Вам также может понравиться

- Choice Discount RateДокумент6 страницChoice Discount Rateprasad_kcp0% (1)

- Employee DiscountДокумент1 страницаEmployee DiscountHailey Patrick100% (1)

- Marriott Promo Codes 2014Документ4 страницыMarriott Promo Codes 2014Dave Ortiz100% (1)

- US Discounts and Offers PDFДокумент31 страницаUS Discounts and Offers PDFFernanda Daly100% (3)

- LSOP - Explore Authorization Form - Associate Non-Room Discount CardДокумент2 страницыLSOP - Explore Authorization Form - Associate Non-Room Discount Card9899659344Оценок пока нет

- Car Rental CodeДокумент2 страницыCar Rental CodeTwilightDawn0% (1)

- Hotel Transportation and Discount Information Chart - February 2013Документ29 страницHotel Transportation and Discount Information Chart - February 2013scfp4091Оценок пока нет

- Benefits of Being HiltonДокумент3 страницыBenefits of Being HiltonMariaMcDermott100% (1)

- 2010 1040a Federal Tax FormДокумент2 страницы2010 1040a Federal Tax FormesvrasОценок пока нет

- RARES DiscountsДокумент2 страницыRARES DiscountsSelarom AnthonyОценок пока нет

- Hotel Friends & Family VoucherДокумент1 страницаHotel Friends & Family VouchermarkballanОценок пока нет

- Hotel Discount GridДокумент85 страницHotel Discount Gridmanishpandey1972Оценок пока нет

- Employee DiscountsДокумент2 страницыEmployee DiscountsBlake Griffin100% (1)

- Marriott Consumer Incentives Overview: Who We AreДокумент46 страницMarriott Consumer Incentives Overview: Who We AreAshleyFurnitureОценок пока нет

- Wells Fargo MIS 08APR - 2015Документ60 страницWells Fargo MIS 08APR - 2015eduardo balinoОценок пока нет

- Hotel Discount CodesДокумент1 страницаHotel Discount CodeslearnandliveОценок пока нет

- Hotel Booking Confirmed, Pack Your Bags Now !: Apr 19 Apr 20Документ2 страницыHotel Booking Confirmed, Pack Your Bags Now !: Apr 19 Apr 20Zamirtalent Tr100% (1)

- CardEase TestCardDataДокумент8 страницCardEase TestCardDataGregorio Gazca0% (1)

- Groupon A63EFA1D2BДокумент1 страницаGroupon A63EFA1D2BSalif NdiayeОценок пока нет

- Current & Recent Credit Card Signup BonusesДокумент31 страницаCurrent & Recent Credit Card Signup BonusesRakib SikderОценок пока нет

- Codes CorpДокумент1 страницаCodes CorpDanielle SeveranceОценок пока нет

- Introduction To Fleet CardДокумент5 страницIntroduction To Fleet CardAbhinaw SurekaОценок пока нет

- American Express® International Dollar CardДокумент1 страницаAmerican Express® International Dollar Cardfranck petbeamОценок пока нет

- 2 Night Welcome Home Quarantine Packages: Confirm Details + BookДокумент2 страницы2 Night Welcome Home Quarantine Packages: Confirm Details + BookVibinОценок пока нет

- Bank CardsДокумент2 страницыBank Cardsalex_212Оценок пока нет

- Rental CarДокумент79 страницRental CarNavit Srivastava0% (6)

- Frequently Asked Questions: EligibilityДокумент6 страницFrequently Asked Questions: EligibilityQuynh TranОценок пока нет

- Merchant Manual (En)Документ137 страницMerchant Manual (En)Abu Rahma Sarip RamberОценок пока нет

- Giftcard ListДокумент7 страницGiftcard ListLuxОценок пока нет

- AsgДокумент307 страницAsgAlexandr TrotskyОценок пока нет

- Hotel VoucherДокумент2 страницыHotel VoucherjoserslealОценок пока нет

- Travel Hacking SpreadsheetДокумент40 страницTravel Hacking SpreadsheetRafael Assis100% (1)

- Jumpstart Credit Card Processing (Version 1)Документ15 страницJumpstart Credit Card Processing (Version 1)Oleksiy KovyrinОценок пока нет

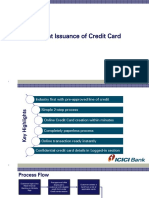

- Instant Issuance of Credit Card - Process Flow-1Документ15 страницInstant Issuance of Credit Card - Process Flow-1pawanОценок пока нет

- Merchant InvoiceДокумент1 страницаMerchant InvoiceHanuman MbaliveprojectsОценок пока нет

- ReadmeДокумент1 страницаReadmeposa akhilОценок пока нет

- Marriot PDFДокумент1 страницаMarriot PDFSarah Price-MarcianoОценок пока нет

- Random Test Credit Card NumbersДокумент3 страницыRandom Test Credit Card NumbersLope100% (1)

- American ExpressДокумент12 страницAmerican ExpressBTC FAREWELL PARTY'S NTVTОценок пока нет

- American Express Travel PDFДокумент4 страницыAmerican Express Travel PDFfooОценок пока нет

- David Lightman-WPS OfficeДокумент33 страницыDavid Lightman-WPS OfficeMikiОценок пока нет

- Hotel CodesДокумент1 страницаHotel Codesapi-351394398100% (1)

- Sign In: Get The Scoop On Vanilla GiftДокумент1 страницаSign In: Get The Scoop On Vanilla GiftSarah JoyОценок пока нет

- Choice Hotels: 20% Discount Off of The Hotel's Best Available Rate (BAR) at The Time of Booking at OverДокумент2 страницыChoice Hotels: 20% Discount Off of The Hotel's Best Available Rate (BAR) at The Time of Booking at OverMichaekОценок пока нет

- Safari - Oct 13, 2020 at 6:15 PMДокумент1 страницаSafari - Oct 13, 2020 at 6:15 PMJaboris JohnОценок пока нет

- Merediths Hallmark - Dealer Letter ActiveX dsiEMVUS - PDCX - AIMsi-45025672378 (2 DID) PDFДокумент7 страницMerediths Hallmark - Dealer Letter ActiveX dsiEMVUS - PDCX - AIMsi-45025672378 (2 DID) PDFKevin SinksОценок пока нет

- Google Play Gift Cards Methods PDFДокумент6 страницGoogle Play Gift Cards Methods PDFAhrisОценок пока нет

- AMEX Consumer BinsДокумент1 страницаAMEX Consumer BinsMajor MinorОценок пока нет

- Hotel CodesДокумент14 страницHotel CodesAngel BambaОценок пока нет

- Store Transactions List: A B C D E F G H 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26Документ8 страницStore Transactions List: A B C D E F G H 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26Shaan RoyОценок пока нет

- Sub Credit, Debit PDFДокумент3 страницыSub Credit, Debit PDFprasanth0% (1)

- Debit and Credit Card - EditedДокумент24 страницыDebit and Credit Card - EditedNikita MutrejaОценок пока нет

- OpenHotel User GuideДокумент114 страницOpenHotel User GuidefazliОценок пока нет

- Anexa 5 Amex CenturionДокумент1 страницаAnexa 5 Amex CenturionRaluca AndreeaОценок пока нет

- Wilson Electronics: Phone Test ModesДокумент3 страницыWilson Electronics: Phone Test ModesmpellegrinoОценок пока нет

- Trend Analysis, Horizontal Analysis, Vertical Analysis, Balance Sheet, Income Statement, Ratio AnalysisДокумент4 страницыTrend Analysis, Horizontal Analysis, Vertical Analysis, Balance Sheet, Income Statement, Ratio Analysisnaimenim100% (1)

- FM 2016 Week 3 - Chapter 3Документ86 страницFM 2016 Week 3 - Chapter 3Wira MokiОценок пока нет

- Aaaaaaa AaaaaaaaaaaaaaaaaaaaaaaaaaДокумент69 страницAaaaaaa AaaaaaaaaaaaaaaaaaaaaaaaaakomalpreetdhirОценок пока нет

- Class 12 Accountancy Project (Specific) Ratio Analysis PidiliteДокумент18 страницClass 12 Accountancy Project (Specific) Ratio Analysis PidiliteAvirup Chakraborty53% (38)

- Basics of Accounting: For SEBI Grade A ExamДокумент13 страницBasics of Accounting: For SEBI Grade A ExamALANKRIT TRIPATHI100% (1)

- ACN II - Home Assignment 1Документ8 страницACN II - Home Assignment 1Mehrab Hussain ZainОценок пока нет

- DELL LBO Model Part 1 CompletedДокумент21 страницаDELL LBO Model Part 1 CompletedMohd IzwanОценок пока нет

- FM02 Ch03 ShowДокумент58 страницFM02 Ch03 ShowRumah Cantik BungaОценок пока нет

- Chapter 6 Practical Aspects of Investment Appraisal (Student)Документ10 страницChapter 6 Practical Aspects of Investment Appraisal (Student)Nguyễn Thái Minh ThưОценок пока нет

- Chapter 7 - Financial RatiosДокумент8 страницChapter 7 - Financial RatiosNatasha GhazaliОценок пока нет

- Socrative Quiz - Week 4 (With Solution)Документ3 страницыSocrative Quiz - Week 4 (With Solution)jenny kimОценок пока нет

- Toy World HBS Case SolutionДокумент16 страницToy World HBS Case SolutionsmeilyОценок пока нет

- BDPW3103 Introductory Finance 1Документ7 страницBDPW3103 Introductory Finance 1dicky chongОценок пока нет

- Jawaban Kuis Uph Debt InvestmentДокумент3 страницыJawaban Kuis Uph Debt InvestmentSagita RajagukgukОценок пока нет

- Auto Car WashДокумент20 страницAuto Car WashAmeya Pai AngleОценок пока нет

- Currency INR INR INR INR INR: Income StatementДокумент26 страницCurrency INR INR INR INR INR: Income StatementNikhil BhatiaОценок пока нет

- Week 14 Analysis of Financial Statements Rev March 2021-TitmanДокумент67 страницWeek 14 Analysis of Financial Statements Rev March 2021-TitmanMefilzahalwa AlyayouwanОценок пока нет

- EB-TopR2R KPIs We Should Be TrackingДокумент13 страницEB-TopR2R KPIs We Should Be TrackingAndrewОценок пока нет

- Financial Analysis of Nestle LTDДокумент43 страницыFinancial Analysis of Nestle LTDShahbaz AliОценок пока нет

- Solution:: Notes ReceivableДокумент11 страницSolution:: Notes ReceivableAnonymous 46mMVoОценок пока нет

- Chart of AccountsДокумент9 страницChart of AccountsMarius PaunОценок пока нет

- LK - Komputer Lawu AccesoriesДокумент24 страницыLK - Komputer Lawu AccesoriesSyafri Syafrita100% (1)

- Module 2 - SFP.1Документ12 страницModule 2 - SFP.1Anne MoralesОценок пока нет

- Cash Flow Assignment-TusharДокумент8 страницCash Flow Assignment-TusharAssignments ExpressОценок пока нет

- (Cpar2016) AP-8007 (Audit of Receivables)Документ4 страницы(Cpar2016) AP-8007 (Audit of Receivables)Dawson Dela CruzОценок пока нет

- MASДокумент45 страницMASAngel YbanezОценок пока нет

- Periodic MethodДокумент14 страницPeriodic MethodRACHEL DAMALERIOОценок пока нет

- BMTH 1003 StudenttestДокумент7 страницBMTH 1003 Studenttestapi-327991016Оценок пока нет

- Afar 10Документ8 страницAfar 10RENZEL MAGBITANGОценок пока нет

- Total Financial RatiosДокумент2 страницыTotal Financial RatioshoangsubaxdОценок пока нет