Вам также может понравиться

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)От EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Рейтинг: 3.5 из 5 звезд3.5/5 (17)

- Build Size and Aesthetics with the 6-Week Hype Gains Hypertrophy ProgramДокумент21 страницаBuild Size and Aesthetics with the 6-Week Hype Gains Hypertrophy ProgramDanCurtis100% (1)

- FDA Sterile Product Manufacturing GuidelinesДокумент63 страницыFDA Sterile Product Manufacturing GuidelinesSmartishag Bediako100% (2)

- How to Calculate PayrollДокумент87 страницHow to Calculate PayrollMichael John D. Natabla100% (1)

- 27 Tds Calculator Rate ChartДокумент5 страниц27 Tds Calculator Rate ChartasareereОценок пока нет

- C.H. Padliya & Co.: Chartered AccountantsДокумент13 страницC.H. Padliya & Co.: Chartered AccountantsSarat KumarОценок пока нет

- Age Discrimination PDFДокумент20 страницAge Discrimination PDFMd. Rezoan ShoranОценок пока нет

- Keys To Biblical CounselingДокумент7 страницKeys To Biblical CounselingDavid Salazar100% (6)

- Disclosure To Promote The Right To InformationДокумент16 страницDisclosure To Promote The Right To InformationSarat KumarОценок пока нет

- Introduction of MaintenanceДокумент35 страницIntroduction of Maintenanceekhwan82100% (1)

- Small Gas Turbines 4 LubricationДокумент19 страницSmall Gas Turbines 4 LubricationValBMSОценок пока нет

- Equipment Operation and MaintenanceДокумент2 страницыEquipment Operation and MaintenanceSarat KumarОценок пока нет

- Vasudeva PunyahavachanaДокумент15 страницVasudeva PunyahavachanaSridhar VenkatakrishnaОценок пока нет

- Ups Installation Method StatementДокумент197 страницUps Installation Method StatementehteshamОценок пока нет

- TDS TCSДокумент231 страницаTDS TCSNarinderpal SinghОценок пока нет

- Presentation On Data Integrity in PharmaДокумент80 страницPresentation On Data Integrity in Pharmaskvemula67% (3)

- D Formation Damage StimCADE FDAДокумент30 страницD Formation Damage StimCADE FDAEmmanuel EkwohОценок пока нет

- INTERNET STANDARDSДокумент18 страницINTERNET STANDARDSDawn HaneyОценок пока нет

- INTERNET STANDARDSДокумент18 страницINTERNET STANDARDSDawn HaneyОценок пока нет

- INTERNET STANDARDSДокумент18 страницINTERNET STANDARDSDawn HaneyОценок пока нет

- INTERNET STANDARDSДокумент18 страницINTERNET STANDARDSDawn HaneyОценок пока нет

- INTERNET STANDARDSДокумент18 страницINTERNET STANDARDSDawn HaneyОценок пока нет

- C.H. Padliya & Co.: Chartered AccountantsДокумент5 страницC.H. Padliya & Co.: Chartered AccountantsSarat KumarОценок пока нет

- C.H. Padliya & Co.: Chartered AccountantsДокумент6 страницC.H. Padliya & Co.: Chartered AccountantsSarat KumarОценок пока нет

- TDS Rates On Payments Other Than Salary and Wages To Residents (Including Domestic Companies)Документ3 страницыTDS Rates On Payments Other Than Salary and Wages To Residents (Including Domestic Companies)Prince RaichandОценок пока нет

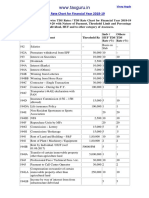

- TDS Rate Chart FY 2021-2022: Section Code Nature of Payment Threshold (In RS.) TDS Rate (In %) Indv/HUF OthersДокумент7 страницTDS Rate Chart FY 2021-2022: Section Code Nature of Payment Threshold (In RS.) TDS Rate (In %) Indv/HUF OthersRajОценок пока нет

- Rates of TDSДокумент30 страницRates of TDSsudhanshu88g1Оценок пока нет

- TDS RATE CHART FY 2021-22-FinalДокумент5 страницTDS RATE CHART FY 2021-22-FinalLeenaОценок пока нет

- Tds Rate Chart Fy 2020Документ4 страницыTds Rate Chart Fy 2020KAUTUK KOLIОценок пока нет

- Tds Rate Chart Fy 2021-22Документ3 страницыTds Rate Chart Fy 2021-22Kadambari ShelkeОценок пока нет

- Tax Deducted at Source UnitДокумент13 страницTax Deducted at Source Unitsatyanarayan dashОценок пока нет

- TDS Rate Chart For FY 2022-2023 (AY 2023-2024) Including Budget 2022 Amendments - Taxguru - inДокумент15 страницTDS Rate Chart For FY 2022-2023 (AY 2023-2024) Including Budget 2022 Amendments - Taxguru - inSachin GuptaОценок пока нет

- Current Changes of TDS: Presented By, Ghanshyam WatekarДокумент10 страницCurrent Changes of TDS: Presented By, Ghanshyam Watekarpraful_watekarОценок пока нет

- TDS EntryДокумент11 страницTDS Entryश्रीनाथ राजाराम दातेОценок пока нет

- TDS RATE CHART F.Y. 2019-20 (A.Y. 2020-21) : WWW - Bharatax.inДокумент1 страницаTDS RATE CHART F.Y. 2019-20 (A.Y. 2020-21) : WWW - Bharatax.inGajendra Singh Rajpurohit Chadwas IIIОценок пока нет

- TdsPac RateCard 0910Документ2 страницыTdsPac RateCard 0910Ebanezer PaulrajОценок пока нет

- TDS Rates and ReturnsДокумент4 страницыTDS Rates and ReturnsMohanlal BishnoiОценок пока нет

- TDS Rate ChartДокумент2 страницыTDS Rate Chartshashi370Оценок пока нет

- Revised TDS Wef 14.05.20Документ7 страницRevised TDS Wef 14.05.20MANAN KOTHARIОценок пока нет

- TDS Rate Chart FY 2020-2021 (Covid-19) : Section Code Nature of Payment Threshold (In RS.) TDS Rate (In %) (Covid-19)Документ4 страницыTDS Rate Chart FY 2020-2021 (Covid-19) : Section Code Nature of Payment Threshold (In RS.) TDS Rate (In %) (Covid-19)Sahay AlokОценок пока нет

- Tds Income Tax Rates Fy 2010-11Документ13 страницTds Income Tax Rates Fy 2010-11Surender KumarОценок пока нет

- Ssra Tds Rates 2021-2022Документ10 страницSsra Tds Rates 2021-2022deepu kОценок пока нет

- What Is TDS?: Tax Deducted at Source (TDS)Документ8 страницWhat Is TDS?: Tax Deducted at Source (TDS)Sandeep RajpootОценок пока нет

- Tds BookletДокумент22 страницыTds BookletSanjayThakkarОценок пока нет

- TDS Rates Applicable from 01.10.2009Документ2 страницыTDS Rates Applicable from 01.10.2009Gaurav MalhotraОценок пока нет

- Budget 2019 Updates - Key Income Tax Changes and TDS RatesДокумент6 страницBudget 2019 Updates - Key Income Tax Changes and TDS RatesAjeet KumarОценок пока нет

- Accounts & Taxations Interview Related NotesДокумент5 страницAccounts & Taxations Interview Related NotesRahul Baburao AbhaleОценок пока нет

- 56 Tds Tcs Rate Chart W e F 01 10 09Документ1 страница56 Tds Tcs Rate Chart W e F 01 10 09Shankar BidadiОценок пока нет

- Tds Rate ChartДокумент49 страницTds Rate ChartSANJEEVОценок пока нет

- WWW - Taxguru.in: TDS Rate Chart For Financial Year 2018-19Документ1 страницаWWW - Taxguru.in: TDS Rate Chart For Financial Year 2018-19Sunny NarangОценок пока нет

- Instapdf - in Tds Rate Chart Fy 2023 24 Ay 2024 25 355Документ7 страницInstapdf - in Tds Rate Chart Fy 2023 24 Ay 2024 25 355skassociatetaxconsultantОценок пока нет

- TDS Chart FY 23-24Документ6 страницTDS Chart FY 23-24kuldeep singhОценок пока нет

- TDS Provisions under Income Tax Act 1961Документ77 страницTDS Provisions under Income Tax Act 1961Sachin KumarОценок пока нет

- Page 1 of 2Документ2 страницыPage 1 of 2veena_hewalekarОценок пока нет

- TDS Rate & Tax Provisions For F.Y. 2019-20 (A.Y. 2020-21) : TDS Is Deducted On The Following Types of PaymentsДокумент10 страницTDS Rate & Tax Provisions For F.Y. 2019-20 (A.Y. 2020-21) : TDS Is Deducted On The Following Types of PaymentsnagallanraoОценок пока нет

- TDS Rates Chart For Financial Year 2021 22 Assessment Year 2022 23 1Документ5 страницTDS Rates Chart For Financial Year 2021 22 Assessment Year 2022 23 1Audit ManifestОценок пока нет

- TDS (Tax Deducted at Source) Rate Chart For Financial Year 2010-11Документ13 страницTDS (Tax Deducted at Source) Rate Chart For Financial Year 2010-11av_meshramОценок пока нет

- TDS and TCS Rate Chart 2023Документ5 страницTDS and TCS Rate Chart 2023DEEPAK SHARMAОценок пока нет

- TDS and TCS-rate-chart-2023 RemovedДокумент4 страницыTDS and TCS-rate-chart-2023 Removeddurgeshsonawane65Оценок пока нет

- TDS - and - TCS Rate Chart 2024Документ5 страницTDS - and - TCS Rate Chart 2024Taxation KTPL (Kalyani Techpark Taxation)Оценок пока нет

- Commonly used TDS Provisions for payments in IndiaДокумент17 страницCommonly used TDS Provisions for payments in IndiaSonika GuptaОценок пока нет

- TDS - Rates - 07 - 08Документ3 страницыTDS - Rates - 07 - 08KRISHNAKUMARОценок пока нет

- TDS_and_TCS-rate-chart-2025Документ5 страницTDS_and_TCS-rate-chart-2025jsparakhОценок пока нет

- Tax Deducted at Source (TDS)Документ7 страницTax Deducted at Source (TDS)Rupali SinghОценок пока нет

- Section 192:: Payment of SalaryДокумент7 страницSection 192:: Payment of SalaryCacptCoachingОценок пока нет

- TDS Rate Chart 1Документ1 страницаTDS Rate Chart 1bulu1987Оценок пока нет

- TDS Summary May 24Документ2 страницыTDS Summary May 24Akil MalekОценок пока нет

- TDS Rate Chart - FY 2021-22Документ3 страницыTDS Rate Chart - FY 2021-22Ram YadavОценок пока нет

- TDS Rate Chart For Financial Year 2022 23 Assessment Year 2023 24Документ9 страницTDS Rate Chart For Financial Year 2022 23 Assessment Year 2023 24Sumukh TemkarОценок пока нет

- Complete Tds CourseДокумент32 страницыComplete Tds CourseAMLANОценок пока нет

- Complete Tds CourseДокумент32 страницыComplete Tds CourseAMLANОценок пока нет

- TCS Provisions For The FY 2021-22 AY 2022-23Документ11 страницTCS Provisions For The FY 2021-22 AY 2022-23Hardik gabaОценок пока нет

- TDS Ready Reckoner (1) 11Документ1 страницаTDS Ready Reckoner (1) 11senthilkumar_kskОценок пока нет

- TDS RatesДокумент1 страницаTDS Ratespankaj_adv5314Оценок пока нет

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesОт EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesОценок пока нет

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryОт EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryОценок пока нет

- Sri Satyanarayana Puja - Powerful Family PujaДокумент6 страницSri Satyanarayana Puja - Powerful Family PujaSarat KumarОценок пока нет

- Disclosure To Promote The Right To InformationДокумент8 страницDisclosure To Promote The Right To InformationSarat KumarОценок пока нет

- Disclosure To Promote The Right To InformationДокумент6 страницDisclosure To Promote The Right To InformationSarat KumarОценок пока нет

- Disclosure To Promote The Right To InformationДокумент11 страницDisclosure To Promote The Right To InformationSarat KumarОценок пока нет

- Disclosure To Promote The Right To InformationДокумент5 страницDisclosure To Promote The Right To InformationSarat KumarОценок пока нет

- Disclosure To Promote The Right To InformationДокумент16 страницDisclosure To Promote The Right To InformationSarat KumarОценок пока нет

- Disclosure To Promote The Right To InformationДокумент16 страницDisclosure To Promote The Right To InformationSarat KumarОценок пока нет

- Disclosure To Promote The Right To InformationДокумент18 страницDisclosure To Promote The Right To InformationSarat KumarОценок пока нет

- ZHAO 1993compressedДокумент146 страницZHAO 1993compressedsandi123inОценок пока нет

- Disclosure To Promote The Right To InformationДокумент9 страницDisclosure To Promote The Right To InformationSarat KumarОценок пока нет

- Quality Risk Management GuidelineДокумент29 страницQuality Risk Management GuidelineSarat KumarОценок пока нет

- Is 10151 1982 PDFДокумент32 страницыIs 10151 1982 PDFSarat KumarОценок пока нет

- SOP For Quality Risk Management - Pharmaceutical GuidelinesДокумент14 страницSOP For Quality Risk Management - Pharmaceutical GuidelinesSarat KumarОценок пока нет

- Diploma in PackagingДокумент5 страницDiploma in PackagingSarat KumarОценок пока нет

- Barry O Donovan Novartis (Compatibility Mode)Документ3 страницыBarry O Donovan Novartis (Compatibility Mode)Sarat KumarОценок пока нет

- Barry O Donovan Novartis (Compatibility Mode)Документ3 страницыBarry O Donovan Novartis (Compatibility Mode)Sarat KumarОценок пока нет

- Disclosure To Promote The Right To InformationДокумент18 страницDisclosure To Promote The Right To InformationSarat KumarОценок пока нет

- Disclosure To Promote The Right To InformationДокумент15 страницDisclosure To Promote The Right To InformationSarat KumarОценок пока нет

- Process Quality Risk Assessment at NovartisДокумент13 страницProcess Quality Risk Assessment at Novartiskumar_chemicalОценок пока нет

- CQA 2013 InsertДокумент16 страницCQA 2013 InsertcsteeeeОценок пока нет

- Certification Vs CertificateДокумент2 страницыCertification Vs CertificateSubramaniyam VaithilingamОценок пока нет

- Homework 5 - 2020 - 01 - v3 - YH (v3) - ALV (v2)Документ5 страницHomework 5 - 2020 - 01 - v3 - YH (v3) - ALV (v2)CARLOS DIDIER GÓMEZ ARCOSОценок пока нет

- MAPEH 2 SBC 2nd Quarterly AssesmentДокумент5 страницMAPEH 2 SBC 2nd Quarterly AssesmentReshiele FalconОценок пока нет

- The Congressional Committee and Philippine Policymaking: The Case of The Anti-Rape Law - Myrna LavidesДокумент29 страницThe Congressional Committee and Philippine Policymaking: The Case of The Anti-Rape Law - Myrna LavidesmarielkuaОценок пока нет

- Experiment 4 (Group 1)Документ4 страницыExperiment 4 (Group 1)Webster Kevin John Dela CruzОценок пока нет

- Adolescent and Sexual HealthДокумент36 страницAdolescent and Sexual Healthqwerty123Оценок пока нет

- Bandong 3is Q4M6Документ6 страницBandong 3is Q4M6Kento RyuОценок пока нет

- Husqvarna 340/345/350 Operator's ManualДокумент47 страницHusqvarna 340/345/350 Operator's ManualArtur MartinsОценок пока нет

- CanteenДокумент8 страницCanteenmahesh4uОценок пока нет

- Product GuideДокумент13 страницProduct Guidekhalid mostafaОценок пока нет

- TESC CRC Office & Gym Roof Exterior PaintingДокумент6 страницTESC CRC Office & Gym Roof Exterior PaintinghuasОценок пока нет

- Mri 7 TeslaДокумент12 страницMri 7 TeslaJEAN FELLIPE BARROSОценок пока нет

- India Vision 2020Документ9 страницIndia Vision 2020Siva KumaravelОценок пока нет

- Presente Continuo Present ContinuosДокумент4 страницыPresente Continuo Present ContinuosClaudio AntonioОценок пока нет

- Stepan Formulation 943Документ2 страницыStepan Formulation 943Mohamed AdelОценок пока нет

- 670W Bifacial Mono PERC ModuleДокумент2 страницы670W Bifacial Mono PERC Modulemabrouk adouaneОценок пока нет

- Kloos Community Psychology Book FlyerДокумент2 страницыKloos Community Psychology Book FlyerRiska MirantiОценок пока нет

- T1D Report September 2023Документ212 страницT1D Report September 2023Andrei BombardieruОценок пока нет

- 4Документ130 страниц4Upender BhatiОценок пока нет

- Pakistan List of Approved Panel PhysicianssДокумент5 страницPakistan List of Approved Panel PhysicianssGulzar Ahmad RawnОценок пока нет

- Fluvial Erosion Processes ExplainedДокумент20 страницFluvial Erosion Processes ExplainedPARAN, DIOSCURAОценок пока нет

- Environmental Product Declaration: PU EuropeДокумент6 страницEnvironmental Product Declaration: PU EuropeIngeniero Mac DonnellОценок пока нет