока нет

- SWDY: A. Stotz Profitable Growth: Excellent Profitability Poor GrowthДокумент5 страницSWDY: A. Stotz Profitable Growth: Excellent Profitability Poor GrowthThủy NguyễnОценок пока нет

- Europe 2020 Targets: Employment Rate: 1. Key Statistical IndicatorsДокумент7 страницEurope 2020 Targets: Employment Rate: 1. Key Statistical IndicatorsAlina ComanescuОценок пока нет

- MAEcono Pol 3Документ117 страницMAEcono Pol 3Edimarf SatumboОценок пока нет

- Dubai Industrial Strategy 2030 PDFДокумент12 страницDubai Industrial Strategy 2030 PDFBashar OurabiОценок пока нет

- The Global Paint and Coatings Industry: Marke T Repor TДокумент6 страницThe Global Paint and Coatings Industry: Marke T Repor TCaptain PriceОценок пока нет

- Bangladesh: Selected Indicators: Trend of Real GDP Growth and GDP Per Capita 1/ Trend of Demographic Indicators 2Документ6 страницBangladesh: Selected Indicators: Trend of Real GDP Growth and GDP Per Capita 1/ Trend of Demographic Indicators 2MD. ISRAFIL PALASHОценок пока нет

- Reading Lesson 7Документ5 страницReading Lesson 7AnshumanОценок пока нет

- CITATION HTT /L 1033Документ55 страницCITATION HTT /L 1033Miskatul ArafatОценок пока нет

- Predicting The Markets Nov2020 - ch4Документ29 страницPredicting The Markets Nov2020 - ch4scribbugОценок пока нет

- Industry Outlook March2011Документ4 страницыIndustry Outlook March2011iminvisibleОценок пока нет

- Gdansk 2015 LO - PrezentacjaДокумент18 страницGdansk 2015 LO - PrezentacjaAndreaAguerreОценок пока нет

- International Macroeconomics: Slides For Chapter 5: Uncertainty and The Current AccountДокумент5 страницInternational Macroeconomics: Slides For Chapter 5: Uncertainty and The Current AccountM Kaderi KibriaОценок пока нет

- International Macroeconomics: Slides For Chapter 5: Uncertainty and The Current AccountДокумент5 страницInternational Macroeconomics: Slides For Chapter 5: Uncertainty and The Current AccountLiu ChengОценок пока нет

- DSP Midcap Fund Mar 2023Документ44 страницыDSP Midcap Fund Mar 2023Aakash ChhariaОценок пока нет

- Us Charts CondДокумент8 страницUs Charts CondJonathan NixonОценок пока нет

- Final Porfolio PaperДокумент15 страницFinal Porfolio PaperDeep DualОценок пока нет

- 2017 Budget-Country Presentation FormatДокумент59 страниц2017 Budget-Country Presentation FormatYhane Hermann BackОценок пока нет

- Economic Forecast ColombiaДокумент3 страницыEconomic Forecast Colombiasuper_sumoОценок пока нет

- Aalberts 2020Документ128 страницAalberts 2020gaja babaОценок пока нет

- Hospital Cost Drivers enДокумент80 страницHospital Cost Drivers enWashington AmericaОценок пока нет

- Trends: S Upply DemandДокумент42 страницыTrends: S Upply DemandThoughts and More ThoughtsОценок пока нет

- The Impact of Macroeconomic Factors On Trade Balance in VietnamДокумент19 страницThe Impact of Macroeconomic Factors On Trade Balance in Vietnamhnaan rehanОценок пока нет

- UNILEVER CHARTS 2018 FINANCIAL AND OPERATING HIGHLIGHTSДокумент17 страницUNILEVER CHARTS 2018 FINANCIAL AND OPERATING HIGHLIGHTSLala BananaОценок пока нет

- On Falling Neutral Real Rates Fiscal Policy and The Risk of Secular StagnationДокумент68 страницOn Falling Neutral Real Rates Fiscal Policy and The Risk of Secular StagnationjackefellerОценок пока нет

- Group of Seven: Meetings of G-7 Finance Ministers and Central Bank Governors February 5 6, 2010 Iqaluit, CanadaДокумент21 страницаGroup of Seven: Meetings of G-7 Finance Ministers and Central Bank Governors February 5 6, 2010 Iqaluit, Canadarakesh s gОценок пока нет

- The Australian Economy and Financial Markets: July 2019Документ33 страницыThe Australian Economy and Financial Markets: July 2019Amita SinghОценок пока нет

- Mughal Rule Muslin, Silk Pearl India Pakistan: TH THДокумент19 страницMughal Rule Muslin, Silk Pearl India Pakistan: TH THDigonto DasОценок пока нет

- Economic Highlights - Leading Index Slowed Down in May, Pointing To A More Moderate Economic Growth in 2H 2010 - 19/7/2010Документ2 страницыEconomic Highlights - Leading Index Slowed Down in May, Pointing To A More Moderate Economic Growth in 2H 2010 - 19/7/2010Rhb InvestОценок пока нет

- Annual Report 2018Документ362 страницыAnnual Report 2018adnan ahmadОценок пока нет

- PGDIB Course Syllabus 102 Shariah Framework For Islamic Banking, UpdatedДокумент3 страницыPGDIB Course Syllabus 102 Shariah Framework For Islamic Banking, UpdatedM Kaderi KibriaОценок пока нет

- International Macroeconomics: Slides For Chapter 8: International Capital Market IntegrationДокумент54 страницыInternational Macroeconomics: Slides For Chapter 8: International Capital Market IntegrationM Kaderi KibriaОценок пока нет

- International Macroeconomics: Slides For Chapter 7: Twin Deficits: Fiscal Deficits and Current Account ImbalancesДокумент74 страницыInternational Macroeconomics: Slides For Chapter 7: Twin Deficits: Fiscal Deficits and Current Account ImbalancesM Kaderi KibriaОценок пока нет

- International Macroeconomics: Slides For Chapter 3: Theory of Current Account DeterminationДокумент41 страницаInternational Macroeconomics: Slides For Chapter 3: Theory of Current Account DeterminationM Kaderi KibriaОценок пока нет

- Best Practice Financial Modeling 2015Документ2 страницыBest Practice Financial Modeling 2015M Kaderi KibriaОценок пока нет

- International Macroeconomics: Slides For Chapter 5: Uncertainty and The Current AccountДокумент5 страницInternational Macroeconomics: Slides For Chapter 5: Uncertainty and The Current AccountM Kaderi KibriaОценок пока нет

- International Macroeconomics: Slides For Chapter 10Документ37 страницInternational Macroeconomics: Slides For Chapter 10M Kaderi KibriaОценок пока нет

- International Macroeconomics: Slides For Chapter 6: External Adjustment in Small and Large EconomiesДокумент34 страницыInternational Macroeconomics: Slides For Chapter 6: External Adjustment in Small and Large EconomiesM Kaderi KibriaОценок пока нет

- International Macroeconomics: Slides For Chapter 2: Current Account SustainabilityДокумент8 страницInternational Macroeconomics: Slides For Chapter 2: Current Account SustainabilityM Kaderi KibriaОценок пока нет

- International Macroeconomics: Slides For Chapter 1: Global ImbalancesДокумент54 страницыInternational Macroeconomics: Slides For Chapter 1: Global ImbalancesM Kaderi KibriaОценок пока нет

- Real Exchange Rate DeterminantsДокумент55 страницReal Exchange Rate DeterminantsM Kaderi KibriaОценок пока нет

- TeachingRatings DescriptionДокумент1 страницаTeachingRatings DescriptionJesse SeSeОценок пока нет

- Nominal Exchange Rates and Monetary Fundamentals - JIE 01Документ24 страницыNominal Exchange Rates and Monetary Fundamentals - JIE 01M Kaderi KibriaОценок пока нет

- Il Ar 2009Документ78 страницIl Ar 2009Md Redhwan Sidd KhanОценок пока нет

- Foreign Investment in Bangladesh: Section - IДокумент3 страницыForeign Investment in Bangladesh: Section - IM Kaderi KibriaОценок пока нет

- Why Bangladesh: PharmaceuticalДокумент2 страницыWhy Bangladesh: PharmaceuticalM Kaderi KibriaОценок пока нет

- 05 ACI Annual Report 2011 PDFДокумент169 страниц05 ACI Annual Report 2011 PDFM Kaderi KibriaОценок пока нет

- National Australia Bank AR 2002Документ200 страницNational Australia Bank AR 2002M Kaderi KibriaОценок пока нет

- Inland Container Terminals Boost Bangladesh TradeДокумент25 страницInland Container Terminals Boost Bangladesh TradeM Kaderi KibriaОценок пока нет

- Assignment 1 - ACCT20071 - T1 2016 1Документ2 страницыAssignment 1 - ACCT20071 - T1 2016 1M Kaderi KibriaОценок пока нет

- BB Gudline Forex Transaction Vol - 2Документ145 страницBB Gudline Forex Transaction Vol - 2M Kaderi Kibria0% (1)

- Ban Glades Hi TV Channels IndustryДокумент19 страницBan Glades Hi TV Channels IndustryShonkor ShujonОценок пока нет

- BOI - Investment Board Act 1989Документ38 страницBOI - Investment Board Act 1989M Kaderi KibriaОценок пока нет

- Sanchez RoblesДокумент19 страницSanchez RoblesM Kaderi KibriaОценок пока нет

- Accounting For Decision Making Lecture 11 To 68Документ26 страницAccounting For Decision Making Lecture 11 To 68M Kaderi KibriaОценок пока нет

- Finding Annuity ValueДокумент2 страницыFinding Annuity ValueM Kaderi KibriaОценок пока нет

- Cocacola Case Bus 401Документ8 страницCocacola Case Bus 401M Kaderi KibriaОценок пока нет

- ALDI Growth Announcment FINAL 2.8Документ2 страницыALDI Growth Announcment FINAL 2.8Shengulovski IvanОценок пока нет

- Final Activity 4 Theology 1. JOB Does Faith in God Eliminate Trials?Документ3 страницыFinal Activity 4 Theology 1. JOB Does Faith in God Eliminate Trials?Anna May BatasОценок пока нет

- CHEM205 Review 8Документ5 страницCHEM205 Review 8Starlyn RodriguezОценок пока нет

- Biographies of Indian EntreprenaursДокумент72 страницыBiographies of Indian EntreprenaursSidd Bids60% (5)

- How K P Pinpoint Events Prasna PDFДокумент129 страницHow K P Pinpoint Events Prasna PDFRavindra ChandelОценок пока нет

- Why EIA is Important for Development ProjectsДокумент19 страницWhy EIA is Important for Development Projectsvivek377Оценок пока нет

- Learn Financial Accounting Fast with TallyДокумент1 страницаLearn Financial Accounting Fast with Tallyavinash guptaОценок пока нет

- Vodafone service grievance unresolvedДокумент2 страницыVodafone service grievance unresolvedSojan PaulОценок пока нет

- Mobile Pixels v. Schedule A - Complaint (D. Mass.)Документ156 страницMobile Pixels v. Schedule A - Complaint (D. Mass.)Sarah BursteinОценок пока нет

- Human Rights and Human Tissue - The Case of Sperm As Property - Oxford HandbooksДокумент25 страницHuman Rights and Human Tissue - The Case of Sperm As Property - Oxford HandbooksExtreme TronersОценок пока нет

- Can You Dribble The Ball Like A ProДокумент4 страницыCan You Dribble The Ball Like A ProMaradona MatiusОценок пока нет

- Penyebaran Fahaman Bertentangan Akidah Islam Di Media Sosial Dari Perspektif Undang-Undang Dan Syariah Di MalaysiaДокумент12 страницPenyebaran Fahaman Bertentangan Akidah Islam Di Media Sosial Dari Perspektif Undang-Undang Dan Syariah Di Malaysia2023225596Оценок пока нет

- Application For A US PassportДокумент6 страницApplication For A US PassportAbu Hamza SidОценок пока нет

- Social media types for media literacyДокумент28 страницSocial media types for media literacyMa. Shantel CamposanoОценок пока нет

- Northern Nigeria Media History OverviewДокумент7 страницNorthern Nigeria Media History OverviewAdetutu AnnieОценок пока нет

- Network Design Decisions FrameworkДокумент26 страницNetwork Design Decisions Frameworkaditya nemaОценок пока нет

- Account statement for Rinku MeherДокумент24 страницыAccount statement for Rinku MeherRinku MeherОценок пока нет

- Bautista CL MODULEДокумент2 страницыBautista CL MODULETrisha Anne Aranzaso BautistaОценок пока нет

- AIS 10B TimetableДокумент1 страницаAIS 10B TimetableAhmed FadlallahОценок пока нет

- High-Performance Work Practices: Labor UnionДокумент2 страницыHigh-Performance Work Practices: Labor UnionGabriella LomanorekОценок пока нет

- ERP in Apparel IndustryДокумент17 страницERP in Apparel IndustrySuman KumarОценок пока нет

- Words and Lexemes PDFДокумент48 страницWords and Lexemes PDFChishmish DollОценок пока нет

- Fe en Accion - Morris VendenДокумент734 страницыFe en Accion - Morris VendenNicolas BertoaОценок пока нет

- Pharma: Conclave 2018Документ4 страницыPharma: Conclave 2018Abhinav SahaniОценок пока нет

- Action Plan for Integrated Waste Management in SaharanpurДокумент5 страницAction Plan for Integrated Waste Management in SaharanpuramitОценок пока нет

- Hwa Tai AR2015 (Bursa)Документ104 страницыHwa Tai AR2015 (Bursa)Muhammad AzmanОценок пока нет