Вам также может понравиться

- GM Foreign Exchange HedgeДокумент4 страницыGM Foreign Exchange HedgeRima Chakravarty Sonde100% (1)

- Trading Course DetailsДокумент9 страницTrading Course DetailsAnonymous O6q0dCOW6Оценок пока нет

- Quiz 2 Compound Financial Instruments Notes PayableДокумент17 страницQuiz 2 Compound Financial Instruments Notes PayableRey Clarence BanggayanОценок пока нет

- Chapter 08 Risk and Rates of ReturnДокумент48 страницChapter 08 Risk and Rates of ReturnNaida's StuffОценок пока нет

- Fin 425 Final NIKEДокумент11 страницFin 425 Final NIKEcuterahaОценок пока нет

- Module 6 Income Taxes For Corporations - Part 1Документ12 страницModule 6 Income Taxes For Corporations - Part 1Maricar DimayugaОценок пока нет

- Introduction To M&A With Piramal Abbott DealДокумент22 страницыIntroduction To M&A With Piramal Abbott DealSachidanand Singh100% (2)

- Eclectica Absolute Macro Fund: Manager CommentДокумент3 страницыEclectica Absolute Macro Fund: Manager Commentfreemind3682Оценок пока нет

- Al Ahli Bank of Kuwait - Egypt - MMF - November 2017 - English - Monthly ReportДокумент1 страницаAl Ahli Bank of Kuwait - Egypt - MMF - November 2017 - English - Monthly ReportSobolОценок пока нет

- Outlook For The SMSF SectorДокумент13 страницOutlook For The SMSF SectorRomeoОценок пока нет

- Using Big Data To Improve Clinical CareДокумент32 страницыUsing Big Data To Improve Clinical CareXiaodong WangОценок пока нет

- 95 - Emerging India Portfolio-March2019 - Final Email VersionДокумент22 страницы95 - Emerging India Portfolio-March2019 - Final Email VersionTarunAnandaniОценок пока нет

- Apollo Credit Market Outlook Jul23Документ157 страницApollo Credit Market Outlook Jul23supОценок пока нет

- Multivariate Time Series Forecasting of Crude PalmДокумент10 страницMultivariate Time Series Forecasting of Crude PalmJose FerreiraОценок пока нет

- J.C. Parets, CMTДокумент25 страницJ.C. Parets, CMTPunit TewaniОценок пока нет

- SSRNДокумент7 страницSSRNjoystocks777Оценок пока нет

- Indian Stock Market AnalysisДокумент36 страницIndian Stock Market AnalysisTushar GangolyОценок пока нет

- Indian Fixed Income Market Update DSP Nov 13Документ2 страницыIndian Fixed Income Market Update DSP Nov 13Anubhav TripathiОценок пока нет

- MEF Analysis UI Claims - March 2020Документ2 страницыMEF Analysis UI Claims - March 2020Dave AllenОценок пока нет

- Risk and Return Models: Equity and DebtДокумент24 страницыRisk and Return Models: Equity and Debtyadavmihir63Оценок пока нет

- Click To Edit Master Title Style: Ambit Good & Clean Midcap FundДокумент20 страницClick To Edit Master Title Style: Ambit Good & Clean Midcap Fundksprakash1990Оценок пока нет

- Portformulas: Formulaic Trending Monthly AbstractДокумент5 страницPortformulas: Formulaic Trending Monthly Abstractdiane_estes937Оценок пока нет

- ExchangeRateForecasts 0914 PDFДокумент5 страницExchangeRateForecasts 0914 PDFPavala AyyanarОценок пока нет

- Update On IDFC Arbitrage FundДокумент6 страницUpdate On IDFC Arbitrage FundGОценок пока нет

- Solr and Lucene Search RevolutionДокумент27 страницSolr and Lucene Search RevolutionErvin MillerОценок пока нет

- Tracking Financial ConditionsДокумент14 страницTracking Financial ConditionsSathishОценок пока нет

- NTDOP One Pager Jun'22Документ3 страницыNTDOP One Pager Jun'22Deepak GoyalОценок пока нет

- Athenian Shipbrokers S.A.: Baltic Dry IndexДокумент17 страницAthenian Shipbrokers S.A.: Baltic Dry IndexgeorgevarsasОценок пока нет

- SageOne Investor Memo May 2018Документ10 страницSageOne Investor Memo May 2018Akhil ParekhОценок пока нет

- CME - Comparing E-Minis and ETFs - Sep2012 PDFДокумент8 страницCME - Comparing E-Minis and ETFs - Sep2012 PDFbearsqОценок пока нет

- Inflation Rates: The Cost of LivingДокумент6 страницInflation Rates: The Cost of LivingAnonymous QKHeLscy2kОценок пока нет

- Jan-12 Sep-13 Jun-13 Mar-13 Jan-13 Sep-14 Jun-14 Mar-14 Dec-14 Sep-15 Jun-15 Mar-15 Dec-13 Oct-16 Jun-16 Mar-17 Jan-18 Jun-18 Dec-18 YearДокумент4 страницыJan-12 Sep-13 Jun-13 Mar-13 Jan-13 Sep-14 Jun-14 Mar-14 Dec-14 Sep-15 Jun-15 Mar-15 Dec-13 Oct-16 Jun-16 Mar-17 Jan-18 Jun-18 Dec-18 YearsyedОценок пока нет

- The Global Liquidity Tracker - 22 Apr 22Документ13 страницThe Global Liquidity Tracker - 22 Apr 22Apurva ShethОценок пока нет

- Athenian-Shipbrokers-April 2013Документ18 страницAthenian-Shipbrokers-April 2013Nguyen Le Thu HaОценок пока нет

- Novus OverlapДокумент8 страницNovus OverlaptabbforumОценок пока нет

- Southeast Texas Labor StatisticsДокумент1 страницаSoutheast Texas Labor StatisticsCharlie FoxworthОценок пока нет

- Information Technology Internal AssessmentДокумент17 страницInformation Technology Internal AssessmentAudrey RolandОценок пока нет

- Due Diligence ReportДокумент45 страницDue Diligence ReportMarc Angelo DavidОценок пока нет

- Part 2.4 InvestmentДокумент8 страницPart 2.4 InvestmentSara MohamedОценок пока нет

- HCMF Investor Letter October 2009 FINALДокумент24 страницыHCMF Investor Letter October 2009 FINALAbsolute Return100% (1)

- Accommodation Supply Analysis in Launceston Part 1Документ34 страницыAccommodation Supply Analysis in Launceston Part 1The ExaminerОценок пока нет

- Lupin Corporate Governance EthicsДокумент13 страницLupin Corporate Governance Ethicshagar sudhaОценок пока нет

- GUT Case 1Документ2 страницыGUT Case 1Jack AtellОценок пока нет

- Gmo - For Whom The Bond TollsДокумент8 страницGmo - For Whom The Bond Tollsfreemind3682Оценок пока нет

- Research Speak - 16-04-2010Документ12 страницResearch Speak - 16-04-2010A_KinshukОценок пока нет

- Portførmulas: The Formulaic Trending Monthly AbstractДокумент11 страницPortførmulas: The Formulaic Trending Monthly Abstractdiane_estes937Оценок пока нет

- Company For The Attention of E-Mail Date: Cannerweg 123 6213 BA Maastricht The NetherlandsДокумент4 страницыCompany For The Attention of E-Mail Date: Cannerweg 123 6213 BA Maastricht The NetherlandsrobertionОценок пока нет

- Time Sheet - Janaury2018 ShahidДокумент56 страницTime Sheet - Janaury2018 ShahidJunaidОценок пока нет

- Southern Water Corp Financial Case Study MCU Student Facing 17052020Документ102 страницыSouthern Water Corp Financial Case Study MCU Student Facing 17052020rehmatullah.idreesiОценок пока нет

- Global Commodity Prices, Monetary Transmission, and Exchange Rate Pass-Through in The Pacific IslandsДокумент16 страницGlobal Commodity Prices, Monetary Transmission, and Exchange Rate Pass-Through in The Pacific IslandslukeniaОценок пока нет

- Risk and Return: Chapter OutlineДокумент6 страницRisk and Return: Chapter OutlineThuyển ThuyểnОценок пока нет

- 1st Forecasting Group AaaignmentДокумент9 страниц1st Forecasting Group Aaaignmentpardeep.prd77Оценок пока нет

- Copyright and The Evolving Learning Materials Market - Campus Stores CanadaДокумент6 страницCopyright and The Evolving Learning Materials Market - Campus Stores CanadaAn Michael Powell100% (2)

- Statistical Inquiry 1Документ4 страницыStatistical Inquiry 1Mavel DesamparadoОценок пока нет

- Stat Chapter 1Документ28 страницStat Chapter 1Hamza AbduremanОценок пока нет

- Central Bank Monetary Policy Analysis: - Guillermo Varela HerreraДокумент6 страницCentral Bank Monetary Policy Analysis: - Guillermo Varela HerreraGuillermo VarelaОценок пока нет

- The Value of Petroleum Resources Analysis of Cash Flows and UncertainitiesДокумент8 страницThe Value of Petroleum Resources Analysis of Cash Flows and UncertainitiesDebasishОценок пока нет

- 1ST ASSIGNMENT ForecastingДокумент9 страниц1ST ASSIGNMENT Forecastingpardeep.prd77Оценок пока нет

- Monthly Fund Performance Update Aia International Small Cap FundДокумент1 страницаMonthly Fund Performance Update Aia International Small Cap FundLam Kah MengОценок пока нет

- FactsheetДокумент1 страницаFactsheetAdam MuhammadОценок пока нет

- Project PlanДокумент1 страницаProject PlanSHIVAM POOJARAОценок пока нет

- Resource Planning and Optimisation ReportДокумент27 страницResource Planning and Optimisation ReportRasika DeshpandeОценок пока нет

- The Global Liquidity Tracker - 06 May 22Документ8 страницThe Global Liquidity Tracker - 06 May 22Apurva ShethОценок пока нет

- Sharot Korn Dolan How Unrealistic Optimism Maintained in The Face of Ukmss-36575 PDFДокумент15 страницSharot Korn Dolan How Unrealistic Optimism Maintained in The Face of Ukmss-36575 PDFAnonymous pb0lJ4n5jОценок пока нет

- Aejfinal PDFДокумент31 страницаAejfinal PDFAnonymous pb0lJ4n5jОценок пока нет

- Conditional Dependence in Post-Crisis Markets: Dispersion and Correlation Skew TradesДокумент35 страницConditional Dependence in Post-Crisis Markets: Dispersion and Correlation Skew TradesAnonymous pb0lJ4n5jОценок пока нет

- David Dodge: The Bank of Canada and Monetary Policy: Future DirectionsДокумент4 страницыDavid Dodge: The Bank of Canada and Monetary Policy: Future DirectionsAnonymous pb0lJ4n5jОценок пока нет

- Empirical Evidence On Volatility EstimatorsДокумент38 страницEmpirical Evidence On Volatility EstimatorsAnonymous pb0lJ4n5jОценок пока нет

- NAG Library Function Document Nag - Quasi - Init (G05ylc) : 1 PurposeДокумент3 страницыNAG Library Function Document Nag - Quasi - Init (G05ylc) : 1 PurposeAnonymous pb0lJ4n5jОценок пока нет

- The Decision To Concentrate: Active Management, Manager Skill, and Portfolio SizeДокумент51 страницаThe Decision To Concentrate: Active Management, Manager Skill, and Portfolio SizeAnonymous pb0lJ4n5jОценок пока нет

- Phenomenology of The Interest Rate CurveДокумент32 страницыPhenomenology of The Interest Rate CurveAnonymous pb0lJ4n5jОценок пока нет

- SSRN Id2606345Документ41 страницаSSRN Id2606345Anonymous pb0lJ4n5jОценок пока нет

- SSRN Id2661752Документ98 страницSSRN Id2661752Anonymous pb0lJ4n5jОценок пока нет

- How To Evaluate Trading SystemsДокумент19 страницHow To Evaluate Trading Systemsalexbernal0Оценок пока нет

- Evaluation and Ranking of Market ForecastersДокумент26 страницEvaluation and Ranking of Market ForecastersAnonymous pb0lJ4n5jОценок пока нет

- Invest Europe Activity Data Report 2021Документ83 страницыInvest Europe Activity Data Report 2021xok panyaОценок пока нет

- Chandan Sharma Project11Документ92 страницыChandan Sharma Project11Chandan SharmaОценок пока нет

- Case Study No Mod (Iv) Working Capital Turnover MethodДокумент1 страницаCase Study No Mod (Iv) Working Capital Turnover Methodamarlata_kumariОценок пока нет

- Dangote Cement - Benue Cement Company OfferДокумент2 страницыDangote Cement - Benue Cement Company OfferbiodОценок пока нет

- European Bond Futures 2006Документ10 страницEuropean Bond Futures 2006deepdish7Оценок пока нет

- Radford Alert Iss Burn Rate Limits For 2014 PDFДокумент5 страницRadford Alert Iss Burn Rate Limits For 2014 PDFjoeymcyoungОценок пока нет

- Simple Interest Answers 1Документ10 страницSimple Interest Answers 1Wasfa AhmadОценок пока нет

- Lesson 1 Introduction To Agricultural MarketingДокумент3 страницыLesson 1 Introduction To Agricultural MarketingSittie Ainah MacapundagОценок пока нет

- Depreciation, DepletionДокумент2 страницыDepreciation, DepletionHassan AdamОценок пока нет

- Financial Management FM Final PaperДокумент13 страницFinancial Management FM Final PaperSaqib AliОценок пока нет

- SB (NZD/SGD) SB ($/SGD) X SB (NZD/$) .6135 X 1.3751 .8436Документ2 страницыSB (NZD/SGD) SB ($/SGD) X SB (NZD/$) .6135 X 1.3751 .8436Saffa AbidОценок пока нет

- Chapter 4 BondДокумент60 страницChapter 4 BondSRAR Nurul HudaОценок пока нет

- الأزمة المالية العالمية 2008 جذورها و تداعياتها ساعد مرابط PDFДокумент15 страницالأزمة المالية العالمية 2008 جذورها و تداعياتها ساعد مرابط PDFساعدОценок пока нет

- Course 2 Sample Exam Questions: y Units of BroccoliДокумент47 страницCourse 2 Sample Exam Questions: y Units of BroccoliEden ZapicoОценок пока нет

- Options Open Interest Analysis SimplifiedДокумент17 страницOptions Open Interest Analysis SimplifiedNaveenОценок пока нет

- Chapter 12 - Leverage - Text and End of Chapter Questions - 1Документ39 страницChapter 12 - Leverage - Text and End of Chapter Questions - 1naimenimОценок пока нет

- Shareholder MaximizationДокумент12 страницShareholder MaximizationROMMEL ROYCE CADAPAN100% (1)

- Hills, Hutman, Et Miles, 2008, The Evolution and Development of Entrepreneurial MarketingДокумент14 страницHills, Hutman, Et Miles, 2008, The Evolution and Development of Entrepreneurial MarketingMaalejОценок пока нет

- Hyundai Motor Company 1q 2022 Consolidated FinalДокумент61 страницаHyundai Motor Company 1q 2022 Consolidated FinalNitesh SinghОценок пока нет

- Unit Test 11: Name - ClassДокумент3 страницыUnit Test 11: Name - ClassAkaki saneblidzeОценок пока нет

- StudentДокумент37 страницStudentChelsy Santos100% (1)

- 04 Homework - Answer KeyДокумент3 страницы04 Homework - Answer KeyVeralou UrbinoОценок пока нет

- Historical Financial Analysis - CA Rajiv SinghДокумент78 страницHistorical Financial Analysis - CA Rajiv Singhవిజయ్ పి100% (1)

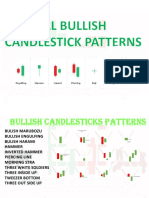

- All Bullish Candlestick Pattern by Optrading00 Telegram Optrading00Документ25 страницAll Bullish Candlestick Pattern by Optrading00 Telegram Optrading00Samitm TamhankarОценок пока нет