Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5784)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Performance Analysis of Top 5 Banks in India HDFC Sbi Icici Axis Idbi by SatishpgoyalДокумент72 страницыPerformance Analysis of Top 5 Banks in India HDFC Sbi Icici Axis Idbi by SatishpgoyalSatish P.Goyal71% (17)

- Offshore Financial Centers: Hughes and Macdonald TextДокумент28 страницOffshore Financial Centers: Hughes and Macdonald TextAlisha SharmaОценок пока нет

- HRG-Complaint Resolution GLOBALДокумент32 страницыHRG-Complaint Resolution GLOBALDannyShallowОценок пока нет

- Wall Street Crash of 1929Документ15 страницWall Street Crash of 1929Sanchita100% (1)

- Islamic Banking Concepts of Qar, Wadiah and AmanahДокумент24 страницыIslamic Banking Concepts of Qar, Wadiah and Amanah_*_+~~>Оценок пока нет

- Lalit Narayan Mithila University: Kameshwaranagar, DarbhangaДокумент2 страницыLalit Narayan Mithila University: Kameshwaranagar, Darbhangafida mohammadОценок пока нет

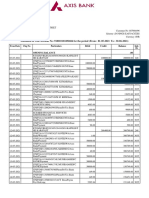

- Account STMTДокумент3 страницыAccount STMTDhanush KumarОценок пока нет

- Regulation of Thrift Banks and their Organization and OperationsДокумент11 страницRegulation of Thrift Banks and their Organization and Operationsskylark74100% (1)

- Teena FDHGДокумент2 страницыTeena FDHGTeena VarmaОценок пока нет

- Sage One Accounting Getting Started Guide 1Документ82 страницыSage One Accounting Getting Started Guide 1romeoОценок пока нет

- Business Finance and The SMEsДокумент6 страницBusiness Finance and The SMEstcandelarioОценок пока нет

- NOTES Onthe Bank Secrecy Law (RA1405)Документ9 страницNOTES Onthe Bank Secrecy Law (RA1405)edrianclydeОценок пока нет

- Brief History of International BankingДокумент27 страницBrief History of International BankingAsima Syed91% (11)

- Reported SpeechДокумент2 страницыReported SpeechKinga SzászОценок пока нет

- British MoneyДокумент2 страницыBritish MoneyСофія Вячеславівна ДемировськаОценок пока нет

- Abhilasha DubeyДокумент8 страницAbhilasha Dubeyanon_292119648Оценок пока нет

- In Gold We Trust 2015Документ140 страницIn Gold We Trust 2015Gold Silver Worlds100% (1)

- Feed Industry of Bangladesh:: Sustaining Covid-19 and Potentials in Upcoming DaysДокумент41 страницаFeed Industry of Bangladesh:: Sustaining Covid-19 and Potentials in Upcoming Daysnandt bangladeshОценок пока нет

- Project On Cooperativr BanksДокумент22 страницыProject On Cooperativr BanksVeeru VeeruОценок пока нет

- HUDCO Tax Free Bonds - Shelf ProspectusДокумент282 страницыHUDCO Tax Free Bonds - Shelf ProspectusSachin ShirwalkarОценок пока нет

- Piggery Farming in Tripura An OverviewДокумент10 страницPiggery Farming in Tripura An OverviewAbdur Rahman Choudhury100% (1)

- Why Should Engineers Study Economics?: Macroeconomics Microeconomics Microeconomics MacroeconomicsДокумент5 страницWhy Should Engineers Study Economics?: Macroeconomics Microeconomics Microeconomics MacroeconomicsSachin SadawarteОценок пока нет

- TOEIC Analyst BookДокумент231 страницаTOEIC Analyst Booklam266100% (1)

- Analysis The Statutory Audit of Bank FormatДокумент9 страницAnalysis The Statutory Audit of Bank FormatDhiraj JainОценок пока нет

- Levy Hermanos Versus GervacioДокумент3 страницыLevy Hermanos Versus GervacioAnskee Tejam100% (1)

- BFSiДокумент70 страницBFSisayanuchatterjee4Оценок пока нет

- Fintech in The Banking System of Russia Problems AДокумент13 страницFintech in The Banking System of Russia Problems Amy VinayОценок пока нет

- Sec. Cert Sample - RCBC ClosingДокумент1 страницаSec. Cert Sample - RCBC ClosingBryan Arupo75% (8)

- AC 506 Midterm ExamДокумент10 страницAC 506 Midterm ExamJaniña NatividadОценок пока нет

- Journal Entries & Correction of ErrorsДокумент33 страницыJournal Entries & Correction of ErrorsSteven RaintungОценок пока нет