Вам также может понравиться

- General Powers, Theory of General CapacityДокумент5 страницGeneral Powers, Theory of General CapacityMitchi BarrancoОценок пока нет

- Torts and Damages NotesДокумент17 страницTorts and Damages NotesadelainefaithОценок пока нет

- GGWPДокумент3 страницыGGWPMitchi BarrancoОценок пока нет

- General Powers, Theory of General CapacityДокумент5 страницGeneral Powers, Theory of General CapacityMitchi BarrancoОценок пока нет

- CasesДокумент11 страницCasesMitchi BarrancoОценок пока нет

- Penalties for Arson and Child Pornography Under Philippine LawДокумент23 страницыPenalties for Arson and Child Pornography Under Philippine LawMitchi BarrancoОценок пока нет

- Psychodynamic Perspectives of Personality COVER PAGEДокумент1 страницаPsychodynamic Perspectives of Personality COVER PAGEMitchi BarrancoОценок пока нет

- Torts and Damages: QUASI-DELICT (NCC: 2176)Документ13 страницTorts and Damages: QUASI-DELICT (NCC: 2176)Mitchi Barranco100% (1)

- Transcript CivProДокумент3 страницыTranscript CivProMitchi BarrancoОценок пока нет

- Valid termination to prevent lossesДокумент2 страницыValid termination to prevent lossesMitchi BarrancoОценок пока нет

- 10 Commandments Pass Bar ExamДокумент1 страница10 Commandments Pass Bar ExamMitchi BarrancoОценок пока нет

- Compromise agreement dismissalДокумент2 страницыCompromise agreement dismissalMitchi BarrancoОценок пока нет

- Doctrines and Principles in Remedial LawДокумент15 страницDoctrines and Principles in Remedial LawMitchi Barranco100% (1)

- Prac CourtДокумент4 страницыPrac CourtMitchi BarrancoОценок пока нет

- Valino Vs AdrianoДокумент11 страницValino Vs AdrianoMitchi BarrancoОценок пока нет

- Stages of Policy MakingДокумент2 страницыStages of Policy MakingMitchi BarrancoОценок пока нет

- Compromise Agreement Accident Reimbursement SimbajonДокумент3 страницыCompromise Agreement Accident Reimbursement SimbajonMitchi BarrancoОценок пока нет

- Torts and DamagesДокумент1 страницаTorts and DamagesMitchi BarrancoОценок пока нет

- Jino Rian O. Albarando Corporation Law Tuesday 5:30-9:30Документ3 страницыJino Rian O. Albarando Corporation Law Tuesday 5:30-9:30Mitchi BarrancoОценок пока нет

- Objections During Direct of Opposing Lawyer On Their Witness Objections During Offer of EvidenceДокумент1 страницаObjections During Direct of Opposing Lawyer On Their Witness Objections During Offer of EvidenceMitchi BarrancoОценок пока нет

- Compromise Agreement CrisostoДокумент2 страницыCompromise Agreement CrisostoMitchi BarrancoОценок пока нет

- Compromise Agreement Accident Reimbursement SimbajonДокумент3 страницыCompromise Agreement Accident Reimbursement SimbajonMitchi BarrancoОценок пока нет

- Compromise Agreement SettlementДокумент4 страницыCompromise Agreement SettlementMitchi BarrancoОценок пока нет

- Case Digest - Namarco Vs Associated Finance Company 19 Scra 962Документ1 страницаCase Digest - Namarco Vs Associated Finance Company 19 Scra 962Mitchi Barranco100% (2)

- CRIMINAL LAW - Latest Decisions PDFДокумент62 страницыCRIMINAL LAW - Latest Decisions PDFMichael Kenneth Po100% (2)

- Obligations ExplainedДокумент5 страницObligations ExplainedMitchi BarrancoОценок пока нет

- Ang Tibay v. Teodoro (74 Phil 50)Документ41 страницаAng Tibay v. Teodoro (74 Phil 50)Mitchi BarrancoОценок пока нет

- AnullmentДокумент19 страницAnullmentNatasha MilitarОценок пока нет

- Evidence Notes (Chan & Mitch)Документ90 страницEvidence Notes (Chan & Mitch)Mitchi BarrancoОценок пока нет

- Special Proceedings Case Digests on Presumptive Death, Money Claims, and PartitionДокумент57 страницSpecial Proceedings Case Digests on Presumptive Death, Money Claims, and PartitionMitchi BarrancoОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- BG, SBLC, Rwa LeaseДокумент23 страницыBG, SBLC, Rwa LeaseJosephОценок пока нет

- Merchant of Venice Act 1 Scene 3 SummaryДокумент9 страницMerchant of Venice Act 1 Scene 3 SummaryAnmol AgarwalОценок пока нет

- SJPДокумент3 страницыSJPapi-304127123Оценок пока нет

- Lawsuit Against City of SacramentoДокумент8 страницLawsuit Against City of SacramentoIsaac GonzalezОценок пока нет

- The Dogmatic Structure of Criminal Liability in The General Part of The Draft Israeli Penal Code - A Comparison With German Law - Claus RoxinДокумент23 страницыThe Dogmatic Structure of Criminal Liability in The General Part of The Draft Israeli Penal Code - A Comparison With German Law - Claus RoxinivanpfОценок пока нет

- TENSES Fill in VerbsДокумент2 страницыTENSES Fill in VerbsMayma Bkt100% (1)

- The Complete Guide to The WireДокумент329 страницThe Complete Guide to The Wirec8896360% (2)

- Passport RequirmentДокумент6 страницPassport RequirmentSom MohantyОценок пока нет

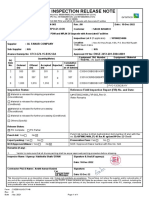

- IL#107000234686 - SIRN-003 - Rev 00Документ1 страницаIL#107000234686 - SIRN-003 - Rev 00Avinash PatilОценок пока нет

- Mirwaiz Yusuf ShahДокумент2 страницыMirwaiz Yusuf ShahNandu RaviОценок пока нет

- Deed of Chattel MortgageДокумент2 страницыDeed of Chattel MortgageInnoKal100% (1)

- "Playing The Man": Feminism, Gender, and Race in Richard Marsh's The BeetleДокумент8 страниц"Playing The Man": Feminism, Gender, and Race in Richard Marsh's The BeetleSamantha BuoyeОценок пока нет

- Aquino v. Delizo: G.R. No. L-15853, 27 July 1960 FactsДокумент6 страницAquino v. Delizo: G.R. No. L-15853, 27 July 1960 FactsMichelle FajardoОценок пока нет

- Arbitrary Detention - NOTESДокумент2 страницыArbitrary Detention - NOTESGo-RiОценок пока нет

- GPF Form 10A-1Документ3 страницыGPF Form 10A-1AnjanОценок пока нет

- Deadly UnnaДокумент14 страницDeadly Unnam100% (1)

- Cyber Law ProjectДокумент19 страницCyber Law ProjectAyushi VermaОценок пока нет

- 6 Royal Shirt V CoДокумент1 страница6 Royal Shirt V CoErwinRommelC.FuentesОценок пока нет

- Torcuator Vs Bernabe - G.R. No. 134219 - 20210705 - 223257Документ9 страницTorcuator Vs Bernabe - G.R. No. 134219 - 20210705 - 223257Maria Fiona Duran MerquitaОценок пока нет

- Pirate+Borg BeccaДокумент1 страницаPirate+Borg BeccaamamОценок пока нет

- Airmanship Vortex Ring State Part 1Документ4 страницыAirmanship Vortex Ring State Part 1Alexa PintoreloОценок пока нет

- Stronger Chords: HillsongsДокумент4 страницыStronger Chords: HillsongsAgui S. T. PadОценок пока нет

- The Naked Church 3rd EditionДокумент256 страницThe Naked Church 3rd EditionChikaokoroОценок пока нет

- FIFA World Cup Milestones, Facts & FiguresДокумент25 страницFIFA World Cup Milestones, Facts & FiguresAleks VОценок пока нет

- OV-10A (Black Pony) Information SheetДокумент14 страницOV-10A (Black Pony) Information SheetSesquipedaliacОценок пока нет

- Microsoft Word - Rop Job Application With Availablity Front-For FillableДокумент2 страницыMicrosoft Word - Rop Job Application With Availablity Front-For Fillableapi-356209272Оценок пока нет

- Geeta Saar 105 Removal and Resignation of Auditor Part - 2.doДокумент5 страницGeeta Saar 105 Removal and Resignation of Auditor Part - 2.doAshutosh SharmaОценок пока нет

- Court Rules on Liability of Accommodation PartyДокумент5 страницCourt Rules on Liability of Accommodation PartyAlyza Montilla BurdeosОценок пока нет

- Dagupan Trading Co. v. MacamДокумент1 страницаDagupan Trading Co. v. MacamBenneth SantoluisОценок пока нет

- Palaganas Vs PalaganasДокумент3 страницыPalaganas Vs PalaganasLucas Gabriel JohnsonОценок пока нет